10% dip in sales in Q3 and Q4 were highlighted by management in the interview before the results as well. Interview.

He had given the various reasons for dip in sales in North America - semiconductor shortage, driver shortage, metal price increase, inflation overall. But even with this management had maintained the guidance of 35-38% growth in sales which they are still maintaining and PAT growth of 30%.

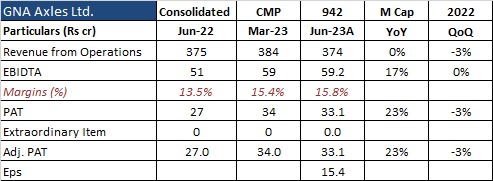

I have found management to be quite honest about the numbers over last 5 years and still PAT has grown from around 30cr in 2016 when they did IPO to 95+cr today. Sales have also more than doubled.

So, I wonder why market is not willing to give more than 15-16PE to this company? Is market concerned about the viability of this business in future? Wanted the opinion of fellow members on this company. @ayushmit - Would highly appreciate if you could share your thought process here since you have been following this company since few years as well.

Back to back two quarter good numbers by GNA Axles after muted last year Q4. Strong OCF, promoter buying continuously from open market, releasing pledged shares. All parameters are indicating for a rally. Stock price still 30% down from 52wk high, also valuation looks attractive.

Main points:

Full year FY 23 Revenue growth expected 22-24%

Q4 also going in same pace as Q3 (positive)

Domestic and exports strong in Q3

Reason for strong performance in Q3:

CV Market - 1st half 60% growth, 9 months 42% growth, 30% growth for the year

Growth in tractors is 5-7% which is very strong since base is high

Exports will be stable for next 2-3 quarters

Capacity being enhanced by 20% regularly via internal accruals

Addiitoan 25% capacity to be completed by June/July

SUV and small component utilization >50% and by may-june utilization will be greater than 80%

Then debottlenecking is planned and then there will be further growth for this segment by end of FY24

Working capital cycle is 120 days

FY 24 Outlook - Top line growth won’t be more than 8-9% on volume basis but because steel prices and freight will be more normalized could see revenue growth of around 15%

6th Mar 2023–GNA Axles --CNBC interview with Kulwin Seehra:

–55% sales is exports and 45% domestic & in that North America has a major chunk which is 60% of total export sales.Rest is Europe / South America & ROW

–FY23 will end at 1550 to 1600 Cr so that is 20% growth but for FY24 we dont expect double digit growth but 7 to 8% on FY23 because this Year is a Peak growth. This is 1750 Cr is at 80% of the capacity and expanding our capacity.All this is through internal accurals

–Capex --we are investing 40 to 50Crs per yr for FY23 & FY24.

–EVs are already contributing with existing cust. i.e 3 to 4% of total sales as of now.

–SUV & MUV Plant ( Have become operational in FY23 ) will contribute in the coming yr 4 to 5% i.e 70 to 80Cr of sales from that plant in the FY24.

–Margins --last couple of Qtrs margins are improving due to high cost earlier which have cooled down now, those will be maintained at 14.5% to 15% even in FY24

Continuous growth can be seen in this company. 10%-15% drop in demand from North America in Q1 forecast by management,and market reacted negatively. Opened with 5% green and closed with 4% red.

Tractor sales increased in 2022 and GNA’s market share increased in this segment

Long term borrowings at 47cr, 4.46m to 4.9m components we are producing right now.

Future outlook - expects growth in CV doemstic by 20%, tractor low single digit growth, first 5 months have been flat for tractor and 15% growth for CV domestic

export is stable at present, expecting to match sales revenue of last year, North america and europe are looking good right now

looking to increase our contribution from NA and europe

started rear axles for suv both domestic and exports. Slowly ramping up sales- can do 80cr this year

Expecting single digit growth this year 6-9%, steel prices are dropping every quarter so top line growth is limited

Answering a question on if they will consider stock split - Share price is steadily increasing, it also increases with shareholder interest. Our work is reinvestment of funds, growth and rest is upto interest of shareholders. If valuation increases a lot we will consider split no consideration right now.

Acquisition - we can consider if there is an opportunity. Did not seem like they are considering anything right now or they are looking out.

US strike in auto companies - It is limited to 3 big players, it is continuing and it is affecting their vehicle production in cars and SUV segment. We are in CV segment which are not under these unions, consumption of our goods due to this strike is not affected.

On competition or new players entering - No new player roughly in our area in India, only existing players. We cannot discuss competition in AGM

We have reinvested yearly to cut down our costs and we have 70% market share in tractor market.

On why we are not present much in tractor/off highway in US and only in CV - In CV exports it is standardised and economical to buy from us but off highway export is not standardised in US

Additional capacity of 600k by next April May. SUV capacity to be doubled by April

If entering African market - African market we never announced and we are not planning to go there as of now

EV axle shafts - Our axles are already there in EV trucks and SUV. No different axle/shafts are requried for EV vehicles. Other parts are different like engine etc. No additional investment for EV from our end is required. We are supplying axles and OEMs would already be using them in EVs, might be 2-3% of our sales. (It seemed like they are not at all affected by EVs as axles/shafts are same in EVs as well)

150cr more investment in next 2 years for capacity expansion. 100cr expansion done this year, 1m pieces capacity to be added, current capacity 7-8m pieces

Growth outlook for next 5 years - Revenue growth we are targeting 10% for next 5 years as base is high, margins should be maintained with our initiatives to cut down costs

On if we are planning to reduce debt instead of doing expansion as interest rates are going higher - debt equity we are maintaining below 0.3 which is well below what others are doing in forging industry

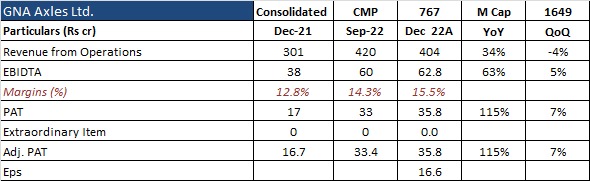

Net profit of GNA Axles declined 37.20% to Rs 22.47 crore in the quarter ended December 2023 as against Rs 35.78 crore during the previous quarter ended December 2022.

Sales declined 11.69% to Rs 357.00 crore in the quarter ended December 2023 as against Rs 404.24 crore during the previous quarter ended December 2022.

Will be interesting to see how much of drop in revenue is due to volume and realization. Since realizations are linked to steel prices which are down, I didn’t expect a very good quarter.