Looks like Fine organics is being added to Rising Giant of Marcellus.

It was already present under LCP.

2 Likes

Where did you find the company concalls?

My bad, I meant company’s interviews and any other company vid interactions I could find. This business doesn’t hold any earning calls AFAIK.

1 Like

An interesting thing about this stock is that irrespective of market conditions, since 2018, the price of this stock consistently moves in an upward trajectory. Even if it dips, it goes back up very fast. It seems to be highly rated by the market. Is this because of the nature of its diversified business i.e. specialty additives for foods, plastics, rubbers, paints, inks, cosmetics, coatings, textile auxiliaries, lubes and several other specialty applications? Given its relatively smaller market cap, it might have a long way to go in the future. Can anyone tracking this diligently, throw some light on future prospects in terms of whether it can sustain its revenue, ROCE and margin growth over the next 5 to 7 years? Thanks.

4 Likes

Hi, one of the reason for the consistent up move is the low float of stock available for the retail investors.

Otherwise the business is great but available at premium valuation.

Regards,

Dr. Vikas

2 Likes

Good critical product and caters to the essentials category. I think this is the main reason. Low float doesn’t guarantee earning though

1 Like

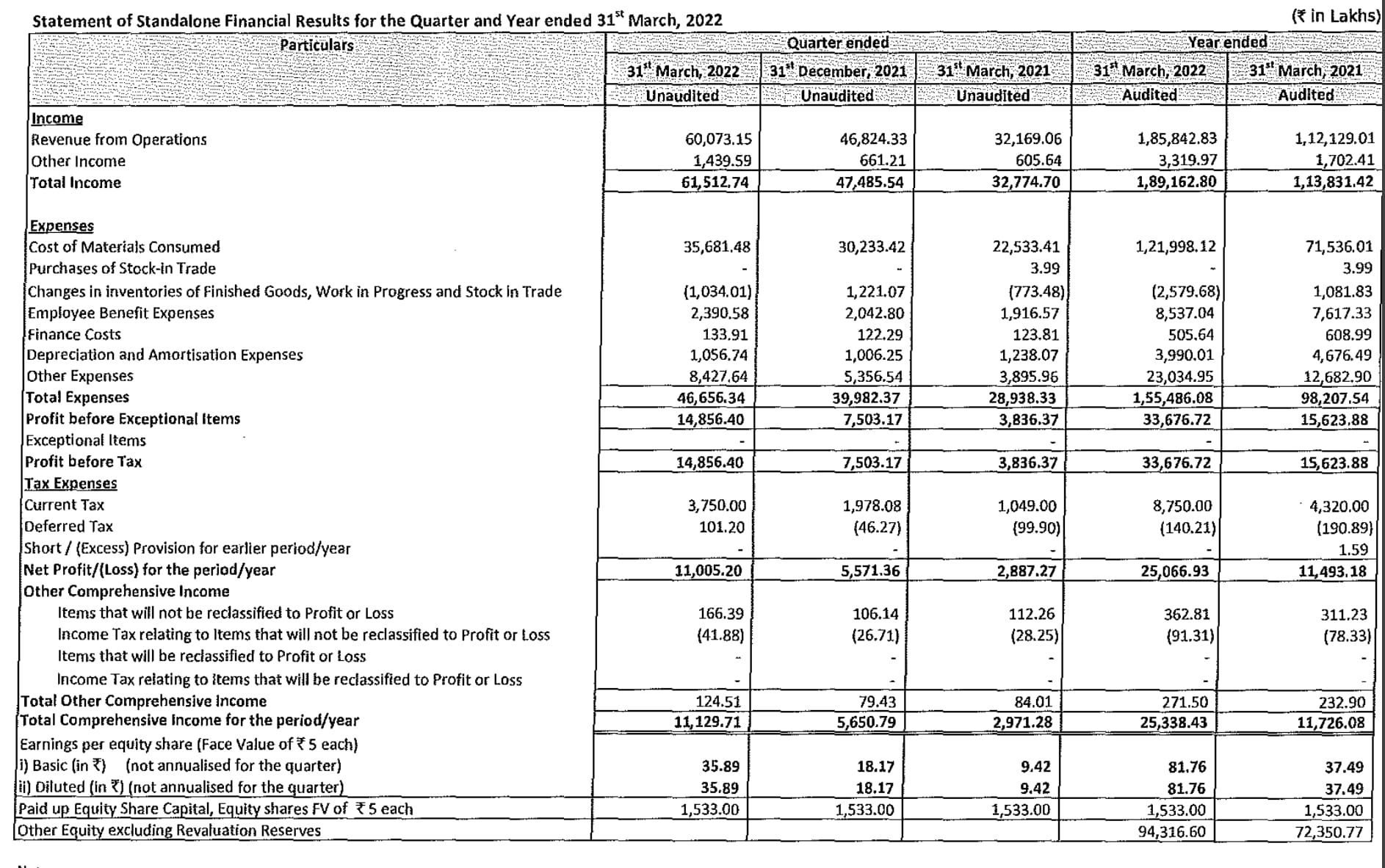

Yes, truly an exceptional quarter from Fine. I had anticipated great growth from them due to operating leverage kicking in, but truly speaking this surpassed the best of my expectations. In times, when all B2B businesses are facing margin contraction, Fine has shown 9% EBITDA margin expansion this quarter, that too when Palm oil prices are hitting ATH. Management has shown their capabilities, and this should justify some of the high valuations this company gets. As Management says, new factories goes to 100% cap utilization in 3-4 years, I think we should see a few more quarters of revenue growth, however margins may contract a bit going forward.

Disc: Invested since Dec 2020.

7 Likes

Indeed great set of numbers. Need to understand the driving factors for this sudden growth. Not sure if this run rate is sustainable?

Discl: Invested at lower levels.

Have I read it correctly that inventory and trade receivable have doubled yoy ? Do anyone know why ?

1 Like

Trade receivables jumped 87% from Mar 21 - Mar 22. However, the Receivable to sales ratio for Mar 22 is 16.1% and the same ratio for the company since 2017 was between 14% to 17% since March 2017. So there is no big variation when u consider Rec/Sales ratio.

Secondly regarding Inventory growth, i would read it along with Sales Growth. For a sales growth of 66% and inventory growth of 87% seems to be normal.

These are my observation. Hope it is useful. Thanks

3 Likes

Fine Organics is under Marcellus LCP portfolio

SBI Small cap MF

Axis Small cap MF

Looks like the float is also low. Thus good results might return a lot of +ve price movement

2 Likes

I don’t know what to say now. ![]()

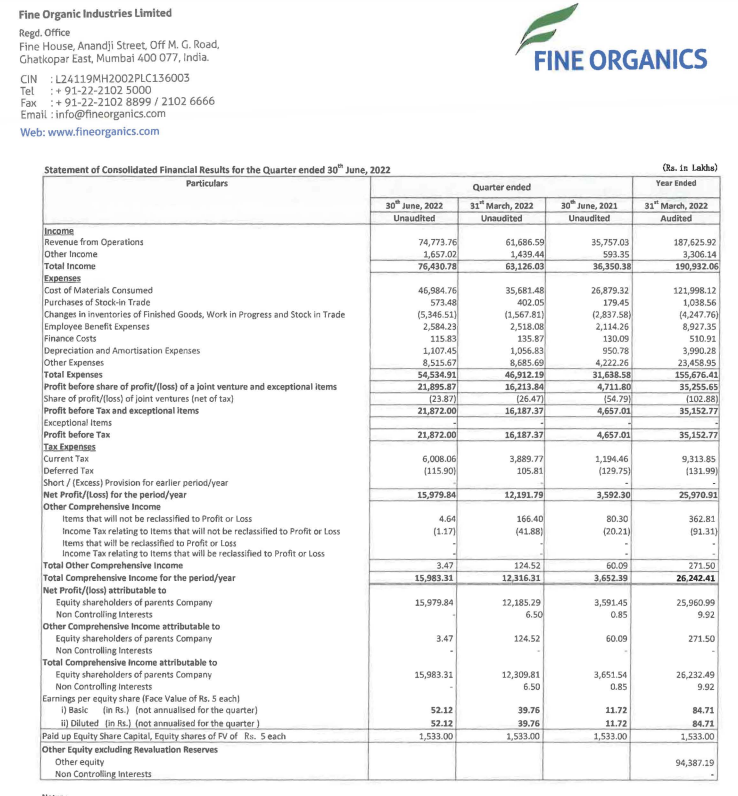

Management has pulled another super fine rabbit out of the hat this quarter. Way beyond my expectations once again.

Disc: Invested since Dec 2020.

4 Likes

Fine organics AGM :

Chairman speech :

We continue to face the challenges brought by the macro economic factors such as cost inflationary challenges including logistical costs.

Globally the trend is to adopt more ecologically friendly products as people become more conscious about the need for environmental preservation. Green chemistry-based products are becoming increasingly important in today’s rapidly changing environment. Consumers are transitioning to Green chemistry as a renewable and sustainable alternative for their products.

We, at Fine Organics, are a well-known and globally recognized Company in the area of green performance additives. Our value creation strategy operates in an environment influenced by both internal and external factors.

Today we have a wide range of specialty additives created from oleochemistry, used in foods, polymers, personal care, coatings, feed nutrition and many other applications

Our manufacturing facilities are at Ambernath, Badlapur, Dombivli and Patalganga, allowing us to deliver in around 80 countries through our offices in U.S. & Europe and over 180 distributors to our more than 5,000 end users. Our unique offerings for our customers across the globe, backed by prudent R&D capabilities.

Innovation is a back-bone of the Company and R&D is a continuous process in our Company. Our strong R&D and innovation capabilities has allowed us to deliver FINE solutions to our customers. We have team of more than 20 Scientists and technicians. Our R&D spend is less 1% of our total revenue because our R&D is more of knowledge intensive than capital.

We are glad to share that we could manage to operationalise the second phase of our Patalganga Facility as per targeted timeline, which is catering to growing Indian food industry. We have also formed a Joint Venture Company in Thailand which will help us in expanding our product basket and further strengthening of our global presence.

We intend to further increase our production capacities by putting up a new plant in Gujarat for new and existing product lines with process improvements and technological upgrades.

The supply chain disruptions and input price volatility hit the company’s profitability in the initial half of the year. But our commitment to service customers at the contracted price allowed us to strengthen our existing relationships. To tackle the volatile environment, we restructured our business model and aimed to engage into shorter-term contracts with customers, wherever possible. This helped us maintain margins in coming quarters.

Some notes from Q&A :

In oleochemicals, we have 450+ products, some are highly profitable and some are less profitable

Competition : Cargill, Palsgaard, Corbion, Emery.

RM : 70% domestic 30% import

When we started green additives when market was non existent. We started making food emulsifiers no market for that. We took long to develop our own market, it turned our advantage, we taught them how to use, helped us long way. That was a mistake, too early.

Emulsifiers : when volumes started growing we didn’t have enough money, RM is vegetable oils and no credit, it is cash and carry in 3 days, difficult to manage WC cycle, converted mistakes to advantages.

1997-98 : some speciality additives in R&D. When we wanted to commercialize, we didn’t have machinery, we went to europe/US. We didn’t have money for those machines. We came back, developed own Engineering R&D, unless we do it ourselves we cannot afford

Now we require less Capex, we design own plant to suit our products, own process.

All 3 turned own advantage.

Now a big hurdle : capex for other player very large, and create own engineering capabilities.

This growth will be there as long as we expanding. Naturally the growth will come, we are aware of customers, markets, we know we can sell and then only we invest.

We have expansion plans in Gujarat. Our growth is slow and sustainable. We have expanded for sure

Fungibility : many products made in same plant but not all. Some rules act food additives plant cant be used for non food.

Focus on cosmetics : Mainly in India in Skincare.

We are coming with home care green surfactants Free of pertrochemical.

We are actively looking at new products (in Gujarat facility )

We will focus on olechemistry as of now. We dont want to go in fermentation.

RD is working on new products (some which helps in energy consumption, RD is slow process other things to be considered).

Are we focussing only on export. Till 19999 100% in india.

2000 onwards, we did some exports since no market in India. We kept on getting export market.

Last few years, 40% domestic 60% export

70% exports 30% domestic (last year).

Domestic will always be priority and hence with Indian customers we want to grow we will not short supply in India and then only export

Hence future, 60: 40 domestic : export

We believe domestic helped us grow and hence we will not be disloyal to them.

We are actively looking at capex in Gujarat, government is yet to give us allotment letter, we will inform on capex plan.

RD is backbone of fine organics. There is continuous development in RD it takes long time to commercialize 3-5 years to get approvals after development (government, country and customer), one needs patience in this business, expensive in time.

The reason for increase in quarterly revenue : Rise in Q4 and Q1 Is due to realization and some volumes.

Shortage of container across globe.

We despite challenges we supplied across 80 countries. We dont know how long tough macros will remain. We have become agile to not hamper growth

Our endeavor to sustain : 18-20% EBITDa margin.

Production capacitdity : 1lac tonne per year.

Utilization : optimum capacity

Increase in freight has increased sharply due to container shortage. Freight rates are not normalized.

Disc : Invested.

20 Likes

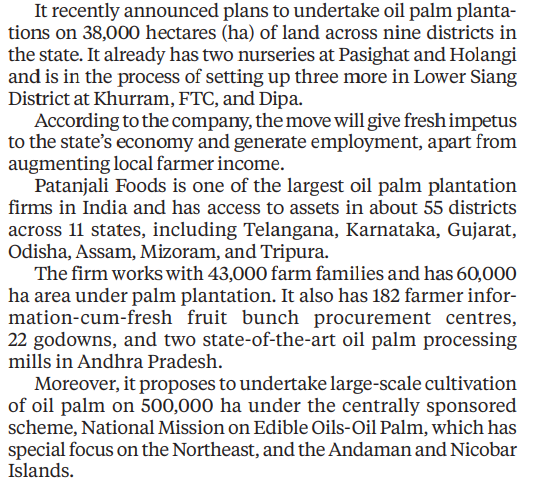

Baba Ramdev is also into oleochemicals manufacturing business,but non related …but can scale it if he intends to.It can be league of FAIRCHEM,FINE …And biggest advantages is that he has raw material sorted as he is cultivating palm on 6 lakh hectares of land allocated to it in INDIA

1 Like

With due respect, I beg to differ here. Oleochemicals is a broad class of green chemicals and can be used in several applications. I don’t track Fairchem, but for Fine Organics, their end user application and customers are different than what Patanjali may offer. Even if they can match the R&D capabilities of Fine (honestly I think it’s very hard to do) or if Patanjali mocks up their products, it takes appx 3-5 years from the customers to get the approval for the products. Fine Organics itself said in last quarter that every time they launch new products, even for them, it takes a few years to get the approval from the existing customer. This creates a lot of hassle and exit barriers for the customers as well, and deter them from choosing another suppliers. Now if these are not Himalayan barriers to entry, then I don’t know what is.

Fine Organics can surely try to backward integrate and may be their JV in Thailand is the same thought process, but their change in policy regarding spot contracts from RM suppliers and the pricing power over their customers will keep them insulated from volatile margins in future. Patanjali surely has edge in this regard, but I don’t think they can disrupt Fine anytime soon.

Disc: Invested from lower levels.

8 Likes

I hope atleast the RM could be sourced from domestic suppliers like PATANJALI once scaled up.

Sorry to ask this question, I have lost track of it few months back.

Is there any news or result for recent fall?

Is something floating in market regarding it.

Disc: Invested from lower levels