Any Pune VPer planning to attend the Garware AGM on 11 Sep 2018? pl DM me in case of queries n other info

1 Like

A good article on Garware Tech Fibre

2 Likes

Did any one attend the AGM last month ?

That could be because they are taking the working capital loans at a much significant less interest rate and are probably getting high interest on the investments.

I have got interest in this counter due to resilience of share price in this falling markets.

Other points to note:

- Looking at Q2 FY19 results there is capital work in progress of around 6 cr. Company might be started deploying cash which is otherwise in last few years there is no capex.

- Company has done a tremendous job of improving the margins from last few years. Are these margins going to be sustained?

3 Likes

Results for Q3 & 9 Months 2018-19:

1 Like

Garware Technical Fibres (GTF) has been an interesting player in technical textiles.

- More than four decades of experience in the cordage industry.

- Market leader (60-65% share) in the organised domestic fishnets.

- Presence in more than 75 countries; 30% share in global salmon aquaculture netting and 17-18% in fishing segment.

- Supplies solution to diversified industries; increased TAM through constant innovation - fishing, aquaculture, agri-tech, shipping and industrial, sports, geo-synthetic and defense.

- Share of value added products gone up from 35% to 67% during last 3-4 years and contributes to 70-75% of profit currently.

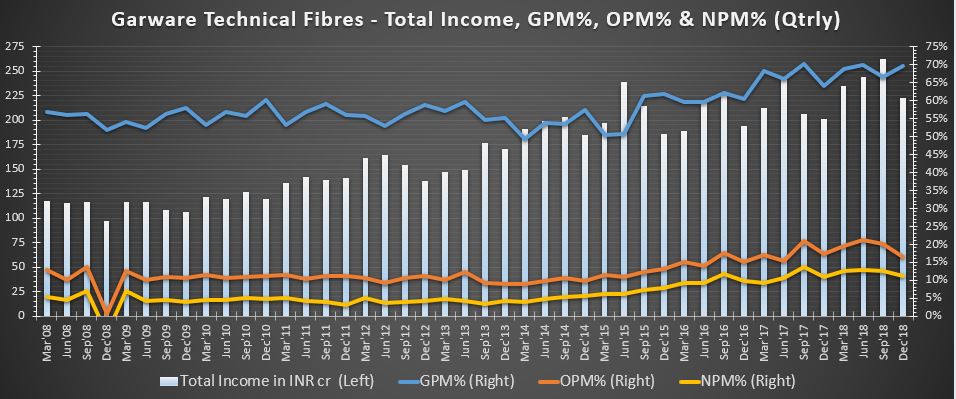

At a high level, seems a steady compounding machine; has potential to double PAT in next 4-5 years or earlier.

Impressive margin improvements (if we ignore last quarter) led by increasing focus on value added products and exports.

Interested in understanding about the following blips. GTF experts please chime in. Basically, just a hiccup in long-term story or something changed?

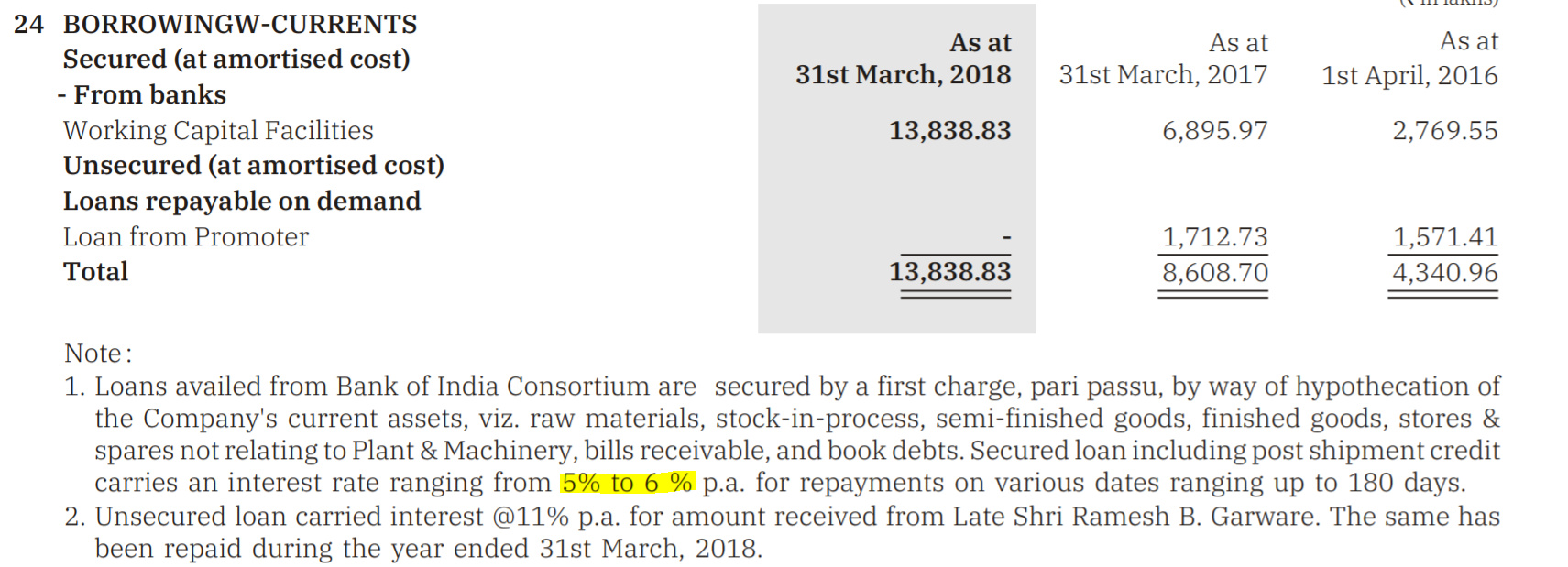

- Spike in Working Capital Changes (92 cr) in Fy18 (Ref: Cash Flows in screener.in)

- Debt gone up in Fy18 and 1HFy19 BS when not much change in topline, Fixed-Assets and/or CWIP.

- Margin drop in Q3Fy19.

5 Likes

-

Spike in WC for FY18 is due to lower increase in payables and a spike in other current assets. Within other current assets you can see from AR that “Balance with Govt Authorities” has spiked by almost 47 Cr. I think this has something to do with how GST works for export companies, while they pay GST on inputs, on the export part the input credit they receive but are not able to net off in this FY ends up as a current asset on the balance sheet. One can see this across many companies where the inputs are local but a chunk of the business is external. Of the 92 Cr increase in WC, almost 40 Cr is due to this while the rest of the increase is due to payables not rising in line with sales

-

Company has been using LIBOR linked packing credit for 2 years now. Between 2014 and 2017 company became debt free and a free cash flow engine, hence you can see investment book increasing from 2016 onward. The surplus gets parked in debt MF where one can expect to make 5.5%+ post tax on a conservative note while packing credit cost is lower than that. The FX gets taken care of due to the export book which as a natural hedge on a cash flow basis. The nature of debt is short term (primarily use to fund WC needs) which is serviced by the exports they make across a basket of currencies. Since the cost of debt is lower than the post tax return they expect to make on their treasury book by more than 150 bps, you can see that both debt and investment book are rising

-

Company sits on inventory of 60+ days, hence fluctuation in RM which is HDPE and PP can impact margins in the short term. While share of value added products is rising, there is still a good element of passing on RM changes to customers (especially in the domestic part of the business). Company margins spiked starting from 2015 when they were able to take benefit of lower RM but managed to keep their realizations higher relative to the fall in RM. This combined with the fact that net debt was brought down over the period led to an expansion in PAT margins. Company has been able to manage margins during the crude up cycle while benefiting during a down cycle.

17 Likes

Garware Technical Fibres profit rises by 24.7% in Q4 FY19

Revenue crosses 1000 crores and PAT grows by 19.5% in FY19

Q4FY19 Highlights:

• Revenue has grown by 23.3% to Rs. 289.5 Cr in Q4FY19 as compared to Rs. 234.8 Cr in Q4FY18

• Profit after tax grew by 24.7% to Rs. 36.6 Cr in Q4FY19 as compared to Rs. 29.3 Cr in the same

quarter last year

• EPS for Q4FY19 is at Rs. 16.73; this is a growth of 24.7% over Q4FY18

FY19Highlights:

• Revenue grew by 14.9% to Rs. 1017.8 Cr in FY19 as against Rs. 885.5 Cr in FY18

• Profit after tax grew by 19.5% to Rs. 125.6 Cr as compared to Rs.105.1Cr in FY18

• EPS stood at Rs. 57-4; reflecting a growth of 19.5% over FY18

2 Likes

BBC News featured our Anti-predator Aquaculture Cage Net “Sapphire SealPro”. Click here to read the article.

2 Likes

6 Likes

Standalone: Q1 FY20 Highlights:

-

Net Sales decreased by 4.9% to Rs. 232.3 Cr in Q1 FY20 as compared to Rs. 244.3 Cr in Q1 FY19

-

Profit before tax reduced by 8.6% to Rs. 42.2 Cr in Q1 FY20 as compared to Rs. 46.2 Cr in the same quarter last year

-

Net profit after tax has dropped by 5.7% to Rs. 29.6 Cr in the quarter as against Rs. 31.4 Cr in the corresponding period of FY19

-

EPS for Q1 FY20 is at Rs. 13.52; this is a de-growth of 5.7 % over Q1 FY19

“The year has begun with a steady performance in our Synthetic cordage segment. Our V2 technology based products are seeing good customer acceptance and excellent order flow. However, we faced headwinds in our Fibre and Industrial Products & Projects segment wherein the general elections led to a slowdown in release of tenders by both government and private sector. Post-election, some of these key projects have now been tendered and awarded. We will be working hard to make up for the delay in Q3 and Q4.”

4 Likes

Exports busines of GTF is a seasonal one with max coming in Q3 n Q4 . Q1 n Q2 are more domestic oriented business which got impacted due to some tenders getting delayed due to elections. These shud materialise in present quarter. Rupee was also quite strong this qtr which adversely impacted the performance.

All in all it remains a steady compounder just see how its eps has grown in last 5 years under ethical mgmt executing well.

1 Like

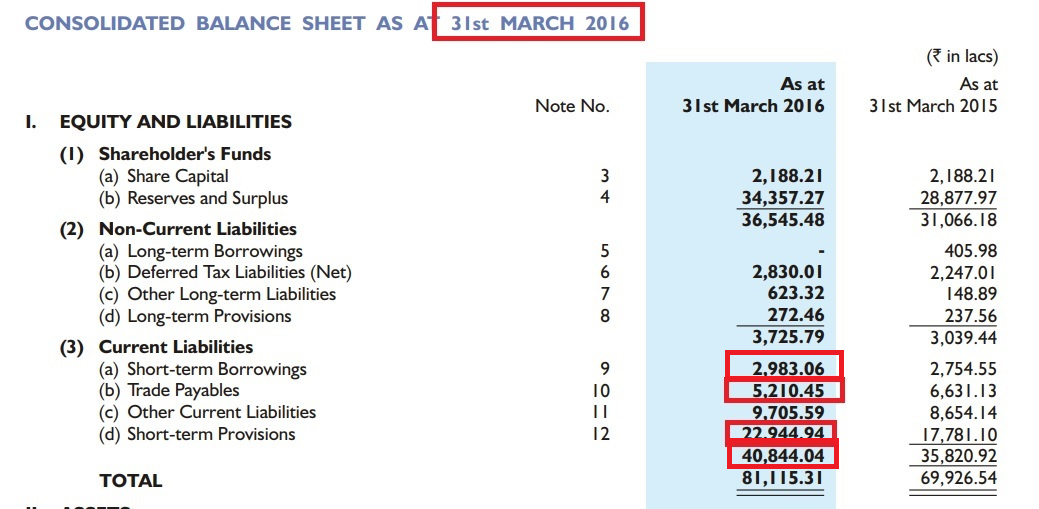

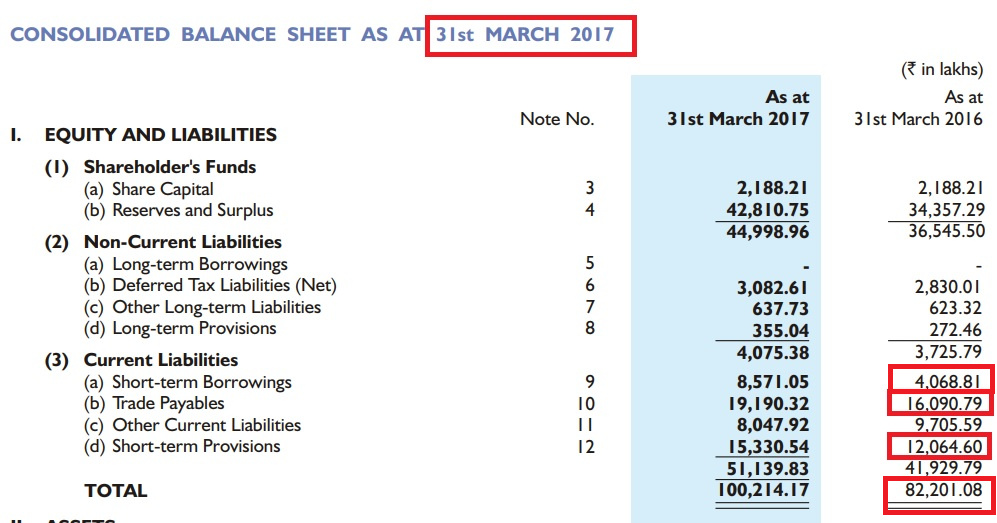

Yes, FY16 numbers are changed in FY 2017 AR. No explanations provided. Can they change previous year #s which were audited and provided in AR?

3 Likes

Can somebody who has invested in this stock, write an email to the company for clarification? They don’t hold any concalls also.

Disc: No holdings.

any VPer planning to attend garware tech fibre AGM on 17 Sep 19 in Pune ?

venue is auto cluster auditorium,auto cluster development n research instt ltd , h block c 181 off old pune mumbai highway,chinchwad- Pune -19

the article and its MD shashikant has nothing to do with garware technical fibres. have you even read the article before sharing ?

2 Likes

He is part of the family. Also Garware Technical Fibre and Shashikant are also promoters of Garware Marine Industries. Just to be aware of the quality of alliances.

1 Like

A good article on Garware tech Fibre n its dynamic owner Vayu Garware. Gives a good gist about good progress and execution this multibagger stock under leadership of Vayu did.Now see how beautifully GTF is performing in newer geographies in field of Salmon farming and aquaculture in Norway and Chile after major share in markets like Scotland and Canada.

A classic example of big wealth creation by remaining inactive in a quality stock over a period of 5 years in its journey of rs 60 to 1200.

Discl-Invested in the stock since 2015.

2 Likes

GARWARE AGM NOTES:

( Notes is my interpretation. There may be few mistakes and my views may be biased as I am invested…Below note contains feedback from my interaction with few others and learning from company products displayed at AGM )

Five year plan to double profit by 2023…first year was in the right direction to reach the goal. Working with consulting firms …mapped areas of opportunities… focus on expansion into new markets, market share expansion in existing markets. New products with better margins.

70% of business comes from value added products which add a lot of value to customers. We can maintain margins even if crude prices rise.

30% of revenue from commodity type products and margins will be impacted if crude rises significantly.

Last few years margins will sustain/improve due to our value added product …lag of 3-6 months to pass on RM increase.

Material used to make Garware products are : Nylon,Polyester,HDPE,Polypropylene (in the order of cost: highest to low). Dyneema is imported from the Netherlands company. Garware has exclusive agreement with the company they cannot sell dyneema to others. Dyneema is used to make ropes(Plateena) for ships and some parts of sports nets.

R&D of new products : Garware follows Gate process: 5 stages. At the end there should be demonstrated value proposition(profit) to customers otherwise Chairman will not allow product to launch…MD,CEO, top management team actively involved in new products R&D.

More than 30 patents registered. R&D is driven by customer feedback and finding solution.

New products ( introduced in last 2 years): contributes 30% of business. That’s our internal goal and its on track. New products may cannibalize the existing products but add value to customers and profits for Garware

New products: introduced recently and few on trials are: Harness for safety of Workers in real estate industry. Protective glove, Fitness rope (online amazon) lifting band and Lashing belts .

Domestic business: stagnant for few years due to reasons like demon,gst,monsoon etc which affected our agri business …efforts are on to grow domestic business. Domestic fishing net business is flat in last two years…some of our products indirectly depend on subsidy to farmers which is problem…looking to increase penetration in domestic fishing sector by introducing new products.

Q1 geosynthetic business affected due to elections and delay in execution of Govt tenders. Govt tenders have come come back now. We can make it up in Q3/ Q4. We are selective in orders with good margins only. In Infra construction, geosynthetic construction is better and faster than traditional. Garware makes metal nets replacing concrete,steel etc in rockfall,landslide protection…etc.

Agriculture products : shade and protective nets. Good growth in agri nets.Agriculture is a big opportunity for garware products for protected farming. The penetration is quite low (1%). Need to educate and convert farm from open to close farming which will take time. It depends of govt subsidy also. Garware has done studies done studies and field trials independently with farmers which demonstrated upto 30 % high yield +better price(depending on crop).

Defence: introduction of new products are in R&D status…It has to go through trials and overall process is slow. As of now the sales are very less but good margins. Army,Police…etc are customers. Products include: inflatable tents (larger focus-our products are successful ),sleeping bags, certain specific nets and ropes used in Himalayas,camouflage nets…

Aquaculture : Salmon fishing doing well worldwide. Countries like Chile,Norway, Scotland,Australia,NZ are good markets for Garware. Chille around 30-35% market share,entered a few years back…Norway 30-35% market share…Canada: high market share.

Doing upgradation of products by replacing older ones. Fishing depends on Govt regulations and restriction on aqua farming…Norway is planning to double their aqua production.

Aq nets: In the past we used to make nets using nylon, now replaced with HDPE or polypropylene. Its cheaper,easier to maintain and risk of algae formation is low. V2 new product with benefits for customers will help in better margins and growth.

Fisheries net : fishing boat with attached growling nets. Net design is specific,studied and improved by Garware to prevent load and drag on the boat. Mouth opening of net is wide which chances of catching of fish…made of hdpe…(sapphire nets)…nets with wide open and good abrasion resistance to prevent damage.

Coated fabrics: relatively new in india…converting from cotton based products in coated fabrics…more durable and better quality compared to cotton

Sport snets : we have to gain market share.

X2 yarn superior in terms of abrasion,cut wet resistance,elongation.

V2 yarn is new innovative, challenging product. Garware got patent…used mainly for aquaculture cages and customer response has been excellent. It prevents algae formation(frowling) and reduce the cost associated with cleaning which is cumbersome. Net profits are high in this. Getting new customers due to benefits of V2 products and replacement of old products through V2.

Distribution : Scotland ,Norway have partners who work with Garware and do servicing for our products…Chille,Canada we deal directly with company engineers.

SKU: challenge in managing as product increases. lean manufacturing practices,highly flexible,repeatable with quality maintenance.

Capex/acquisition: Not much capex required. Next year 40 to 50 cr capex…optimally utilising the assets…machines are flexible depending on production we are able to make changes. Suitable acquisition if its meets our criteria. Have enough internal accruals for acquisition. New capex we look for payback in 3-4 years at ebitda level.

Loans from promoters: We are net cash+ but will require cash sometimes based on business cycle…WC of 100 cr…investment of cash with longer cycles of maturity.

Payables : includes raw materials imports payables(60 -180 days) and subcontract payables of geosynthetic business(long payable days)… infra business our subcontract will get pay when we get paid from Govt as per our contract terms…

WC days : Exports high wc days 80-90 days…GST money from Govt is pending.

Tender based revenue : geo-synthetic business, business with transmission companies and industrial products.

24 Likes