Dear @kkpatel1924 Ji,

I completely agree with you. Frankly, until some time ago I was enamoured by the job of an equity analyst. I thought that it would be my occupation for life. But, as time passed I realised that there are several vocations that I may enjoy. They may pay a little less but could be satisfying. Hence, in my humble opinion, decisions needn’t be arrived at in a hurry. We must contemplate, perform thought experiments and then decide. And, if it doesn’t augur well there should be no hesitation to switch to alternatives.

1 Like

Dear @kkpatel1924 Ji,

I have a few queries to make. I request your guidance.

In the message you’ve posted you’ve shared your thoughts that equity investing as an occupation should be for those who’ve graduated with a relevant finance degree or those who have experienced 3 bull runs and 3 bear runs.

I’m inclined to believe that the average duration of a bull run is 6-7 years and the duration of a bear run is 2-3 years. My belief is not backed by data.

So, that would imply that only those with at least 25 years of experience of outperforming the market should become full time investors.

But, recent finance graduates with not much experience of investing can embrace investing as their occupation.

This disparity is intriguing.

I would like to humbly present my thoughts-

Even 25 years of outperformance can seldom assure a person of healthy returns in the future. Past is never a good indicator of the future.

25 years will definitely equip a person with the skills required to survive in the market.

But, then the question is that can’t a person acquire the same skills in 5 years or 7 years or 10 years?

Your guidance is much appreciated.

1 Like

Investment Career with the appropriate education would automatically give you ‘returns’ with salary.

So, save money from the salary and invest in SIP. Done. So, you are already in an investment career.

If you get really good, jump ship, do some certifications and manage your own portfolio (investment and trading).

Now, if you are not into the investment career path, my subtle and sub-conscious message above was to use your brain and earn money through the profession that you have created (IT, Mechanical, Robotics, Pharma etc). Save money. Invest money. Do SIP.

If again, over the longer term (3Bull + 3Bear) you can prove that you can do well, then you can think about going solo and become an investment professional. If not, then continue with job, and invest the cash flow from job income to invest with professionals. It is the BEST way to build “wealth” since you are almost doubling the speed of money gains (creating wealth through job, and growing the capital invested).

If you jump too early without proven experience, then you would have given up your job, and also not do well with investments. Now, you are going into negative on two fronts > No Job Income i.e no Wealth Creation, and also Losing on Returns.

Nothing in life is guaranteed, and just as past is no indication of future, if you can double up with Job + Investment (DIY or MF) you are almost guaranteeing a good outcome (much high probability).

So, it is logical, and I know you understand. I am practicing this method and it is working well, and I have gotten lots of people like me who wait until 60, 62, 65 or even 70 before they retire. Jumping off the train early needs assurity and guarantee that I WILL definitely make a good return and a bear market will not kill me!

KKP

5 Likes

KKPji,

I do not agree with you that one needs a finance degree to become a

full-time equity investor. A lot of the skills can be gained by reading and

exploring on one’s own. However this would require considerable amount of

time and patience and tuition fees need to be paid to the market.

You are right in saying that an investor has to sit through multiple bull

and bear phases to formulate the investing philosophy s/he is comfortable

with. A 15-20 year timeframe is sufficient to teach one the magic of

compounding. And if one has compounded his or her capital well in this

period, the investor can consider himself or herself financially

independent.

1 Like

Dear @kkpatel1924 Ji,

Many thanks for replying. I had erred in interpreting your message. What you’ve mentioned is a great strategy to follow.

Thanks again.

@phreakv67d @maverickroger @shreys

Thanks for your replies. Well, i agree with you on scalability and the long term value creation. I didnt mean to say doing real business is better. My point was on sense of ownership. ( even if the portfolio is large). One’s net worth can fluctuate every second. Also, as they say in the very long term everyone will be dead. Anyways there is no right answer to this question.

One could argue that you are lucky to have the ability to focus and work hard

Congratulations on your success so far. Is there a place where you have shares insights on how you identified specific companies and how the story played out?

Thanks in advance,

Dinesh

Thanks a ton for kind words, it’s really encouraging.

I am trading in equities from 2005, didn’t have a vision of “what can happen to stock if we hold for long term” at that stage. Missed lot of opportunities to create wealth, bought Shree cement 144, Maruti 400, unitech at 100 10 rupees face value, capital was very short less than one lakh hence tendency was to book profits when money doubles & move on.

In 2007 I had been very active in future trading, by God’s grace made a killing & generated 10x return on capital in 6 months using SBI, L&T, BHEL & reliance. Took out 70% or capital in Nov 2007 due to marriage if my younger sister:grinning:, remaining capital wiped out when markets crashed in Jan 2008, that was an eye opener. Wasn’t actively involved between 2008 to 2012. Started taking interest in 2013 when one of my friend recommended Mt to read Peter Lynch “one up on wall street”. That was an eye opener for me & have me a broad perspective in equities as wealth generator in long term. I liquidated my insurance policies, other small FD investment & out in money in equities. I think to one of moneycontrol boarder ReddyM to teach some valuation techniques that really helped out.

Took major bets on below 5 stocks in 2014

- Madhucon Project ( was operating on 90% PLF, market cap 90 cr, asset 2000 cr)

- Gayatri Projects ( had firm PPA with AP government, market cap 300 cr)

- Rattan power ( firm PPA with Maharashtra)

- Suzlon ( sold repower )

Gayatri went 7x, madhucon sold at 5 x, rattan power though trading at lower levels still generated 2x trading returns.

BJP government came & piyush goyal started replacing high power florescent bulbs to LED, country moved to power surplus from power deficit. Sold all power holdings & moved to pharma ( suven life, jubilant Life, granules, wockhardt, natco) , had to sell out pharma in 2017 th

Thanks to Donald Trump’s, he started giving ANDA approval to all companies which killed pricing power, rotated capital to chemicals, cement sector in 2017 & bingo, hit a jackpot(meghmani, Kiri) , best investment is waterbase bought at 120 levels in Sept 2017 & sold 50% at 400:grinning:

Financial have dragged my always apart from yes bank.

I am betting on below sectors

- Cement

- Shrimp

- Rice

- Ac

- Small finance banks

- Niche companies

7 chemicals

5 Likes

My 2 cents- First post on VP

I also aspire to be a full time investor but I would use the below mentioned framework to time the transition from a full time job to a full time investor.

Always remember

- Networth = P(1+r/100)^n- So when you quit a full time job to get into full time equities always answer the question that how will your principle amount be affected and can you improve the rate of return by deeper research. Once your base principal and your incremental rate of return marry each other in a way that the return is higher than the annual salary that is your time.

-

Managing Cashflows- We all know markets are unpredictable and can price very good investments at a discounts- The larger point is that you should not be dependent on your monthly expenses- Be it EMI or any other fixed expenses etc on you selling some stock.

When your Portfolio Dividend= 1.5 x Annual Expense then it is a good time/safe . Typically dividend yield should be 0.5-1% of your portfolio value but would greatly depend on your style of investing/choice of stocks so do check this - Let markets not be an escape route: We all face challenges at work and full time investing seems an easy way out. To my mind it is elegant but not easy by any stretch of imagination

- Make sure you see the full cycle- Make sure that your gains are due to your brilliant stock picking rather than buoyant markets.

6 Likes

I have 2 corrections here

- Before opting for thought of full time equity investment, please do below as mandatory

A. Clear of home loan

B. Clear all other car/personal loan, keep credit card in hiding

C. Generate fixed income to cover your monthly expenses, salary is not right creteria, my expenses are 30% of my salary as I am being paid very handsomely.

D. Take minimum 30 lakh family floater health

insurance for parents as well

E. Take a term plan if you have any long term liability else not required

Now you are ready to think for full time trading or investing.

I have closed home loans & rent on one property equal to remaining home loan EMI of 2nd investment property hence, my loan monthly EMI liability are zero. My EPF is adding monthly interest which is 40% of my monthly expenses requirements, need to plan 60% more & am done.

8 Likes

The past 4-5 years have been virtuous for retail investors. The rally in nano, small and mid caps has generated tremendous wealth. But, there’s also a dark side to this sharp upward move- It has elevated expectations of average returns to unreasonable, unsustainable levels. And, in calculations for retirement corpus projections are made using the CAGR for the past 4 years. I’ve personally seen this happen with my family members.

My father’s cousin, a person in his late 50s, who until 7-8 years ago invested predominantly in fixed deposits, switched to futures and options, where he lost money and then to direct equity. And, investments in direct equity served him very, very well. He generated a CAGR of around 30% in the past 5 years. And, he’s truly pleased. His returns are almost 3 times the interest from fixed deposits. There’s nothing to not like about it.

But, the problem being his plan to shift funds from other investments to equity and perform investing full time. It’d be imprudent for him to expect high returns to persist. Markets will fall, its a question of when and not if. During those times his returns will moderate. But, this regression to the mean will be excruciating for him- Because he didn’t expect it.

Another point, his switch to investing is not out of love for investing but the illusion of skill.

1)For most people full time equity investing is not suitable- A job or business is often more meaningful and satisfying.

Full time investing could do more harm than good.

2)But, if someone’s desirous it should be done, as seniors have shared, after experiencing a full cycle- Bull and bear market.

3)If person is too keen and can’t wait for complete cycle, then it must be ensured as @Cshar Ji mentioned that no loans are outstanding.

4)And, if someone disregards all the above points and still wants to invest full time there’s a very high risk that the outcome will be catastrophic.

2 Likes

Hi Shreys

When we say stock market is down not everything is down. You need to have a overview of economy, movement if currency, crude price/ fiscal deficit if you are interested in financials. Even in today’s market there are stocks which will be multibaggar returns.

Whatever wealth I have created it’s from most risky section (small/mid cap) of stocks declared by these so called analyst’s:grinning:.

I am an avid F&O trader & despite so much volatility, able to generate returns in F&O as well. This is very personal & can’t be followed or duplicated.

Look for businesses which have long term moat like basmati rice, shrimp, FMCG with valuation fair. 2018 will be difficult to generate returns as you will make money in some & loose in some however long term indicators are very positive.

Dear @Cshar Ji,

Many thanks for replying. I agree that a meltdown in the market doesn’t necessarily mean a slowdown in the economy. But, for someone who has invested entire savings in capital markets a bearish environment could give a rude shock. It could be devastating. The massive appreciation in microcaps accrued over the past few years is definitely not sustainable.

@Cshar Ji, You have equipped yourself with the relevant skills and have the necessary financial cushion.

But,most people are lured by extraordinary returns offered by the market recently. Once market meltdown begins I’m fairly certain that even SIP inflows will reduce. At the end of the day, humans are governed by emotions more than cognition. Few can survive the onslaught of fear and greed.

And, regarding long term moat, I politely disagree. Everything around us is changing rapidly. It’s very difficult to predict if a company can maintain its competitive advantage over 10 years. It’s almost impossible to tell. I do realise that in most of my posts I do sound like an eternal pessimist. But, I’m not. It’s just that markets are being heroized and people lose money when reality strikes- Regression to the mean. This keeps happening time and again. In 2000, in 2008 and in the future as well.

2 Likes

I think this is a very important point and I thank @kkpatel1924 for bringing it out - that you need to have a solid finance background either by education or experience. This is perhaps the most understated point in this entire thread which mostly relates to subjectivity about philosophy of investing, how to handle life etc.

One of the gurus of investing said to someone I know - you can’t do masters in engineering before you do a bachelors. The same holds true for investing. You can’t expect to do well over the long term as a full time investor unless you have your basics clear.

A surge in small and mid caps in recent years have made many online gurus and pundits as well as their followers. These gurus mostly have left their jobs in IT, project management and non-finance backgrounds and have been mostly investing since 2009. The problem is that since then market for such small and midcaps have been great in this period, a lack of financial knowledge hardly hurt them. While many people know common financial terms, they lack the conceptual understanding of the same - few have taken the efforts to build the base first, which is crucial towards sound performance over the very long term.

One of the most famous bloggers recently valued a cement company on EV/ton basis, came to a number which he then compared to market cap and hence said that company is undervalued. He failed to subtract the net debt and made a disastrous error in comparing it to current market cap coming to an altogether wrong conclusion. Similarly, on a discussion on FEL on this forum, many people started valuing it on EV/EBITDA and saying it is very cheap - failing to understand that any organized retail outlet gets obsolete in less than 10 years (or the tenant throws them out much earlier by increasing rent) and hence 1/10th of the stores need to be completely rebuilt and hence depreciation is a very real cash cost (unlike many Indian factories which keep chugging along for 30+ years) and needs to be deducted to understand and arrive at real profitability of core business. Both these cases of exhibition of superficial knowledge. The problem is success hardly teaches us anything and there has been lack of experience of failure among many of the new age full time investors and gurus. These are anyways examples of very basic mistakes - a full time investor clearly needs to be much more nuanced than not making basic mistakes to logically justify to himself that he is a full time investor. Clearly, given the uncertainty of equity - you will demand much more than your salaried income in the medium term over a normal return on your portfolio to justify being a full time investor.

Hence, for people wishing to graduate to the highest level - i.e. being a full time investor - the first question that they need to ask is whether they are well versed with the basics first. Do you understand the basics, have you taken conscious time and effort to learn it, have you read basic books on corporate finance and accounting and have you been able to absorb the concepts well.

Some people say that they love investing but make no mistake - nobody loves to loose money, and many are destined to achieve sub-optimal results and rue their decisions to become full time investors if they don’t have the basics corrected first. Also, even a mere CA or MBA degree wouldn’t help - there are dime a dozen of them who know just the theory but not the application and what concepts to use when.

All the best,

Sarvesh

17 Likes

Also, I would highly recommend that the ‘educated’ use the grey matter between the ears to ‘generate wealth’ by using that ‘education’ to get a nice pay-check. Invest in MF initially (early) during your career. If and when you get more time in your 40’s think about quitting the job. You will NOT. Cause, the career is generating such good incomes, and investments are doing well also, and now you realize that you have DUAL sources of income.

In reality, you are already doing Equity Investing as a Full Time Career, but now you have TWO FULL TIME careers. How’s that for converting Silver to Gold to Diamonds! How about that?

Think seriously about this cause it is what my Seniors recommended to me, and I am sitting here having been on that path, and so so so so many times I wanted to just quit and get to investing, and today, I am so much (3x) better off since I invested in India, invested outside of India, and also continue to generating a career income also. There is a time to retire also, but I am not there yet, but that is for a different forum topic, so lets not go there!!!

3 Likes

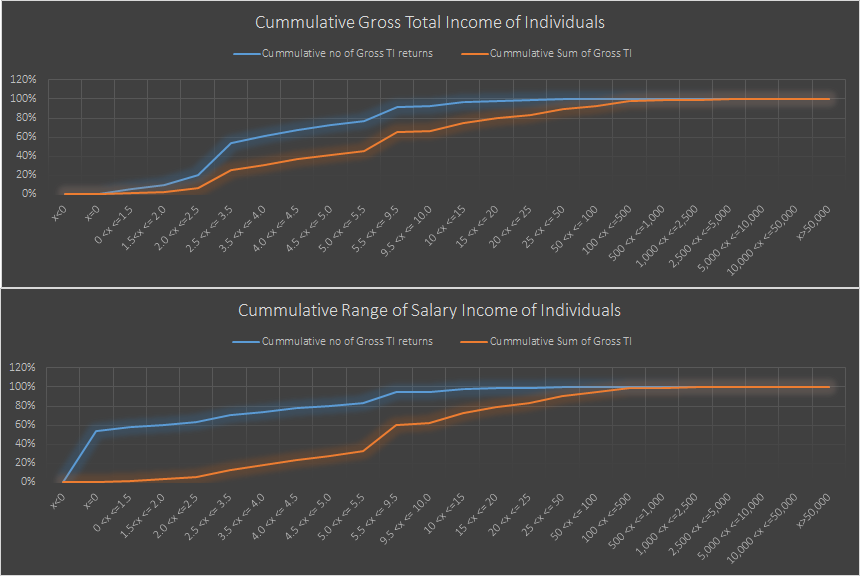

Hi

Something of interest for this thread. Income Tax publishes analysis of filings. It is freely available online for 2015-2016.

If we look at only the Individual Tax Payers (and not all types of taxpayers - table 2.1 & 2.2 in the report) we get some interesting insights. On Gross Total Income basis 2.08% individuals earned 19.97% of the top total Gross Income. On a Salary Income basis 1.35% individuals earned 20.65% of the top total salaries. The cut off mark is 15 to 20 lakh income bracket in both these cases. So any individual in this bracket or above is the cream in terms of earnings.

Another interesting observation is the difference between total gross income and income from salary at a mean level. Only after the income bracket goes above 1Cr then there is an appreciable incremental positive difference, meaning the person with 1Cr or more is earning more than 1 lakh of rupee of additional income other than his or her salary (actual number is 3.94lakhs). If one earns below 25 lakhs in salary he or she doesnt earn anything outside it, infact loses money loses money below 15 lakhs of income.

Disclaimer is that this is a very superficial analysis. But my hunch is that trends in HUF and other likely suitable categories would be similar. My point echoes with what @kkpatel1924 has said in the post above. I would safely say its better to continue with a job and keep investing than to go full fledged into investing unless you are entering the money management business as a founder perhaps.

And offcourse the most basic prerequisite is real depth in investment techniques as @kkpatel1924 and @8sarveshg mentioned.

Regards

Deepak

3 Likes

Dear all,

Some time ago I came across an interview of an investor from Mumbai whose rise has been meteoric. I’m not certain if I’m allowed to mention details of the investor. Hence, let’s address the veteran investor as Mr.S.

His success story is inspiring but the obstacles he faced are moving. Despite those impediments he never gave up. He vanquished those roadblocks and emerged victorious. The success story is an outcome of a concoction of grit, determination, dedication, integrity. The interview was conducted by Mr. Puneet Khurana from Stoic Investing. I’ve made notes of the 120 minutes interview. If I err my apologies.

The Beginning:

At the outset of the interview Mr. S declared that he didn’t complete his graduation course . He abandoned the Bachelor’s of Science course.

However, he had a keen interest in economics and statistics.

Iron and steel broking was his family business.

Post college he joined the family wholesale brokerage business.

His responsibility as a broker involved visiting the train yard and selecting defective steel units, pieces that could fetch a decent amount in the market and acting as a liaison between the buyer and the seller.

However, the yard was later shifted to a location far away from his home.

The increased distance prevented him from visiting the yard and selecting good quality steel samples.

Per him success in the brokerage business is dependent on honesty, integrity.

Ever since he left college he had developed an affinity for equity Investing.

He was an avid reader. He would collect new issue forms. New issue forms are today called Red Herring Prospectuses. He would preserve all the forms.

It was difficult for him to manage his passion for equity and the iron and steel brokerage business simultaneously.

It dawned on him that there wasn’t enough money to be made in the metal brokerage business. It helped him earn enough money to survive. But, not enough to thrive.

It was either equity or metal broking. Finally, he took the difficult decision of moving to equity full time. He was enamoured by the tremendous growth stories of ACC, HUL, etc.

This happened more than 3 decades back.

The Struggle in Equity Markets:

The veteran investor, today, has no qualms in accepting how difficult the first 20 years in equity were for him.

His decision to switch to investing full time was looked down open. The stock market was considered a speculators’ den. Disparaging remarks were often passed for the market.

But, Mr. S didn’t give up. He firmly believed that the market is always right.

His dream, his mission in life was to find multi baggers. Per him, stocks that are in the limelight, that are well discovered can seldom become megabaggers.

He is a staunch believer in the contribution of luck to a person’s success.

Between 30 years ago and today, his wealth has multiplied manifold. His quality of work has remained the same. But, what changed was his luck.

In the expert investor’s opinion, there are various factors that determine a person’s success. The important one being luck, good fortune.

But, most importantly, ALWAYS TRY HARD. ALWAYS GIVE IT YOUR BEST. YOU NEVER KNOW WHEN FATE FAVOURS US.

Finally, fate smiled at him in the early 2000s. Not because of the dotcom boom.

But, before I get to the life defining success he achieved I’d like to share the difficulties he faced on the path to victory.

His 10 year old son wanted a bicycle. On enquiry it emerged that the cycle costed Rs. 1600.

It may seem like a small amount today but in those days he didn’t possess it.

He resolved he would gift his son a cycle. Expenses on all non essentials were reduced and finally, after 18 months of toil, enough money had been saved to acquire a bicycle.

Survival was a struggle. In the meanwhile he worked at the garment business of an acquaintance. The job didn’t pay much but it was warranted to supplement earnings.

Finally, after a year, he left the job because the equity bug wouldn’t leave him.

Despite the laborious life he never abandoned his desire to learn, to acquire knowledge. He had been a big collector of annual reports. He wanted to buy financial magazines. But, they were expensive. Hence, he would work hard to secure a magazine that was reasonably priced. He believed that newspapers and magazines are the cheapest yet the most reliable sources of information.

One day, almost 2 decades ago, he was reading a financial magazine. He was impressed by the organised retailing industry.

Captivated by the retailing sector, in 2000, he invested in shares of Pantaloons for Rs 12 apiece. The major competitor in organised retail was Shopper’s Stop. Shopper’s Stop was attracting millions in PE money.

Hence, he theorised that Pantaloons would succeed as retailing would migrate from the unorganised to the organised sector.

After repeated attempts he was able to get a meeting with Mr. Kishor Biyani whose vision was organised retail in India.

I must reiterate that Mr. S still hadn’t achieved extraordinary success. But, he was trying.

Pantaloons’ first store was at Crossroad 1.

One day, Mr S convinced his wife to visit a Pantaloons store to experience modern retail.

His wife, however, wasn’t willing to visit the store since they didn’t possess the wherewithal to shop at such stores. They had just enough money to commute via public transport to and from the store. However, he convinced her to visit the store and just have a look at the new face of Indian retail. He was trying the Peter Lynch investing philosophy.

His wife was mighty impressed by the extensive range of clothes, outfits offered. Also, the experience of shopping in an air conditioned enclosure was remarkable. He was convinced this form of retail would do well. It was only a question of when.

His patience paid off. From his investment in the year 2000 for Rs 12, the stock appreciated to Rs. 2500 in 3-4 years. A return of almost 20000% in 4 years. Truly incredible.

His next investment was in a company called SSI.

He invested a significant portion of his portfolio in SSI.

He still wasn’t financially secure. But, was patient, calm.

He had decent unrealised gains.

But, past success in investing emboldened him to try his hand at trading.

His gains in SSI were eroded by trading in a now famous fertiliser company.

He sold his entire holdings in SSI at X and the stock appreciated to 35X.

He was subsidising his loss of speculation by booking his profits in tech companies. Not a very good strategy, in hindsight.

And, he continued to speculate because there was a desperation to make big money. He still hadn’t made big money and he was exhausting his savings for day to day expenses.

In this tumultuous period he never gave up learning. He worshipped newspapers and annual reports.

In 2000, when everyone was focused on IT stocks he focused his concentration on a stock called Elecon Engineering. His investment was based on the capex cycle over the next few years. But, since hardly anyone was paying attention to stocks other than IT he got a wonderful entry price of Rs 27. Along with Elecon he invested in Dynamatic Technologies at Rs. 27. He was able to detect the trend before anyone else.

When market trend aligns with our strategy massive wealth is created.

And, he attributes it to luck if such a favourable alignment occurs.

He was way ahead of the trend. His patience was tested. But, fruits of patience were sweet.

In 4-5 years he sold his holding in Elecon at Rs.4000.

One master tip- He never looks at his cost of acquisition. It leads to anchoring to the cost price. He looks at the current price and assesses the situation. If investment thesis is valid he holds. Else exits the stock.

He chose to be a contrarian and invested in leaders in the struggling sector. When the sectoral outlook improved gains were massive.

Criteria for investment :

1)Which are the emerging sectors?

2)Which sector can have positive trend in the market?

3)Most important is the price of entry and patience.

4)Good entry price gives margin of safety.

5)Look at shareholding pattern.

6)If mutual funds, FIIs have holdings,the stock is dissected enough, it is unlikely to be a megabagger.

7)Never place target on selling price.

8)Always set review prices.

9)If review target is achieved, review stock fundamentals. If thesis is still valid hold. Else, sell.

8)Annual Report is the Holy book.

9)All persons have strengths and weaknesses.

10)Find your strengths and focus on it. Refine it.

11)Always be a student. Keep learning. The day you stop learning the downfall commences.

12)Knowledge is supreme.

13)More than what to do, what not to do is more important.

14)Be an eternal optimist.

15)Don’t give up. Have faith.

16)Finally, stay invested in equities and trust the growth story of India.

And, the investor finally did make it big.

He did very well for himself and achieved his dream of being an extraordinary success by starting from scratch.

It’s a true success story. The aforementioned investor, now in his late 50s, may not garner media attention. But, it’s a story that’s inspiring, motivating and reassuring that every person possesses the ability to succeed.

If I’ve erred in any part my genuine apologies.

Many thanks.

23 Likes

Thanks for your efforts in putting up a big motivating story.However I would like to draw attention to few aspects which need a cautious approach towards stocks:

1.poor corporate governance STDs in India leading to quite a few companies having a free fall eg p c jewellers, vakrangee, kwality, axis etc etc in recent past and the reasons still not clears till date.

2.I am sure the annual reports incl financial data of these companies must HV bn good

3.The legal system being v slow and provision of class action suits not being there in India encourages promoters,management to do all kind of mischiefs and get away.

4. There may be one successful investor, there may be 99 others who must have lost in this process and could not recover.

While it’s desirable to remain motivated, it’s also necessary to remain cautious as everyone may not be that lucky to get back once fallen in trap.

2 Likes

Dear @atul1082 Ji,

1)There will always be some companies,around the world, that will skirt the law or blatantly violate it.

The US, which is believed to have stringent corporate governance standards has had several companies that indulged in unscrupulous practices. The actions of those companies were in wanton disregard of the law. Rather they were contemptible.

Let’s not conveniently select some companies that have indulged in unscrupulous practices and paint the entire universe of stocks with the same brush.

And, when we decide to invest in stocks we have to embrace the risks associated with it. It’s entirely possible that the company we invest in is a sham. But, is there anything we can do about it?

We can diversify sufficiently to protect our portfolio?

Beyond that, there’s precious little we can do.

If a person isn’t willing to shoulder this risk then investments in equity should be avoided.

Now, coming to the supposedly risk free investments- Fixed Deposits

Over centuries there have been banks that have failed. Even the ‘too big to fail’ ones have failed.

Does that mean we stop placing faith in banking institutions?

It’d be imprudent to do so.

At some point we have to place faith, we have to trust. The entire modern economy is based on the faith that the future will be better,that businesses will grow, that life will improve.

I agree it’s wrong to have blind faith. We must introduce safeguards to protect ourselves. But, there’s only so much we can do.

Shams, manipulations and charlatans will always be there. We’ll sometimes be their victims.

But, we have to accept it and move on.

And, finally it boils down to having reasonable expectations. I don’t think I can ever be as successful as the investor whose story I shared. Not even close.

All I want from equity investments is preservation of purchasing power and some.

If I achieve that I’m a happy person.

Many thanks for sharing your thoughts. I truly appreciate it.

@shreys I have also listened to this podcast of Mr. Divyesh Shah. The Rags to Riches story. His story kind of reminds me of the life of Mr.Kedia.

2 Likes