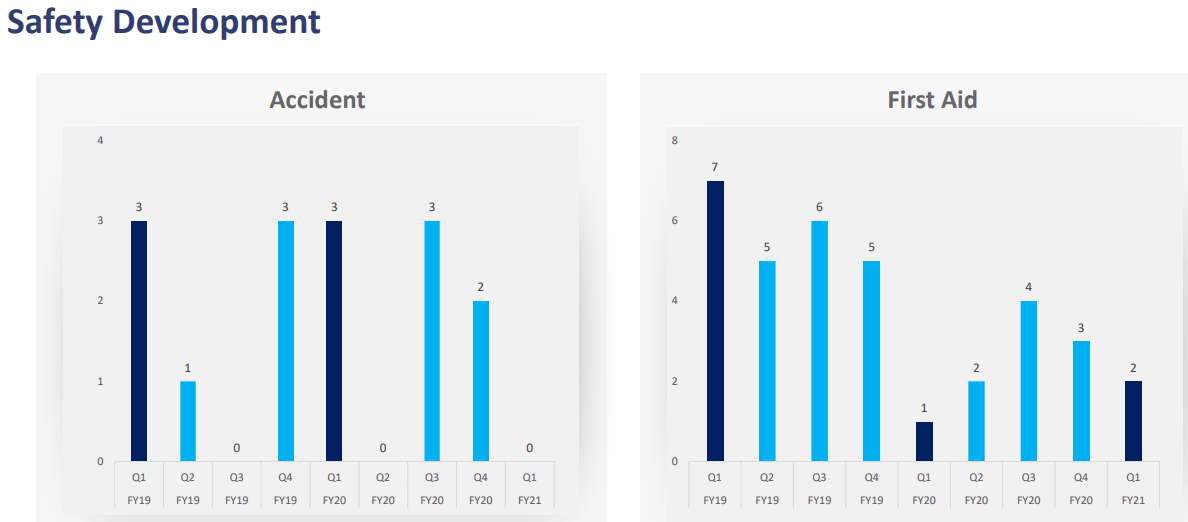

This is from the latest investor presentation. Is this normal? There may be serious quality issues with the product.

They seem to have performed impressively this quarter capturing the gains in the 2-W market. Good to see that the EV segment is going to be targeted with ather, Hero Electric and Okinawa. Obviously legacy business will lag because of the declining performance of CV and I think they have lost out because they were suppliers to erstwhile Maruti Omni. Views of the forum?

1 Like

Seeing this thread has been a bit inactive for now, I would like to know your opinions on the latest concall where they confirmed that OLA Electric is very happy with their front forks and have asked to ramp up the program. Won’t this provide a very big opportunity for the firm considering OLA Electric’s plans?

2 Likes

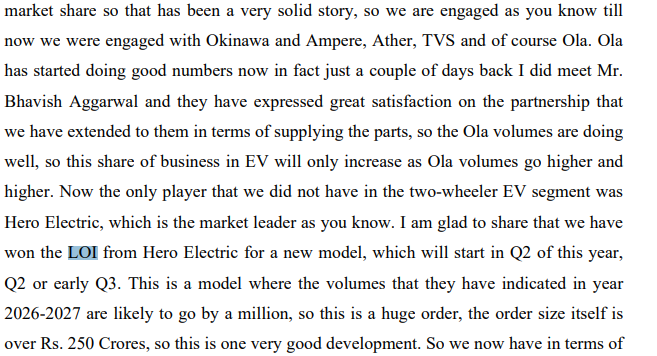

Have been itching to see how Gabriel will cope with the burgeoning EV segment. They seem to be doing the right things. Ola/Ampere/TVs seem to be onboarded as customers and now Hero Electric (the largest market share) seem to have handed a LOI worth potentially Rs 250 cr over 4-5 years.

Now we have to see if it translates to real numbers or not.

7 Likes

Gabriel India wave count, Looks like a flat here,Although w2 tend to be zigzag, Either way even if its W3 then it should break the “C” marked on chart, If not its a flat

Was analysing the stock, As a part of process i follow TA aswell so thought to share here for reference

2 Likes

Gabriel.pptx (2.3 MB)

My PPT on GABRIEL - covering the basics about the business, management and valuation

4 Likes

I would surely look into it. Hope, this helps!

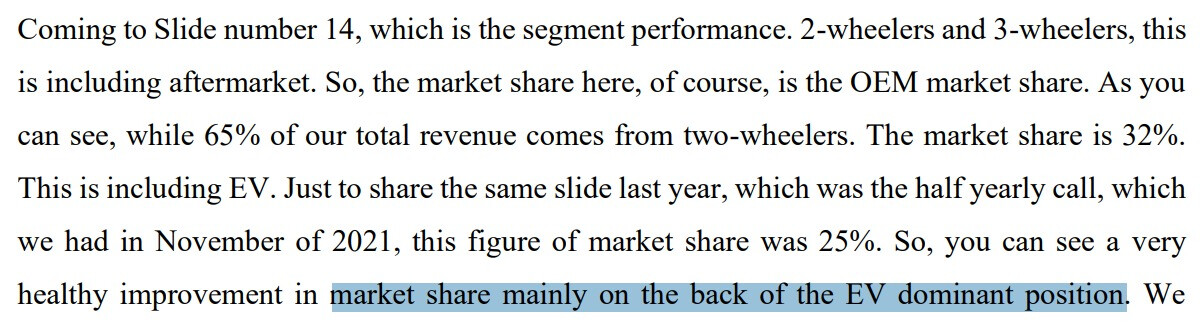

Market Share for 2W & 3W segment which was 25% last year has now increased to 32% mainly on the back of EV dominant position

Gabriel has been heading south daily, even though there is so much inherent strength. Ola front fork recall is negatively perceived as it appears to be. Ola recall is in a way a positive development, since the new strengthened front fork is developed in record time. Ola electric is gaining more momentum. Over the next few years, Electric portfolio can give a big uplift for Gabriel. Gabriel is way undervalued w.r.t its capability and corporate governance. Once the current turmoil in the market settles (may take longer time) Gabriel will be marching forward, ahead of the pack! After market sales alone can cross 1000 Cr turn over in another five years. So there multiple reasons to stay invested.

Disc: invested.

3 Likes

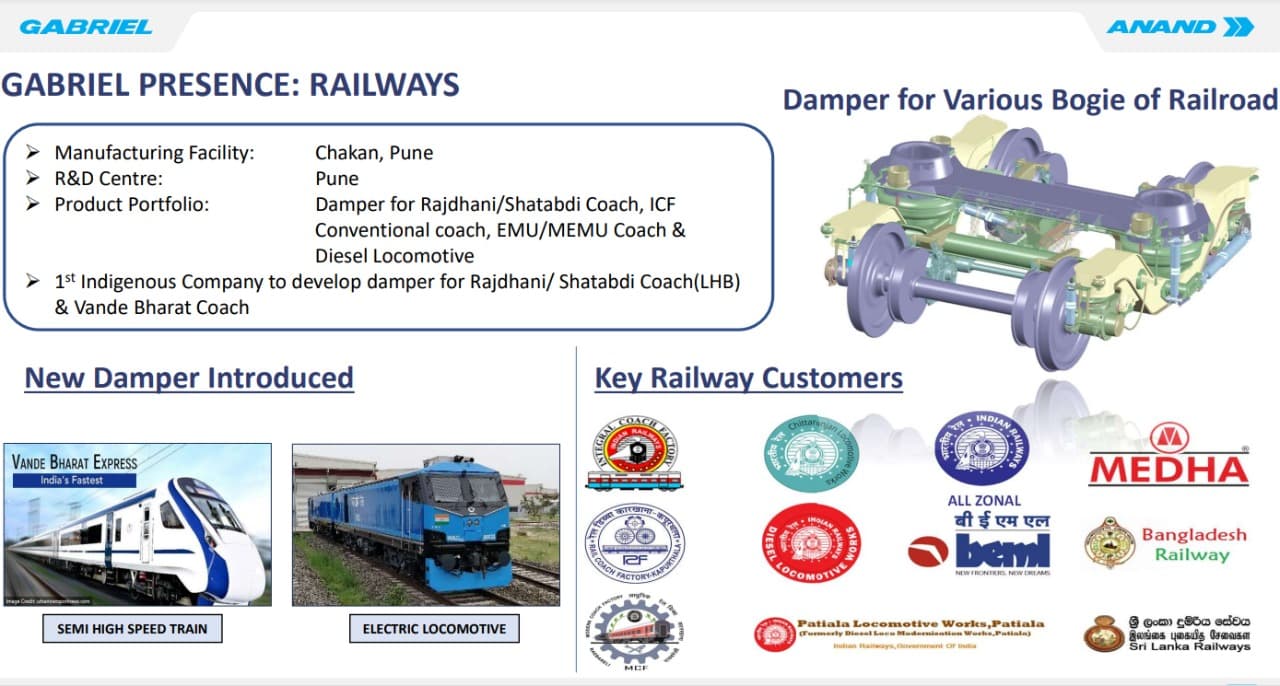

was gabriel the sole supplier for the suspension and forks for ola? or was it just a general over reaction of the market? i am also optimistic about the co’s prospects and looking to add at current levels. Also their railways business is another interesting trigger for growth

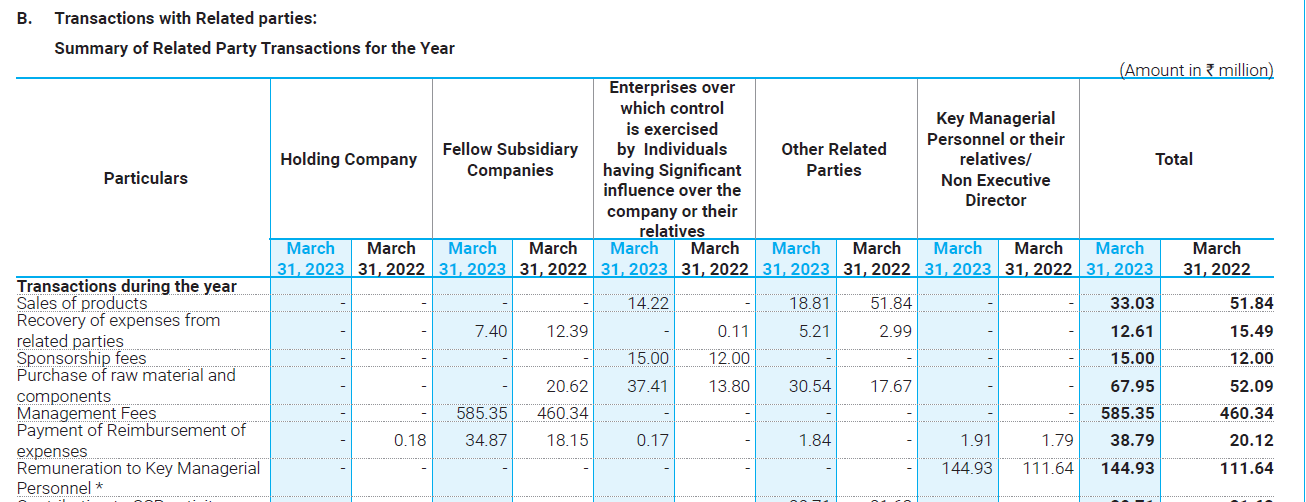

The new finance bill has doubled the tax on royalty - For gabriel that should have minimal impact, assuming royalty is paid to the us partner (1.55Cr). The bigger management fees, the legal and professional charges (52.133Cr) are actually paid to the Anand group which is an Indian entity. So over all impact should be less. Ola recall impact should be done, its only short term as the ability of Gabriel India to provide a redesigned front fork in record time is a good thing and Ola is likely to remain a customer. General market is tight with the liquidity tightening and interest rate shoot up(and its effect on banks and other institutions) in developed markets. So pressure on share prices may continue for some more time, while market waits for more and more signs of disinflation in developed markets. However, I repeat w.r.t its capabilities corporate governance (except for the way the management fee is collected) company is solid and well poised to grow faster in coming years.

Disc: invested.

Company made partnership with inalfa for making 200000 sunroofs plant. It’s 49-51 partnership. Avg sunroof price 30k. 2L sunroofs will fetch 600cr revenue. Out of which 300cr belong to Gabriel. Current sale 2200cr approx. this sunroof won’t aid much in incremental sales growth. Any huge impact on eps because of this. I don’t feel so. Views are invited.

4 Likes

After Inalfa sunroof JV, Gabriel is looking for another big ticket acquisition/venture as per the last con call. With a possibility of margin improvement and further export growth possibilities, stock should be able to cross the resistance zone pretty soon if the market conditions remain favorable. After a long consolidation Gabriel stock is poised for a secular up move into uncharted territories. ANAND group has put special focus on their crown jewel Gabriel this year. Lets see how it all add up and reflect in the share price.

Disc: Invested.

3 Likes

Growth and margin improvement are happening at the same time. If the management is able to deliver on the double digit margin with growth, stock can trade in four digits in a favorable market. Currently the company is on track aided by the strong positioning in the UV + EV and the after market segments.

Cheers to the management for the efforts.

Disc: invested.

Can anyone explain the nature of management fees paid to fellow subsidiary companies amounting 58 cr? Thank you.

2 Likes

True, there has to be a better way to collect the management fee. The management was certainly contemplating one, hopefully they will implement it.

Disc: invested

@JJu, @Prateek_Dugar what you think about the valuations now for GABRIEL?

Do you think there will be headwinds ahead for a timely correction? or you see tailwinds?

I had exited the stock due to 40% subsidy cut by government to all EV : this would put pressure on sale → going to low volume and low demand.

Any thought is highly appreciated

1 Like