DRHP of Equitas Small Finance Bank.

Will Buying Equitas now entitle me to apply for IPO under existing shareholder category ??

Yes. But you need to have at least one share in your demat account in the record before Equitas Small Finance bank RHP filing date to be eligible under shareholders category.

The draft RHP was filed with SEBI on Dec 16th. Would that be considered the record date for the Shareholder category applications?

If i bought on 17th December then i am not qualified for shareholder category application?

According to my knowledge you need to have shares in your account on the date of filing of RHP with SEBI. The filing date of Draft RHP (or DRHP) is not relevant.

You need to buy the shares before T+2 trading days of the filing date so that you get the credit of the shares in your Demat account a day before the record date.

Q3 FY20[Link]

Healthy growth in loan book, NIMs increased from 8.83% to 9.17 % QoQ

Stabe GNPAs 2.86% vs 2.88% QoQ

Cost to income 66.2% vs 69.1%

MicroFinance now only 24% of overall book

CASA ratio needs further push, at 23%

RoE and RoA of 2.1% and 14.86%

NIMs have went up despite MF share going down

Disc: Invested

Update: Mgmt commentary today:Link

3 Likes

Investor Presentation

Concall Highlights

Investor Conference Call Highlights

- During Q3, the company has raised Rs 250 Cr of primary capital by private placement.

- SMB loan business saw strong growth and 60% of the customers in this segment are new to credit, showcasing good untapped potential in this segment,

- In the MF segment, the company saw some issues in 4 districts in Maharashtra mainly due to floods and political disturbances. The company has started cross-selling recurring deposits to MF customers and more than 3 lac customers have engaged in this already.

- The company has also issued 80,000 FASTag stickers in the quarter.

- The slippages in this quarter have grown in line with advances according to the management. The above-mentioned incidents of floods and political disturbances have also contributed to this rise. Overall, on a net slippage basis, the company has remained flat for the last 3 quarters.

- The company has not seen any issues arising from its existing Karnataka portfolio as it does not operate in the regions affected by the political disturbances that happened in the state in the recent past.

- The company is also seeing its unsecured business loan assets unwinding and this has also led to somewhat stable NPA figures. These assets are at Rs 200 Cr now and are expected to be run down within a year when the loan terms end.

- The company has around 65000 customers in retail TD which is around 13% of the total CASA portfolio.

- The growth in the SMB loan segment is driven by the Rs 5 to 15 lac tickets. The <5 lac ticket loans have grown around 20% YoY.

- The average ticket size for the SMB book is around Rs 6-7 lac. The management has stated that accounting for the inherent risk of the business, the NPAs levels were expected to be around 4% but the current NPA levels of 2% showcase the company’s good risk management and performance in this business segment.

- The NIM has risen in Q3 primarily due to a fall in cost of funds in the quarter.

- The employee cost has grown 27% YoY mainly due to the addition of 328 and 247 people into the workforce in Q1 and Q2.

- The company has moved to the new corporate tax rate from Q2 onwards. The new tax rate is expected to be a little less than 25% overall for the company.

- The company is seeing stress in the M&HCV segment in the vehicle loan business which comprises 65% of the vehicle loan book. Thus the company is trying to shift the product mix from M&HCV to LCV and SCVs to reduce stress on the loan book.

- Around 65% of customers in the vehicle loan business are first-time borrowers and thus have no CIBIL scores. The management believes it to be a characteristic of the segment and are confident in the company’s risk assessment and disbursement system to properly handle this issue.

- The company has more than 100% cover for its secured working capital loan portfolio. The customer composition in this segment is 47% trading, 27% manufacturing and 27% services. The growth in this business segment is driven by tickets in the 50 lac to 1 Cr range segment. The company is also looking to expand the lower ticket segment to build a more granular portfolio with better collateral security.

- The company also made recoveries of Rs 35 Cr in both the CV and SMB loans businesses.

- The PCR for the company has remained stable QoQ.

- The company is primarily targeting loan customers of banks with weak finances and takeover or merge targets. It is also looking to expand its working capital loans business by adding more customers who are uninitiated to working capital.

4 Likes

1 Like

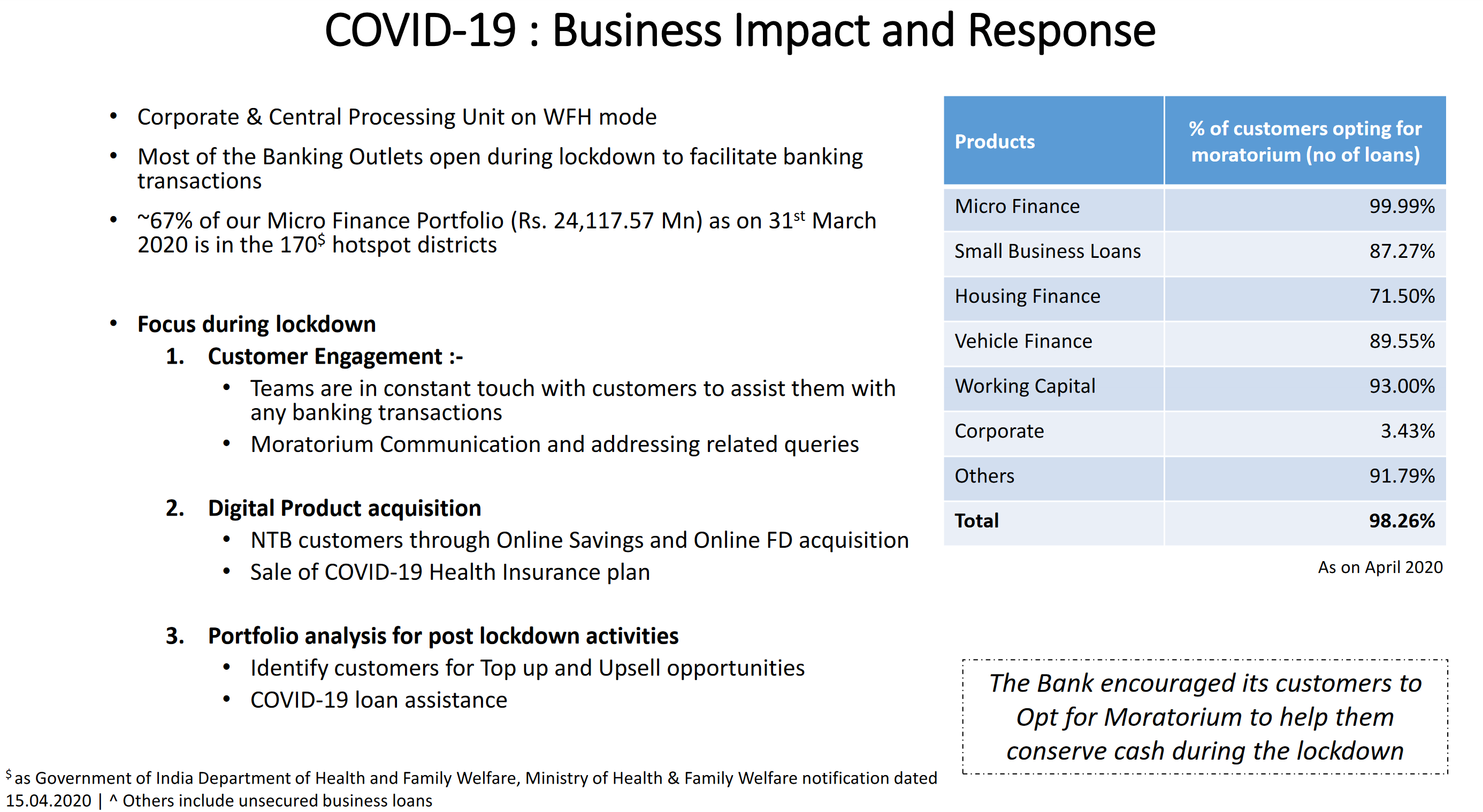

Q1 Results out

Around 43% of book under Moratorium .

Rest all parameters are good.

1 Like

No one talks about financials, especially SFBs these days. Ujjivan SFB trades below the issue price band of 36-37 at 32. The sector is in pessimism and will that make a good choice to invest in Equitas SFB IPO ? That pessimism is indicated in this thread also without any new posts for 2+ months in these IPO days. Inviting views.

Here is the IPO note from geojit with subscribe . https://newsletter.geojit.com/researchnotes/research_note_2020-10-19_12-40-53-000000.pdf

Problem is that Equitus SFB may also go through the same dilemma as Ujjivan SFB shareholders are having currently. I mean the overhang of higher shareholding and reverse merger etc.

Reports:

a good article on ESFB but seems a little too optimistic

1 Like

Haha, the moment he projected EBITDA/share about a bank, I came to know that the author has no knowledge about fundamental analysis and the moment he started giving technical analysis about a stock listed less than a month back, I also came to know that the author has no knowledge about technical analysis.

Beware about what you read on the internet or for that matter anywhere, most things that are worth reading on not published and and most things published on internet for free are not worth reading anyways.

11 Likes

Equitas SFB launches 3-in-1 account offering various investment options:

Equitas Small Finance Bank announced the launch of a 3-in-1 account that allows its customers to invest in a widevariety of financial products. The account will combine savings, trading and demat accounts as three financial products under one umbrella. A 3-in-1 account is a convenient option that helps the customers keep all their banking and financial investments under one umbrella entity.

Not quite active thread. :)…Equitas came up with decent set of numbers and declared dividend

EQUITAS_05022021174707_EHLResultsSE31Dec20.pdf (3.8 MB)

Dividend yield seems to be decent at this level.

What caught my attention is the FII increasing stakes during the Dec quarter. Below is summary

MIT & Al Mehwar Commercial Investments Llc- (Treefish) increased stakes by more 1-2%

Tt Asia-Pacific Equity Fund, Societe General and Mine Superannuation Fund taken fresh position around 1%

Overall FII holding increase ~ 5%

Views on result and expected performance from someone following this stock closely will be very helpful

Disc - Holding since IPO in small quantity

They are offering 7% interest on FD.

how they can manage such interest rates…

They will attract lot of deposits at such a high rate…

Disc. Tracking

Probably, the price is sideways could be due to

How promoters are going to reduce it to 40% as per RBI Regulation. It means that SFB share capital will be diluted so that the Holding company percentage comes down. Similar to how idfc bank merged with capital first to meet 40% requirement after 5 years.

or

Waiting for a reverse merger. or GNPA rise due to Covid Impact on SMEs and MSMEs.

1 Like