Given company is doing public concalls, frankly i dont see point of 1:1 discussions. Why not join next Q concall & ask company whatever you want to? Let whole world know the answers.

3 Likes

Sure we can. but dont want to wait until then, that is the main reason i was trying for an early one.

Company started con calls just now, not sure if they will do it next qtr as well. Also, we might not get enough chances too… analysts take much of the time, number of questions will be limited too.

But yes, we can use the qtr con call definitely.

really good thread. And thanks @johnsgeorge.cet.

1 important thing to check…promoter holding is reduced by -15%…NOT GOOD ![]()

anyway stock is near ATH and awaiting to correct…definitely not a buy at CMP. Let it cool at least 30%.

PE is OK .

In SME cos…I look for 4 things

1> Promoter must be hunger for success.

2> Promoter SHP near 60-70%

3> if having big client as in this case…is good… as Reliance, BMW must have done due diligence…

4> BUY only during consolidation… never buy at peak… I did same mistake in CHEMCRUX…but i learned it…

what’s others say… Dis- not invested…but looking to invest…

Thank you @kumar010203

The reduction in promoter holding is due to the preferential issue for raising funds, promoters have not sold their stake.

6 Likes

thanks @johnsgeorge.cet . do you see fall in near term …ahve you invested… what’s your criteria for going for micro cap biz…

I might not be the most qualified to comment, still learning the art ![]()

Anyhow, to answer you from my viewpoint, for such small companies, it depends upon your destination - if you are looking at long term, returns like 10x or 50x in say 10 or 20 years, the buying valuation is not as important as we think. 10x is 1000% total returns, a difference of 25% or even 50% here will not be of a great deal.

Just to take a random example:

300Rs stock doing 50x in 20y is 22% cagr.

But same stock bought at 600Rs, cagr will still be 18%.

This is assuming the microcap in question is capable of pulling a long haul - buying right - which is a different topic in itself.

However if you are looking at short/medium term, returns like 50% or 100%, then yes, you must buy it cheap. Especially because we cant say whether the particular stock or market will fall in near term.

I have not bought Focus yet, not waiting for price correction but mainly to know more details about the concerns i have, which I mentioned earlier in the thread like corp structure, market leadership claims and so on.

6 Likes

Criteria for microcaps, let me try to summarize a few points:

- Long runway - either under penetrated market or fast growing market, with the company growing faster than the industry.

- Improving margin profile, ROCE and ROE, Stable or Improving Debtor days and Inv days. (In short, improving leverage)

- Growing without need of debt.

- Right capital allocation

- Honest, capable and passionate management - I think this must be given the most importance, to be able to bet big on a stock. Smaller the company, the more important it is, more than the numbers.

6 Likes

Methedology

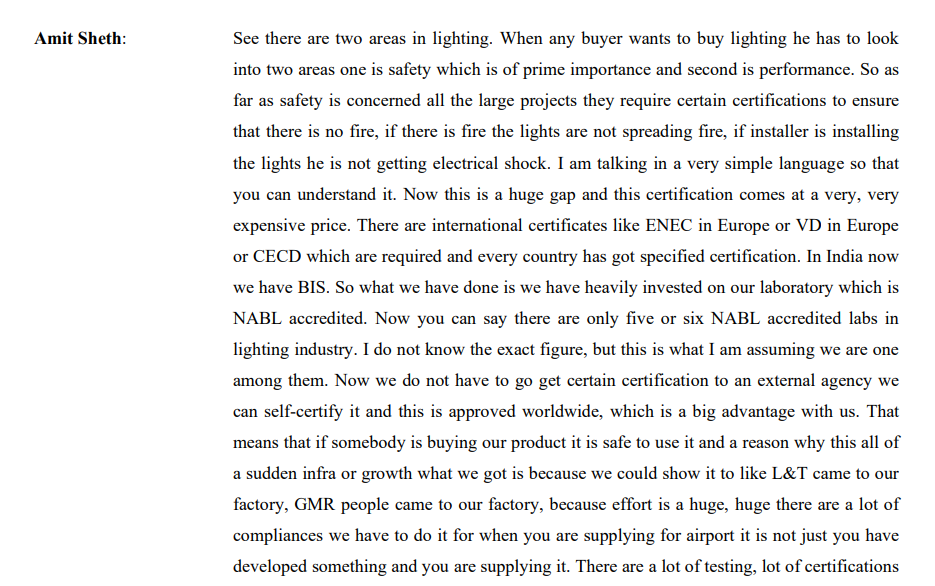

Focus talked in the concall about one of the competitive advantage being nationally accredited testing laboratories

The reason this is important is so that large reputed customers like GMR, L&T, jockey would want quality & some assurance of the same.

202206060949-NABL-400-doc.pdf (3.6 MB)

Above is list of ALL NABL accreditations from 2022

link: https://nabl-india.org/nabl/file_download.php?filename=202206060949-NABL-400-doc.pdf

we can see Focus’s NABL accreditation here for Electrical & Photometry.

Now there are 42 companies which have telemetry instruments (400 odd for electrical). Most of these are testing & instrumentation companies & so not competitors for focus. I went through all 42 to find possible competitors for focus (based on pricing, quality, target cistomers etc, they may or may not be competitors in reality)

Potential Competitors

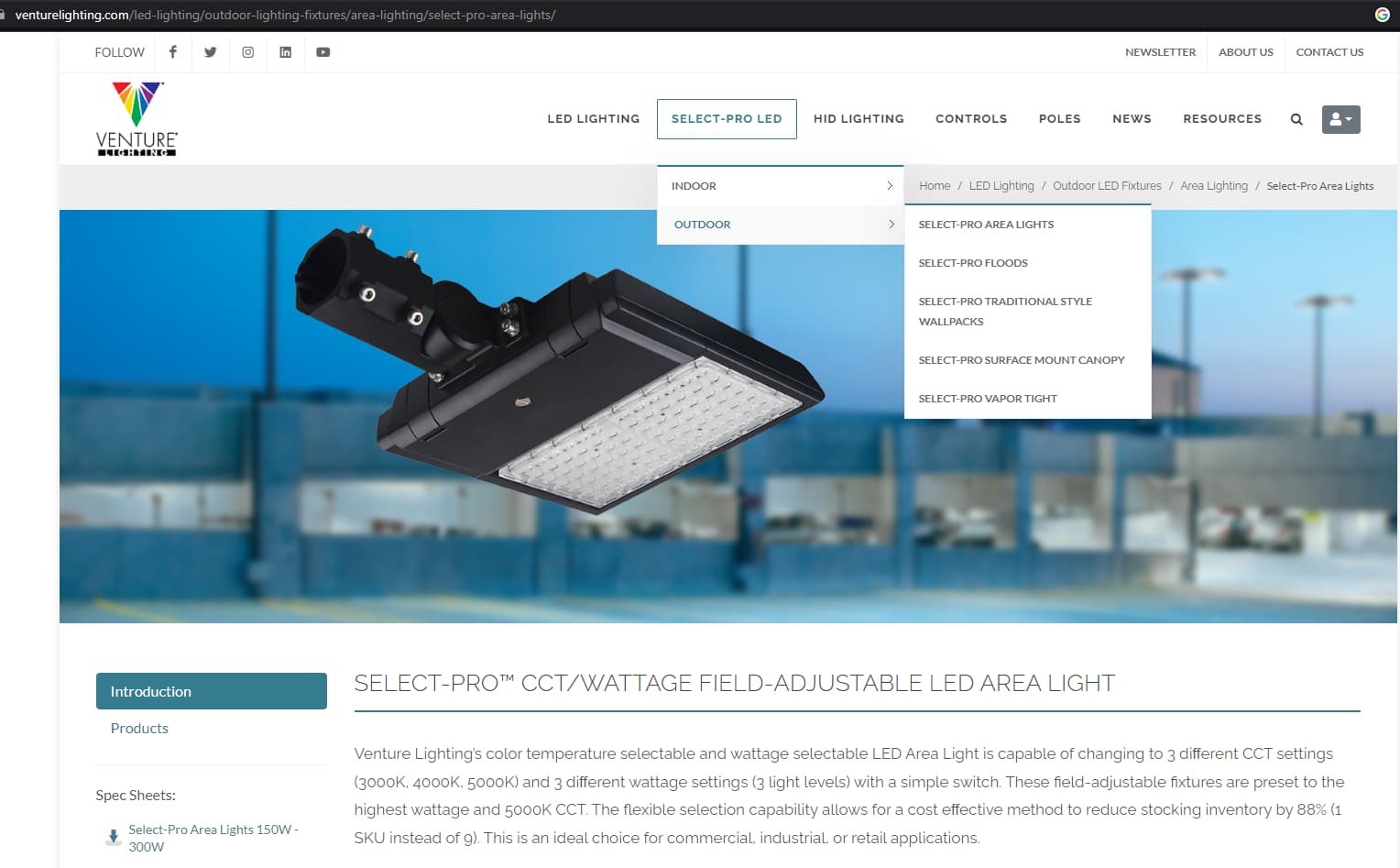

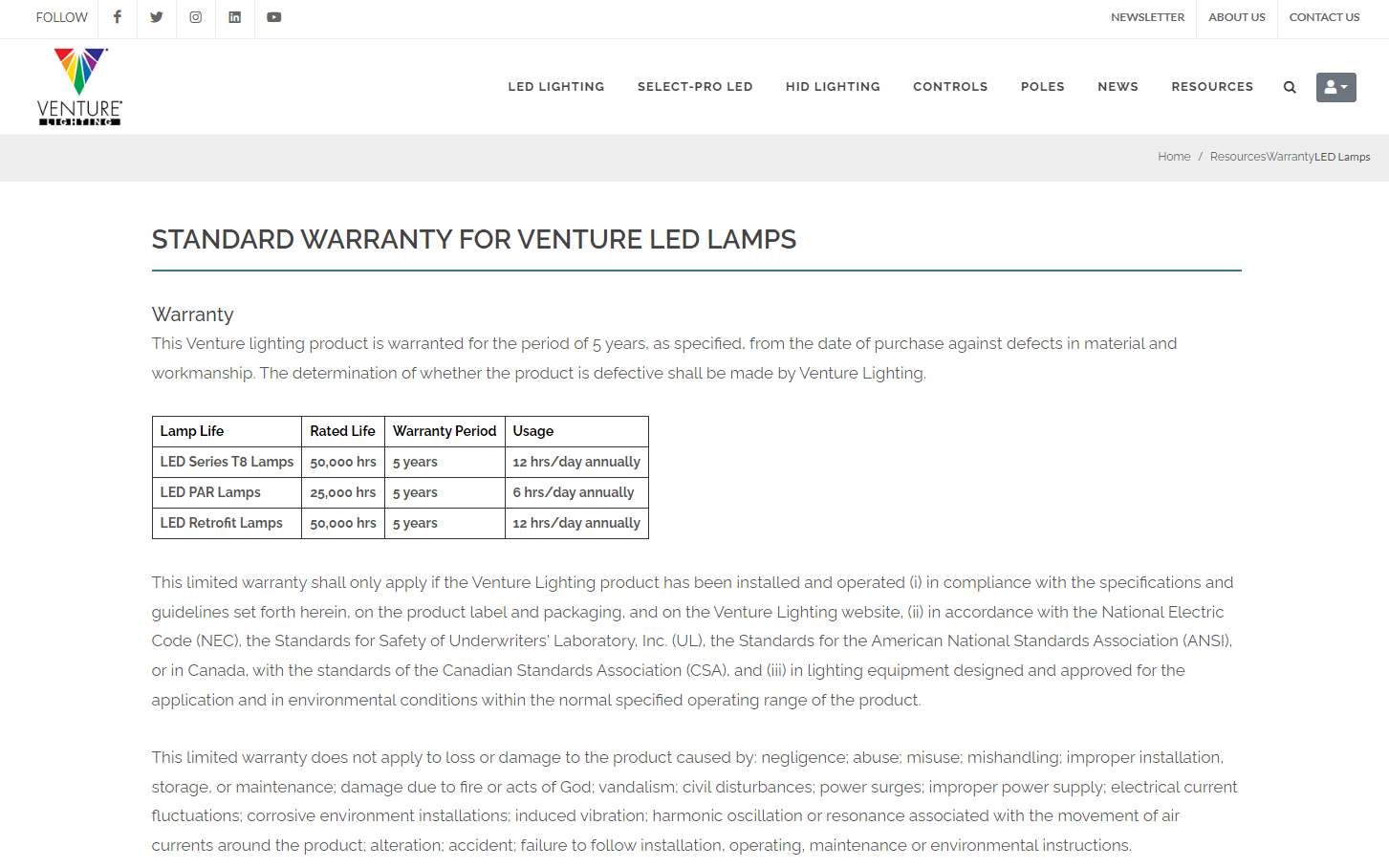

Venture lighting

Venture seems to provide 5 year warranty for their products & to that extent seems to be of good quality.

Venture also has focus on Outdoor lighting (seen from website)

Interestingly venture is also HQed in Ohio, USA so is an MNC competitor (hence needs to be considered a serious competitor & studied more deeply).

Lighting technologies

Lighting Technologies is also an International Manufacturer and Supplier of lighting solutions.

Focus on outdoor lighting is visible.

Gupta power infra

Seems a bit more diversified than other 3 companies. Gupta Power Infrastructure Ltd is a into manufacturing array of Cables & Conductors. Overhead Conductors, HT-LT Power Cables upto 66 KV, Instrumentation Cables, Mining Cables, Thermocouple Cables, Airfield Lighting Cables, Railway Signaling Cables & Specialized Cables. With its own EPC Division, GPIL provides. I would not be surprised if lighting is not a focus area for them.

https://www.linkedin.com/company/gupta-power-infrastructure-limited/about/

They do seem to be present in industrial lighting, commercial lighting etc but couldnt find too much on website on this. Mostly focused on Wires, cables, conductors.

Non Competitors

Interestingly i am not counting surya roshni as a competitor since it only has photometry accreditation but not electrical.

surya is listed btw but lacks focus imo, no pun intended).

Varroc:

Though varroc has both accreditations but we know that its focus is on auto sector, so i am excluding it from potential competitors list.

Fiem:

Fiem doesnt have electrical accreditation & focus is on Auto (fiem investors should take notice that it doesnt have electrical accreditation)

Wipro:

I think a lot of us have used wipro products. It is clear though that they also, do not have electrical accreditation

Signify:

Signifty is phillips. We know that signify/phillips focus is primarily on end customer segment with lower value, quality & shelf life. It has its pros & cons. Due to this focus it is more akin to an FMEG manufacturer. Whereas Focus is closer to a Capital goods provider (where quality & economic value much more than brand).

I could only find 3 potential competitors who have both accreditations. This is definitely interesting. I will try to dig deeper into all 3 by visiting their website & downloading their financials.

Overall interesting stuff. 2 MNC. 1 local competitor who might be diversified. Need to do more due diligence on all of them.

Disc: Invested, biased

14 Likes

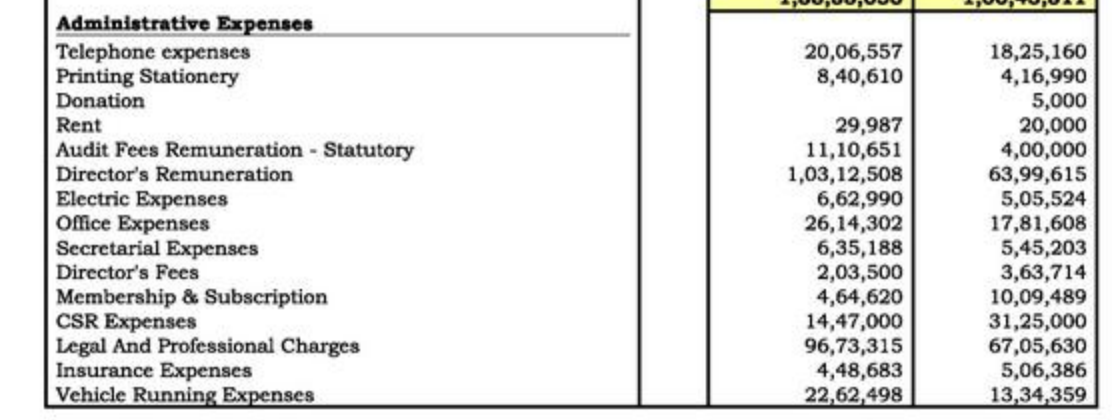

Hi Sahil

I noticed one Red flag in their Annual Report:

Auditor’s fees has increased 3X (4 lacs to 11 lacs) from FY21 to FY 22.

Maybe this needs to be clarified by the management on this generosity shown on their Auditor.

Disc : Invested since last two months with good position size (> 20%).

Hi all,

The quarterly call or the conf call we requested is nearing, sharing my remaining questions/concerns here. I have sent it across to the IR, will update here if I get any response. Otherwise, will want to get these clarifiied on the call.

If any of you have any inputs, please feel free to add.

1. The above table shows the fixed assets (property, plant, machinery) and capex data as per statements.

a. During 2018 to 2022, there was a capex of 27.5 Cr but gross block addition was only 19.4 Cr. There were no intangible assets added too. What was the extra 8Cr capex spent for?

b. Also, heavy capex of 27.5Cr has been spent for plants - I suppose it was for the Bhiwadi and Ahmedabad manufacturing plants/lab - which is sufficient for future growth, as per your recent interview. Then what was the need for the preferential issue of 31.4Cr in 2022? What will this capital be used for? As per the IR company Kirin, this amount is used to expand R&D team and so on, however why such a big amount for R&D team? If it is for any other purposes, please elaborate.

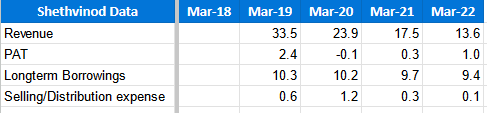

2. Shethvinod has the same directors - Amit Vinod Sheth and Deepali Amit and Vinod Tarachand Sheth (Who i assume is Mr. Amit’s father) - then why keep it as a related entity, why not merge or bring under Focus as a subsidiary?

3. With reference to Sethvinod financial statements pasted above (got from Tofler.in):

a. Looking at Shethvinod financial statements, I see there is a Net Profit of amounts like 1Cr, 2.4Cr etc. Had Shethvinod been inhouse manufacturing unit, Focus Lighting would not have spent this amount. Similarly, there is a selling/distribution expense and other misc expenses like Auditing fees, which would not be needed also. How can you then say this arrangement is in the best interest of Focus lighting company and the shareholders?

b. There is long term debt in Shethvinod balance sheet, does Focus Lighting have any relation with this debt?

c. Also, had Shethvinod an inhouse manufacturing facility, its assets and liabilities will be on Focus Lighting’s balance sheet, which will be different from the current state. Is this in the best interest of Focus Lighting share holders? (For example, more property/plants will increase fixed assets, debt of Shethvinod will be in Focus’ balance sheet, which then cant say a company without debt and so on).

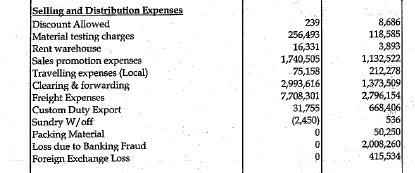

Screenshot of Other expenses from 2020 report of Shethvinod:

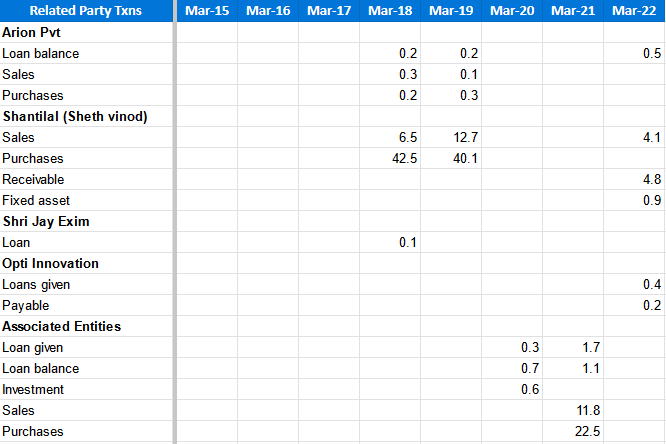

4. Related Party Transactions:

a. Why is there a sales transaction with Shethvinod. It is the manufacturing unit for Focus, why would Focus sell anything to Shethvinod?

b. When a sale transaction through Shethvinod is recorded, how does the auditor verify if it is a legit sale to an end customer, considering that Shethvinod is not audited as it is not a subsidiary? (In the case of direct sale or sale via a subsidiary, there will be invoices from end customers which the auditors can verify.)

c. There are substantial amounts of loan given to associate entities like Arion, Shri Jay Exim, Opti innovation. Even though going by your previous response that this was given to help with their capital needs, why is Focus Lighting obligated to do this with an associate company? In what way these companies help or add value to Focus lighting that necessitates this hand holding? Why is this in the best interest of Focus Lighting and its shareholders?

Disc: Not invested

9 Likes

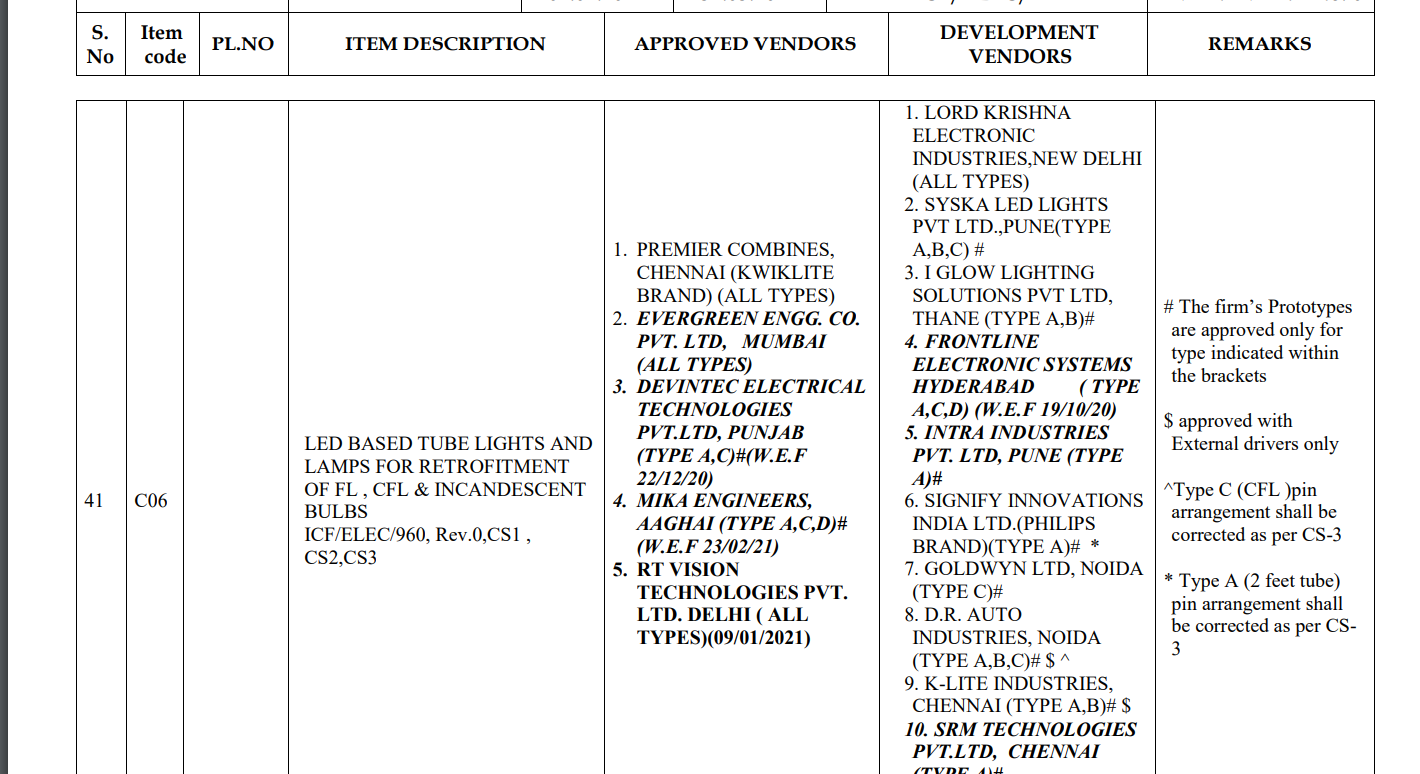

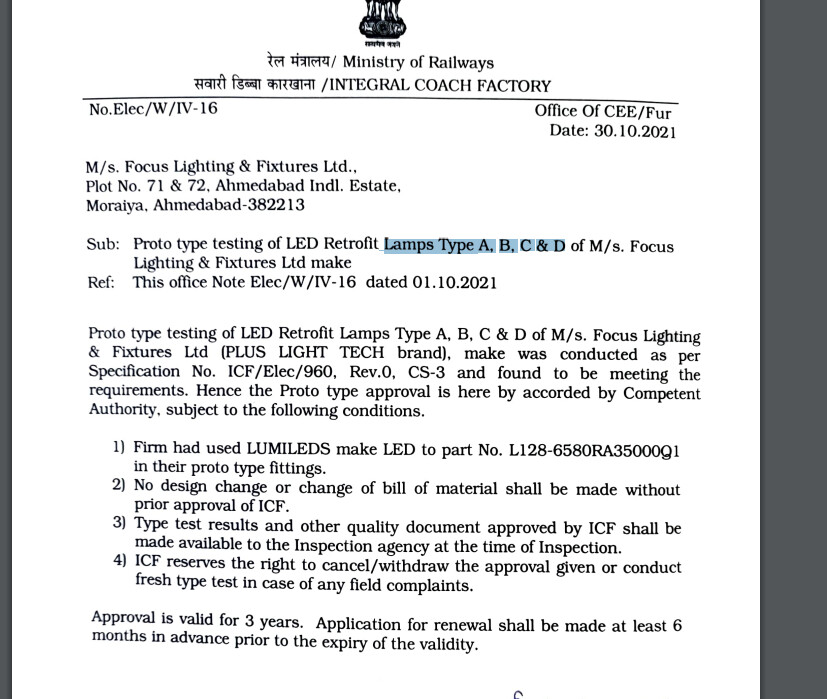

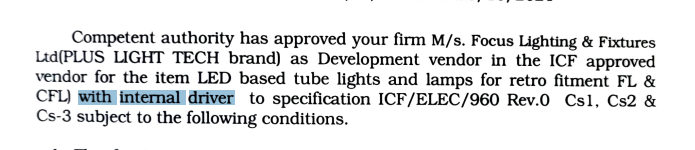

Some capability points

Focus was empaneled with ICF (Integrated coach factory) for LED supplies per mgmt as development source, here is the certificate

here is the list of both approved and dev sources for same product category from https://icf.indianrailways.gov.in/uploads/ICF%20ELECTRICAL%20VENDOR%20LIST%20VER-14.pdf (there would be revision of this doc as focus was added in october and this list is from April - point here was capability side)

and here is the screenshot for focus

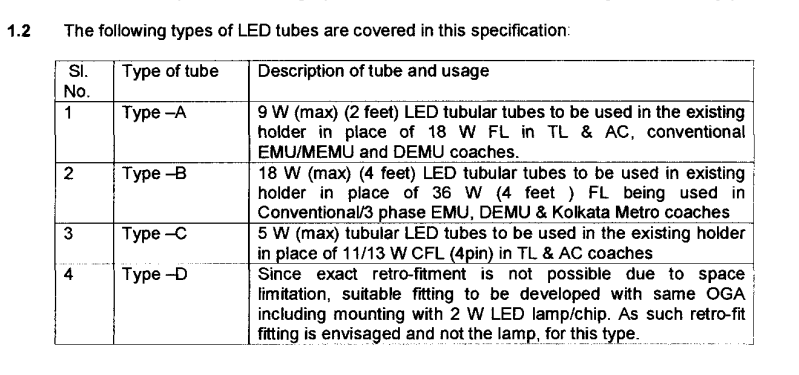

If we see both doc - focus is across all categories - A.B,C,D - where as we can see some known names like Syska, Philips, Kilite are supplying only subset of these categories.

Also for Klite (comparable peer in thread) has external driver per screenshot, where as focus has its internal driver

these are cursory findings and sizable revenue kicks in from railways once they are upgraded from Dev to approved source (due in may 23 per last con call) - it does provide us with validation of mgmt claim + tech capabilities. It also tells that there is competition warming up given lot of names in Dev category.

Folks with better understanding of ICF LED categories and vendor shortlisting criterion know how can further enlighten rest of us ![]() , or something we can ask mgmt during upcoming concall.

, or something we can ask mgmt during upcoming concall.

some more stuff on categories - D seems difficult and Focus seems only among few - high level observation

D : Invested

7 Likes

Has anyone here received the annual report from the company?

Results are out. While sales/PAT growth are impressive, Inventory shooting up, no cash flow.

Cash flow statement shows a preferential allotment of 31 Cr. Another dilution?

https://archives.nseindia.com/corporate/OutcomeofBMwithResults_03052023190929.pdf

Absolutely not time for this - was the reply from Focus this time for my questions. Hope to get these clarified in the call today.

Who else is joining?

Here is the invite, you can register in the link there.

Focus Ligting & Fixtures Limited Q4 FY23 Concall Invite.pdf (252.3 KB)

1 Like

What is your takeaway from the concall?

Any question diverted to the CFO goes either un-answered or insufficient details shared in the concall which I found very disappointing.

1 Like

The promoter aims to persuade the investors by highlighting the following key points:

- Our performance should not be evaluated solely based on quarter-over-quarter (QoQ) measurements. By focusing solely on short-term performance fluctuations, the true potential and long-term growth trajectory of the company may be overlooked. It’s important to consider the broader picture and assess the company’s strategies and prospects.

- Similarly, our performance should not be evaluated solely based on year-over-year (YoY) measurements. Annual fluctuations can occur due to various external factors that may not reflect the underlying strength and potential of the business. Investors should consider the company’s long-term growth plans and overall market trends.

- If an investor is primarily focused on short-term performance and expects immediate returns based on QoQ analysis, this may not be the right stock to invest in. The company’s value lies in its long-term growth potential, and investors should align their expectations accordingly.

- We have a strong growth projection, with the potential to achieve a topline (revenue) of 400-500 crore in the financial year 2026-2027, compared to 162 crore in FY23. This demonstrates our commitment to expanding our market presence and capturing a larger share of the industry.

- We are making significant progress in becoming an approved source for the Railways, which would provide us with a substantial competitive advantage. This achievement would position us to secure over 80% of the Railways’ business, and we anticipate completing the approval process within a month.

- Our strategic focus is shifting towards expanding our manufacturing capabilities and reducing our reliance on trading activities over the next three years. This move aims to enhance our control over the supply chain, increase efficiency, and potentially improve profit margins.

- We are dedicated to investing a significant portion of our revenue, precisely 7-10%, in research and development (R&D). This investment underscores our commitment to innovation and the development of new and improved products. In the current year, we are targeting 10% of our revenue for R&D, with the possibility of increasing it up to 20% in the future.

- The promoter personally oversees product development, which demonstrates our hands-on approach and commitment to delivering high-quality solutions. Recently, the promoter spent a month in Europe, engaging with various companies to gain insights and explore opportunities for introducing innovative solutions to the Indian market. This proactive approach ensures that we stay at the forefront of technology and customer demands.

Investors who recognize the long-term potential of our company and align their investment strategy accordingly will be well-positioned to benefit from our growth trajectory and strategic initiatives.

(invested)

12 Likes

The answer was pretty clear: There will be cash flow issues in the future too since payments are on a weak wicket due to exposure to Govt in infra lighting space.The major point was that being a 170 cr company,they can still take on orders as large as 100 cr at one go.A huge rock on a light boat rocks the ship & can sink it,just like a heavy order for a co. of Focus’ size can.So,the promoter said while OCF could remain in bad shape,they will be able to manage WC in a way that it doesn’t sink the company & thus gain higher scale in the process.

Disc.: Invested.

10 Likes

This point is, still in the possibility zone, right ? 60 days is the normal payment cycle. In Infra, IF they take a 100 cr. project, of course it’s going to lead to cash flow problems. Right now infra share in overall revenue is 7.5-8%.

We can take the 12 odd cr. Surat project’s payment schedule as an example. Where 40% of the payment comes after a good chunk of work (Sl. No. 3) is done and another 45% after some important but light work like system integration etc…

I thought the possibilities on the Railway side was interesting.

Key takeaways on Railways : Current year business 1.18 cr. Expecting to get 15-17 cr. this year (FY24), but overall we see potential that in 2 years we can get 70-80 cr run rate. Approved sources margins are 30-40% more than development source margins. Cash Flow: ( Banks ready to discount the PO by ~90%, so cash flow is not a problem for Railway projects.). Development vendors have to do min. qty to qualify for approved vendor. We have developed 16 products and got approval for all of them.

5 Likes

yes hence no guidance in the concall. I chose the number as an example given their revenue base & to drive home what the management said.

The company mentioned that the Indian Govt is seriously looking at creating a world class railway system including quality lighting.As such the opportuninty is a mega,multi-year one.Even at 70-80 cr in 2 years we might still just be scratching the surface.

5 Likes

While we as investors have a way/expectations to look at performance, it would be worth to see promoter perspective and then validate two to see if there is synergy

There are broadly two sets of biz segments - established with good growth(retail B2b, exports etc ) and emerging with exponential growth (Railways and infra etc)

- Focus has been predominantly a retail(B2B - showrooms etc) focused co - FY 23 at 60%+ revenue( this was majority part in FY 22). This is supported by credentials, financial hygiene and a well oiled engine to generate predictable growth - if promoter were to pursue only this track - most of challenges will go away and we get a 20-25% CAGR biz with decent margin, cashflows etc.

-

Railways - seem to have two parts and promoter is quite bullish in tnear term(supported by sector tailwinds)

---- Standard tender based bidding they did sub 2 cr in FY 23(at 20% so 10 cr tender win) - FY24 at similar win rates but at 80% they aim to do 20 cr type (at 80% need 25 cr tender win as approved vendor) - logical to assume Q2 onwards when developed vendor approval comes.

----- Exploratory - IoT based solutions - could be large but lets leave it out of calculations for now - - Infra - this is the vertical which is making all lumpiness and also presenting enormous potential, they have done delhi ariport and two projects like bade baba/surat fort in hand (together ticket size near 30 cr) - mgmt intent is clear that ticket size will only go up and they are prepared for cash flow impacts.

This is a high growth story where jockey wants to run show its way and not be judged for v short term in return for mid term potential (akin to PE space), will have spikes to an extent where mgmt itself cant predict near term.

Would be watching out for (note below are pure speculation basis FY 23 base and base growth 20% in existing biz/mgmt guidance)

- Railway Dev approval, wins and rev run rate (Q2 onwards) = 20 cr FY 24

- Retail and exports run rate and margins (Fy 23 base of approx 125 cr together) = 150 cr+ FY 24

- Infra - Current order execution (Temple + heritage fort) + new wins quantum and WC = 30 cr+ ?

there is no doubt that stock has had one way move from 100 to 800 type and euphoria post Q3 call, and a 31% fib retracement puts it at near about 580-600 level - will also bring valuations closer to 750 cr/ 32X TTM basis or 23 X FY 24 basis (going by mgmt claim for 30% growth). Not cheap but not overvalued either for high growth.

D - invested and could be wrong in assumptions, mgmt may surprise on upside given optionality or struggle in cashflow /execution given nature of infra biz(though they know what they are getting into), heavy R&D disproportionate to size of biz is another risk

15 Likes