Could somebody explain what is part of “other income” in Glenmark’s case which has been the major factor for reduction in net profit.

Thanks

They have taken a write off on some intangible assets. Details to be known in concall.

Operating results are pretty solid. Ryaltris is doing well leading to jump in both ROW and europe.

With impending launch in us and 12 eu countries picture is expected to brighten from here.

Intrest cost are going down qoq and trend expected to continue.

India too performed well.some 15 % growth.

Q4 concall pointer

Munroe remediation likely by q4 and costing 20 30 mn usd in fy22 and will cost lower in fy 23

Us price erosion steady at high single digits

Pressure on RM due to china and russia situation leading to higher inventory

Money stuck in russia now getting released

Write of covid drugs approx 80 cr and some amount of write off expected in coming qtr

Europe row doing well on account of respiratory portfolio india doing well on acct of cvs, cns, respiratory and derma.

Flovent mdi filed and expected to be launched by fy 25

Ryaltris us launch expected in h2

Ichnos can pivot post proof of concept. Expected in 2 to 3 months. At least one out licensing this year

Margin to remain at 19 %

Revenue growth 6 to 8 % excluding covid growth in double digits

To me, most disappointing was the management not being forthcoming on what went wrong at Munroe. It was a new facility with no legacy issues, still they could not clear the FDA inspection. Glenn Saldanha, even on being pressed twice only repeated “Running a facility in the US is always going to be challenging”. Also, no clarity on Ichnos, they just keep promising but don’t deliver.

Disclosure - Invested since long with huge opportunity cost.

Q1 concall summary

India growing at 15 to 16% ex covid

US will be flat this yr and low single digit at best

Europe likely to continue at 15% for next 2 to 3 yr

Row markets performing well and likely to continue at current run rate, brazil at breakeven

API will grow with more capcity coming upstream, demand is steady ( from gls concall)

Overall guidance of 6 to 8% for the year

Ebidta for the year likely at 19 %

Munroe likely to be remediated and operational by q4, no new fililing from munroe as of now

12 launches expected in US and 25 in india,

Debt likely to be pared down further

Capex at 700 cr, 40 cr of write off expected of covid drugs

1 outlicensing deals expected in this fy

Ichnos 2 proof of concept (1342 & 1442) expected this yr and isb 2001 human trials expected

Capital raise in ichnos still being targeted in this fy,

Ryaltris likely to be 100 to 150 mn drug in 3yr.my guess it will do approx 200 cr this yr, 600 by next yr once china and US also approves and 1000 cr by 3rd yr.

Apart from flovent one more pmdi likely to be commercialised by fy25.

Manpower costs will be at normal levels.

US had both pricing issues as well as supply chain issues. At least supply chain will be better from q2

Fda queries for india baddi, aurangabad etc have been responded.

One small correction for ryaltris US has approved ryaltris commercial launch pending

I have two questions.

Q1: How long will Glenmark have patent protection and/or marketing exclusivity for Ryaltris?

Q2: What are the margins for Ryaltris are likely to be? Since Ryaltris is a novel drug combination so presumably the gross/operating margin for this product is likely to be significantly higher than generic formulations, right?

This guy left Ichnos already.

Typical patent protection in usa is for 10 year. I think it will be similar in most countries.

Margins should be higher. Significantly higher than generic. How much higher has not been indicated by the company.

Q3 call updates

Q4 likely to be in 3400 cr range, margin at 18%.

Fy 24 to have 10 to 12% growth with some debt reduction

Usa coming to 100 mn usd sales per qtr after long. Likely to continue in this range.

Row and europe consistently growing in double digits and likely to grow at this rate for couple of quaters predominantly on strength of respiratory

Flovent and pmdi likely to be filed in cy 23 and launched hopefully by fy 25.

Injectable launches contingent on remediation of munroe. Remediation hopefully by q1.

Goa baddi remediation likely by q4 or q1.

Ryaltris usa sales to pick by h2 of cy 23. 100 mn likely by fy 25. Current year in 20 to 25mn range

Ichnos- poc of 1342 by q1, 1442 by q2 and 2001 by q4. No timelines for outlicensing, capital raise.

Debt to be down r&d to be down, capex in 700 cr range. Inventory to remain high till remediation of goa, baddi.

Api external sales are good but cdmo and inhouse sales low.

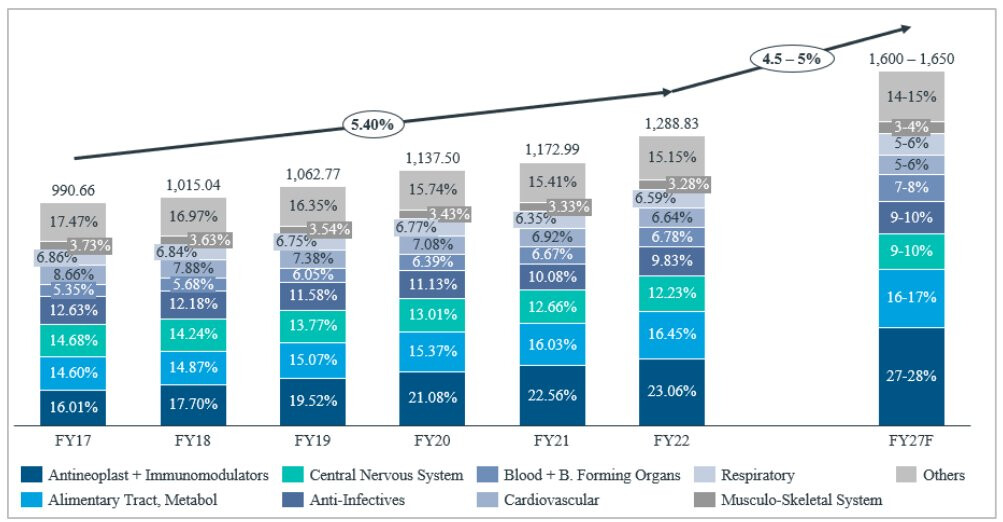

What is the source? Presumably, this chart is for Glenmark Pharma, right? What is the y-axis of the chart - consolidated revenue? … in what units? I ask because the reported consolidated revenue for FYe22 for GLENMARK was 12305 crores and I am confused as to what the the chart represents here …

above is the growth expected in various therapies worldwide

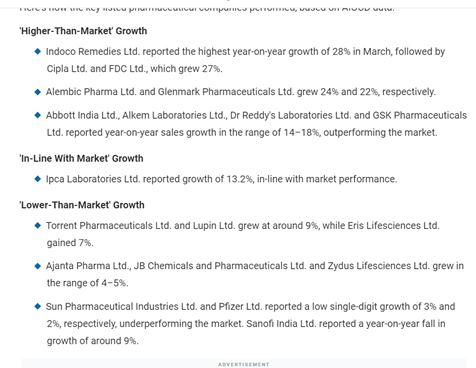

below is the march growth company wise

What the graph indicates is that at worldwide level most therapies are increasing at roughly the same pace as the mkt and have constant market share except onco which moves from 23 to 27 %.

Ichnos productsare cutting edge in this regard with isb 2001 leading complete remission in rats. The first line pdts 1342 and 1442 are also claimed by the company to be better than existing line of pdts.

Thanks for the explanation. Yes, GLENMARK’s investment in ICHNOS as a percentage of its profit after tax is quite substantial. Your remark indicate that if clinical trials are successful, the molecules/therapies being developed by ICHNOS could be very effective. The other question of course is to the safety of these molecules and how likely is such an innovative drug to successfully pass through the clinical trials…

Disclosure: invested, ~2% of portfolio.

Glenmark life science stake sell

Posting in GLS thread. By mistake posted here…