I respect your viewpoint but I differ on this point. Capital allocation is very important to create substantial wealth. To me in starting years one should concentrate on gathering capital money for quality long term investment. Only thing can help on that is doing some mainstream job or business(considering that person do not have huge ancestral property as capital money)

It is not rocket science. There are so many examples of people who have done well in equity without much educational background. What some may lack in educational background, they can compensate with sheer hard work.

End of the day,

- You need to find that company(ies) that has the potential

- Find the right time to invest in those companies

- Find the right time to sell those companies.

Now, 2 & 3 only comes with experience. There’s no two ways about it. But the number 1 is the hard work part. You are not going to gain the knowledge by reading a book. Site visits, speaking to customers, suppliers , vendors of prospective companies, attending investor calls/meet are all those not in any books. But this could give you the edge over the people who are so good in analysing the books. Not saying you could do with one over the other. Both knowledge is required to an extent. But by being good in one, can compensate for the other missing item.

1 Like

Not sure if this is answered before. What term one can use to describe if one is doing full time investment and managing his personal money only? ie if someone ask what you doing, then instead of saying stock market investment, what could be more professional term one can use?

Be truthful to yourself . Tell the truth .

If you are feeling ashamed of telling what you are really doing and cover up by using fancy term – you will never feel passionate and love full time investing .

It is difficult at first as people don’t understand full time investing is REALLY FULL TIME WORK and they might ask you what you REALLY DO .

For starters work out a DAY PLAN … It will be easy for family to understand when they see you follow a day plan , slowly your neighbours & relatives will understand and within 2 years you will not have to explain what you do …

If you need assistance in working out Day plan , I will do so … but in long run you should have your own plan that you are comfortable of following DAILY

2 Likes

It is an interesting question. As someone who has followed passions one after the other since 2007, I’ve often been stumped when someone asks me what I do. Most times even I don’t know what I do. After a point I gave up explaining and in some circles called myself “unemployed”, which was easy. Freelancer, writer, seeker, coder, founder, entrepreneur, trader - Irrespective of what I answered, it was mostly a look of sympathy from people that didn’t know me and a look of envy from the ones that did.

Sometimes I am very happy that I am doing something that’s not easy to put into words. So it’s not important to label yourself for the benefit of others. Sounding professional and being busy is what is acceptable to society but to actually get things done, being idle with nothing to do and no one to please but yourself is how you can get a lot of things done that are important to you. Be comfortable with what you do and that should do. Others will respect you sooner or later (if that’s important to you).

To answer your question in short - call yourself an “investor” and look into the middle-distance thoughtfully (maybe think of what you had for dinner last night). It usually works.

45 Likes

Thanks for your reply. I would be interested to know what could be a daily plan.

Thanks. Apart from that if one has to fill child school forms or any random form then what one should fill in profession column?

I usually fill it as “Consultant” out of habit. Maybe you can fill it as “Investor” if that’s what you see yourself as.

1 Like

Some ideas what to fill in various forms

-

Visa forms & Statutory Forms - "Retired: - It is better than writing investor here as most often most of us may not have accreditation from SEBI or may not business IT returns certified by CA

-

Other non Statutory forms - " Private Investor " is be good term to define oneself …

My First Year Day Plan as full time investor … Mon - Friday

6am - 7 am - Walk in park thinking of my day plan & strategies

7 am - 8am - News paper , news on twitter

8 am - 8.30 am - Yoga

9.00 am - 11 am Read research reports from various firms & Check on VTC order status

11 am - 11.15 - break

11.15 to 1.00 - Annual Report / investor presentation / industry report

1.00 - 2.00 pm - Break

2.00 pm - 3.30 pm - Concall transcripts or audio & Check on VTC orders & updates orders if any for next day

3.40 to 4.15 - Afternoon Nap

4.30 - 6.00 - Review of a new industry / company

6.00 - 7.00 : walk and think over day affairs

7.00 onwards - Family time & social media time

After 2/3 years you will find better ways to work on daily plan as you get on auto mode on lot of things and it does not take time to study and review companies .

20 Likes

I agree with the point discussed above. Also agree with phreak that there are questions which only we can answer. We have to remind ourself what works best for us and what is good for us. Social acceptance is a human need and we can do that by doing some part time social work. Also important is to selectively mingle with like minded, ambitious and off beat people who can provide one with the extra push or help when required. Also important would be develop and cultivate creative habits which will help us to take breaks from bad phases and also keep ourself engaged in a fruitful way. It’s imp to have a day and life where one feels they are doing enough both mentally and physically.

Regards

Divyansh

3 Likes

Tell people what the landed gentry of old England described themselves as: Gentlemen of Leisure!

Shiv Kumar

3 Likes

Rocket science, probably yes.

For every person successfully making a living in the stock market, there are a several dozen who only have sob stories.

Hence, I understand the predicament of a full-time investor about describing his profession to people.

People know the statistics. Even if you put up a front, and convince them that you are an earner, they know its only for the time being.

I think you misunderstood my comment. When I said not rocket science , I was replying to other person comment on his not having fancier educational background. I said there are many successful investor without big edicational background.

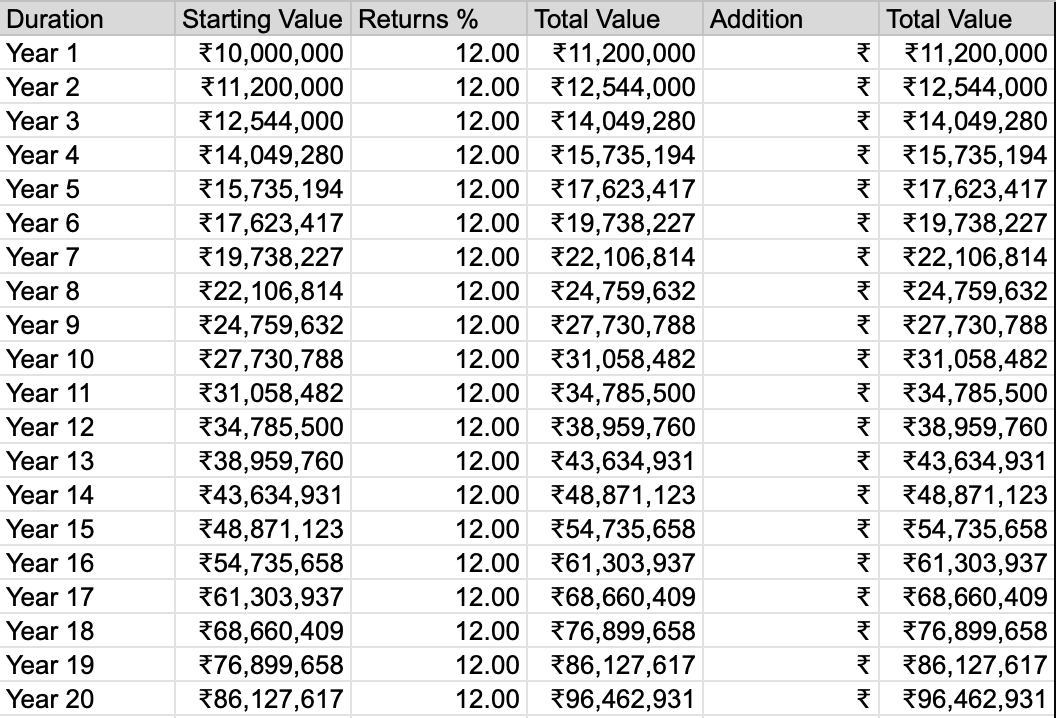

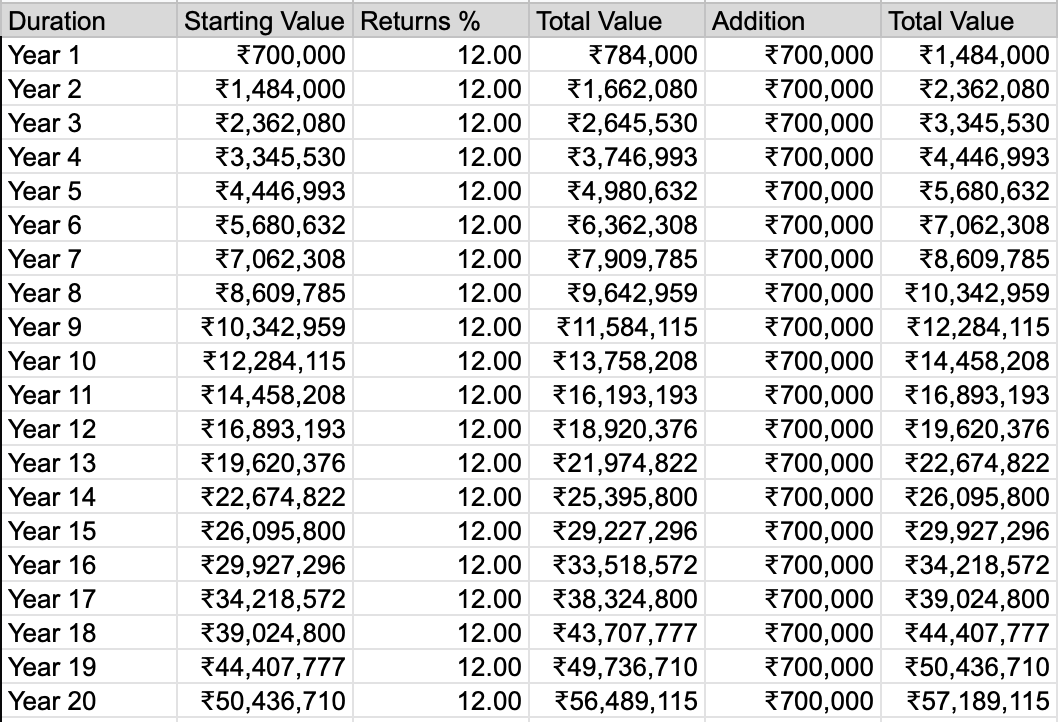

I have been running some numbers and thought of sharing with a view to get some opinion.

In the below calculations, I am running different investment strategies, with constants assuming a 12% rate of return in equity investment, an initial corpus of 1 crore and a time horizon of 20 years.

Strategy 1;

Deploy 1 Crore today and get a return of 12% CAGR for 20 years. The result is 9.64 Crores.

Strategy 2;

Deploy only the interest of the 1 crore which is taken at 7% and the core 1 Crore is never touched. We end up with 6.7 Crores (5.7 in the returns and 1 crore still in the bank as it was never deployed)

So is just deploying interest income not a wise strategy as the effect of any drawdown is taken out in portfolio building as it smoothens out the ups and downs and gives a very acceptable return sleep adjusted?

6 Likes

Are you referring to floor and upside strategy of investing? That is invest in fixed income and use equity as top up

2 Likes

Dear @Ganhk Yes. I didn’t know it is a strategy

2 Likes

HI @valuestudent , from where you getting this “Addition” 7,00,000 each year to add.

From the 1 crore which is to be kept in interest bearing products. Could be a fixed deposit or a tax free government bond.

@valuestudent, I am also trying similar setup, 1cr if you strictly don’t want to touch, you can park in perpetual bonds or govt sec bonds (Govt banks bonds or UP power & Amaravati state gov backed bonds), which can easily and safely yield up to 9.3 to 10%.

1cr compounded @9.37(SBI perpetual bond) for 20 years will give you 6cr  , and if you put interest back in equity it should be much better.

, and if you put interest back in equity it should be much better.

I have divided my capital into 3 buckets:

- 50% Equity - Fully Invested.

- 50% fixed Income(Currently building): 60% all in perpetual bonds yielding up to 9.37%, 40% Govt Sec bonds, yield up to 10%. —> Interest income --> Equity

- Monthly Income --> Cash into Liquid Funds: 7% yield —> Equity depending upon opportunity.

Risk: Perpetual bonds are interest rate sensitive and inflation risk is there also liquidity is very low, so entry & exit might be very tuff, although default risk seems very low.

I would also appreciate if anyone can highlight any other risk in perpetual bonds, which I might have omitted.

5 Likes

Friends, I think you stray.

Consider this:

The following setup takes a lot of work, but will pay well. And you are surely capable of doing it, then why settle for less (a lot less)

Invest in the following manner-

-

70% in Nifty 50. Like Yogesh. Long term return of 17% CAGR is achievable. Nibbling at sharp corrections in gold is also wise.

-

30% in established mid/small caps. Which have

15plus RoE

Growing sales

Time proven management

In an industry where:

A. it’s a leader.

B. Disruption is unlikely.

C. Backed by a strong parent.

D. Industry has plenty of runway.

Of course, we have friends at VP to let you know when your assumptions are wrong. Here the returns can be between 15% to 25% cagr over the very long term.

This approach will give close to a net 20% CAGR, but there will also be drawdown. If you have chosen good businesses, drawdowns will not bother you, but will be an opportunity.

1 crore at 20% cagr is 40 crores after 20 years. Max drawdown will be 20%, so for a potential loss of 20lakhs, we forgo 40 minus 6 crores is bad business.

The risk free strategies are also fine, but returns are barely okay. Who wants 7 crore on their death beds! One is likely to spend some money.

5 Likes