yes details of MOU are not mentioned in IP. i am planning to call company’s CS tommorrow. If you have any questions, please let me know.

from my side, i want to get better understanding of LED business. they are increasing their capacity frm 50k led bulbs to 2lakh bulbs this yr nd then later on to 4 lakh bulbs. they hav not won any major orders this yr from EESL. so want to get a sense of how they plan to utilize such large increase in capacity. do you hav idea regarding the same ?

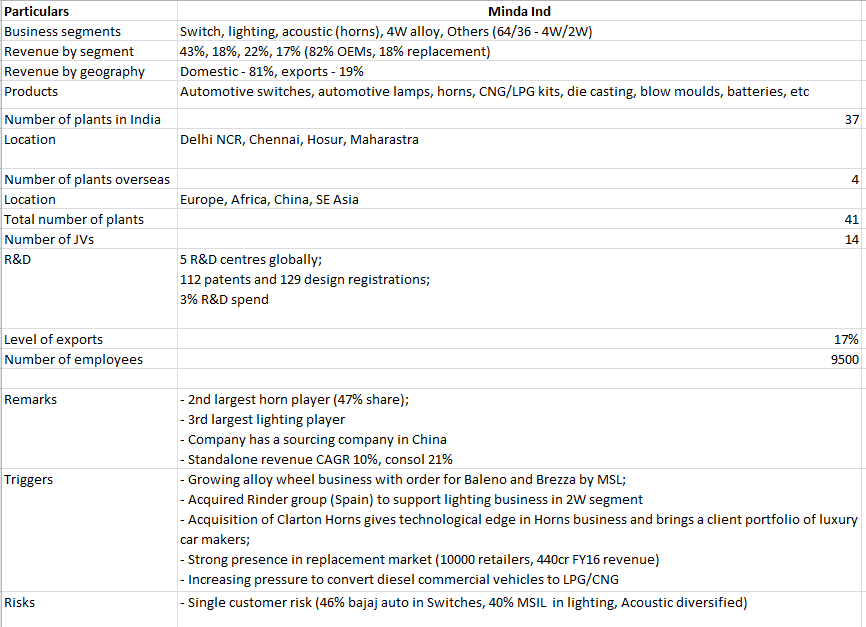

Only being a devil’s advocate here. Isn’t Minda Ind a better auto ancillary player than FIEM for a neutral investor?

Disc - I hold neither but I’m tracking Minda. I just saw FIEM’s IP and want to discuss to learn why one shouldn’t invest in Minda. Also there is no dedicated thread for Minda Ind (although I plan to start one once I’m done my research)

Agreed they don’t have exactly same product portfolio, but Minda has a better market cap and turnover at roughly equal key ratios (screener.in) in the same industry. Minda has a better global footprint with almost 7 JVs and over 100 patents. Even the product portfolio is more diversified. Infact Minda has recently forayed in renewable energy which is a different vertical altogether. The sale from exports is more and so is from aftermarket segment. The top management at Minda isn’t full of promoter family. In terms of clients, Minda supplies to more 4W OEMs but also has global OEMs in its client list, especially after acquisition of a Spanish company in lighting business.

I had prepared a table of important business indicators for Minda. Appreciate if somebody tracking FIEM could compare it to understand the triggers better.

Orders from EESL tends to be lumpy…we should not doubt the capability of company here…company must be having much insightful info about their LED business which we do not have…They will always take a planned and more conservative call…

We need to ask them about the non mentioning of other MOUs…

We also need to ask them the progress of the MOU with Honda locks Japan which has been mentioned in the IP…Till I know Mr. Jain had told that they are expecting some updates on that MOU by end of the fiscal…but no news yet…

Thanks Abhishek. will surely try to ask about the MOU.

@aashish2137

hi ashish, I havent looked at Minda in much detail. but what I like about FIEM is a) their steady margins. The EBITDA margins in last 5 years has remained in the range of 11.5-13%. I havent found any other auto anticillary company with such consistent margins. b) domestic exposure only. FIEM caters to only Indian 2 wheeler customers, which makes it a easier stock to track. we dont have to worry about performance of global auto companies and currencies.c) their LED business. the market for LED is huge. FIEM claims that it has a cost advantage over the other players. It can be also seen from higher margins in LED business. EBITDA margin of LED business is 16.6%.

Honda Motors and Scooters India, HMSI, which is the biggest client of FIEM (45% of revenues) has reported 22% increase in June sales. this is the third consecutive month of strong sales of HMSI.

TVS motors which is the second biggest client of FIEM (25% of rev) reported 12% increase in June sales.

This should provide Fiem plenty of scope to keep their facility running at high utilisation levels. Assuming an average price of INR 75 per unit, Fiem should have sold 16 mm units of LEDs in FY16. So if their 2 lakh unit per day facility can operate at a 60% utilization (ignoring the capacity addition), they should be able to sell 30 mm units this year (which should be supportable through the demand). This should lead to a ~2x growth in LED revenue. The problem seems to be that prices are dropping dramatically (see the same article). The FY16 EBITDA margin on LED is 16.6%. However, if the average realisation were to drop even by Rs 5 (which seems not unlikely based on historical trends), that margin falls to ~40% (ie 6.6%). As a result, ~2x growth in revenue will bring about negative EBITDA growth and not be accretive to Net Income. How does one get comfort around this pricing issue and the margins on the LED business?

The retail price seems to be ~4x this level, at ~230 per bulb. Is there a way to understand what proportion of FIEM’s sales are retail/non-government as compared to EESL tenders? That’s the only way I can think of trying to get a handle on this potential question around the margins and pricing in the LED segment.

strong Aug sales from top customers of FIEM. HMSI reported 25% increase in sales while TVS reported 21% increase in sales. this two customers contribute 70% of sales.

FIEM has informed BSE that they have signed MOU to set up JV with Su Kam Power systems for the purpose of selling and marketing of LED lighting products.

This is a positive development as it will help the company to sell LED bulbs in the retail market through the distribution network of Su Kam. This JV can help FIEM utlizing its increased capacity of LED bulbs.

I have tried to analyse this company and have prepared my report on the same which has been attached herewith. Please correct me if I am wrong anywhere or if I have missed something.

Good analysis… Apart from vgood return ratios and sales/profit growth in

the long term, the best part is that its cash conversion cycle is around 15

days. And MFs have a very miniscule holding in co ( DSP Micro cap fund ).

The company market cap has recently crossed 1000 Cr. MFs must but this co

sooner than later. And when they do, the stock is bound to go up rapidly.

FIEM’s top two customers have reported November sales. HMSI’s sales are flat yoy while TVS sales are up 1% yoy. the impact of demonetization can be clearly seen in november sales but still its lower than what analysts were expecting. two wheelers are expected to be more impacted than four wheelers as sales through cash mode are much higher.

I think the auto business will do OK in the long run as company has good track record there.There could be some bumps along the way but that is not an issue.

The trouble is the LED business which was doing well until recently is losing margins much faster than anticipated. EBITDA margins dropped from 16% to 9% in the most recent quarter and now below auto segment’s 12%. LED business is barely breaking even at the EBIT level. that means drop in realizations is flowing directly to bottom line. This could be due to effect of low margin EESL order but how company can grow it’s LED business profitably from here on will determine what happens to the stock price. At current valuations, there is no room for error.