100% agreed with you

This was posted to share investment thesis

Most off things r well covered in our thread only new I found … Some key scuttlebutt findings…

So share it .

Disclosure invested from lower level only by reading this thread

Thanks

100% agreed with you

This was posted to share investment thesis

Most off things r well covered in our thread only new I found … Some key scuttlebutt findings…

So share it .

Disclosure invested from lower level only by reading this thread

Thanks

Everything is in the Ambit report. I don’t know why Stalwart is putting up a public piece on GWRL now, after having invested in 2015 in the late 300s. I personally think its not ethical and also smacks of post-facto chest thumping / “me too” mindset.

A company having a global market, having unique products with not any

formidable competitors. Long term crude price trend down and derivatives

being their raw material…still trading at around 20 PE only…IMHO, the

market will rerate Garware-wall sooner than later…

The reasons for PE rerating has been well summarised by ‘rvetri’:

Since GWRL is seeing interest these days, my two cents:

All those wishing to enter now should likely wait till after Q4 results to assess the impact, if any, of forex movements. It may give a good entry point. The performance may theoretically be affected by the 5% movement in currency rates between USD / INR . Other goods exporters have also been negatively affected by currency movement and suffered loss of margin despite growth in sales up to 3-4%. One such example is Sutlej Textiles and Industries, which has stated that currency movements have affected realizations (though there may be other reasons too).

Edit: also wish to point out that GWRL has in the past managed to avoid impact of foreign currency movements.

If you are in similar profession what would you do to seek more clients in terms of sharing success stories ? Precisely thats what is being done. No one is forcing anyone to buy. Its as good as a news piece.

Hi

I find results quite good but what i do not understand is its balance sheet.

Can anyone help me on above points?

Thanks

Prashant

Is there any capacity expansion? Need to confirm with CS. Otherwise this can be a red flag. Need to dig more. Pune friends can help.

Annual Report should give a little more information on this. Otherwise I think anyone attending the AGM should raise these questions.

Hi as has been pointed out here, I am still unable to get a hold on their provisions (150+cr) in FY17.

Clearly the stock has been re-rated and has been featured in the Sohn conf too.

Any insights into the current B/S PnL as per FY 17 will be appreciated. Thanx!

What is this Baseline survey, Can you pl share it.

Thanks

The FY 17 B/S is a bit remarkable- it means company is now negative working cap considering their A/R + Inv < A/P. Any luck with management interviews to understand this huge jump in A/P?

Also, not sure why they need short term debt in the absence of working cap + capex spends.

Some points noted

PAT has increased by 30% however the sales has gone up by 5 % . This could be because the company is enjoying some operating leverage .

The rise in profits could be also due to the fall in crude oil which has reduced the cost of materials considerably by 44 crores.

The net fixed asset turnover is falling since 2015 - Reduced from 4.91 to 4.31.

4 ) The firm has put money into investments to the extent of 105 crores .

From the above we can conclude that the sales is deterioating and the management is not keen on doing any capex and so putting money into other investments . Also the profit increase is primarily due to crude price going down , so it’s a negative.

Please note I have not completed the analysis, so various other aspects once studied can change my opinion.

Disc: not invested.

haha. good point!!!

Crude prices falling and raw material falling is exactly the reason why

Sales is going up slowly. The profit increasing inspite of sales increasing

by only 5% shows the pricing power of company and the brand equity. Look at

many other cos selling unbranded plastic compounds having crude derivative

as raw materials like ester…Sales and profits are falling…

@rvetri

Crude oil is the main raw material - However in quarter 4 there has been a 55% increase in the crude price . However the gross margins still went up , which is a positive .

The sales has increased because they have penetrated into newer markets like Norway and Chile . Also added some new products.

You mentioned about the pricing power, which I have also mentioned in my 1st point as operating leverage.

@Finrahul…

Agreed…instead of seeing QoQ, we should see how company has performed

when crude was at 120 D and when crude is at 50 D currently. Which is over

a 3 - 4 year band…In this back drop co has done extremely well to increase

sales…As customers always have a RM price pass through clause both when

RM prices go up or down… If you read Ambit’s latest research report on

Garware - all your doubts are well answered there…

Thanks Vetri

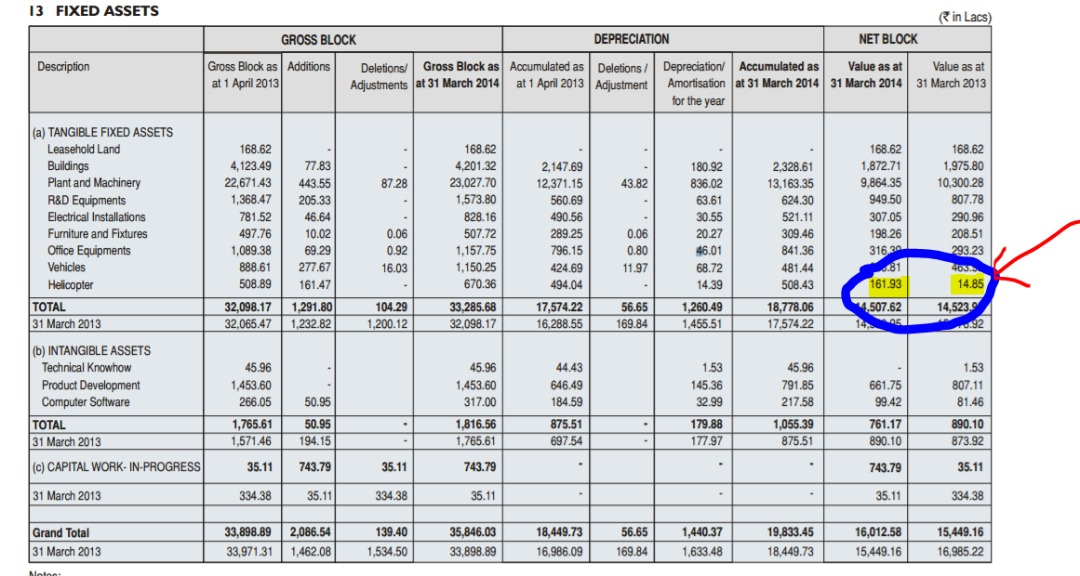

Ambit report hasnt covered some of the other red flags.

For eg.

what is this helicopter doing as an asset in Garware ?

Agreed…Good point…But how do we decide a helicopter is not a required

asset in Garware-walls business ??