The reason I prefer Ujjivan is because it’s valuations are cheaper, better geographic diversification and better GNPA and NNPA ratios. But both have some pain left in theNPA and pre-demonetization growth fronts. The valuation has caught up a bit as Equitas fell from Rs170 odd.

2 Likes

I will sound extremely biased towards Ujjivan so pardon me

In this business of possible tail risks, geography diversification must be very important. Ujjivan’s GNPA had been extremely low pre-demon (thats because their loan book was totally composed of group loans which have negligible NPLs). Their CASA is low because their strategy until now has been to garner institutional deposits. Hence, a lot of scope for CASA improvement as all branches are converted to SFBs. They only yet have ~100 liability branches. Samit Ghosh’s track record impressed me more (I’m not undermining Equitas management). And I love Ujjivan’s logo!!

Disc. core holding for very LONGTERM. Biased because invested or the other way round, I do not know.

3 Likes

Results- https://www.bseindia.com/xml-data/corpfiling/AttachLive/45d801b3-d702-4bd8-8948-3e26df83469a.pdf

1 Like

Looks like equitas SFB is finally back on track reducing its npa’s and further provisions and improving operational efficiency. Equitas SFB decision to move aggressively toward secured loans is starting to show results.

How is Bandhan Bank placed vs Equitas n Ujjivan? Are tailwinds back for whole of the sector?

it was Demonetisation that separated men from the boys, Bandhan is incomparable with equitas or ujjivan, although these new kids on the block has a long way ahead, I think bandhan should trade on par with hdfc bank given its superior asset quality or return on avg assets/equity.

This 1 sector is where ocean of money that just lies underneath and the potential is still untapped, ofcourse high returns comes with high risk, having said that the indian economy is something that would just suck out whatever you drop in it

Disc: hold all 3 since their IPOs

2 Likes

3406957 shares have been bought for delivery today. It was last seen in 1st week of Jan 2018. In last 365 days, it is 4th highest day that has seen such a huge delivery.

Some fund off loaded 2,424,812 shares Yesterday. Despite this stock is steady, watch out.

1 Like

Good coverage about company https://www.edelresearch.com/showreportpdf-36346/EQUITAS_HOLDINGS_-_INITIATING_COVERAGE-APR-17-EDEL

good that you posted an old report. I could see that the earning projections are missed badly for FY18. Clearly, why we need not follow them especially when the industry is in transition. They should stick to excel sheet and copying management commentaries.

2 Likes

Yes, due to black swan event for MFI in the form of demonatisation. Now, their 1. Mfi percentage of total loanbook has come down majorly. (a conscious decision by the management) 2. Collection efficiency is back up. 3. Deposits and casa as a percentage of total borrowings has gone up.

Disc: invested.

1 Like

I don’t understand the expectation here. They failed in their main biz i.e. MFI which was supposed to be a simple business of lending to lower strata. They were given banking license to accelerate the financial inclusion and now they want to move up the value chain and serve relatively better off. How are we sure that they would succeed in this relatively complex biz of banking and multi line lending. The other day I saw an AU Small Finance bank branch at a prime location in Mumbai. I have talked to few Uber/Ola drivers in Mumbai. They told me that AU Finance is the prime lender in this predatory vehcle finance @18% leading to lots of distress among first time drivers/borrowers. One Uber driver promised me to take to an yard where 100s of abandoned vehicles financed by AU finance are kept. All defaulted and ready to be sold but nobody is interested. We must all request RBI to revoke their banking licenses for this fraud and bubble creation.

1 Like

demon affected MFI the most of all industries. Relative to overall credit, MFI will always always remain a tiny percentage anywhere in the world .There is only so much scope to grow in MFI. Their long time aim is to be a full fledged bank, not just a small finance bank.

Listening to the concalls, you would perhaps get a feel that the emphasis is on minimizing risk while the opportunity for growth remains aplenty.

2 Likes

Press Release:

Q1FY19 Results:

Investor PPT:

Management Commentary:

Hi @desaidhwanil bhai & others,

I just went through Q1 FY19 conf call & investor presentation of this company. I haven’t studied the company in depth. Following are some questions I have. It would be great if you can answer them.

-

Equitas has tried to diversify the loan book by going into Vehicle Finance & Property Finance. The questions I have is - are these loans going to the same set of MFI customers or these are non-MFI customers? There are few reasons for this question -

One, the mindset required to serve non-MFI customer & operational parameters are very different from those required for the MFI customers. How is company able to handle this dichotomy of mindset while lending?

Two, I went through various loan products on the company’s website & I see few things - like Micro LAP - is this MFI product or non-MFI? Similar thing for product called Micro Home Finance. So where are these micro versions of LAP/Home Loans are accounted in MFI portfolio or non-MFI portfolio? The mindset required for Micro-LAP might be very different from normal LAP product apart from accounting question. -

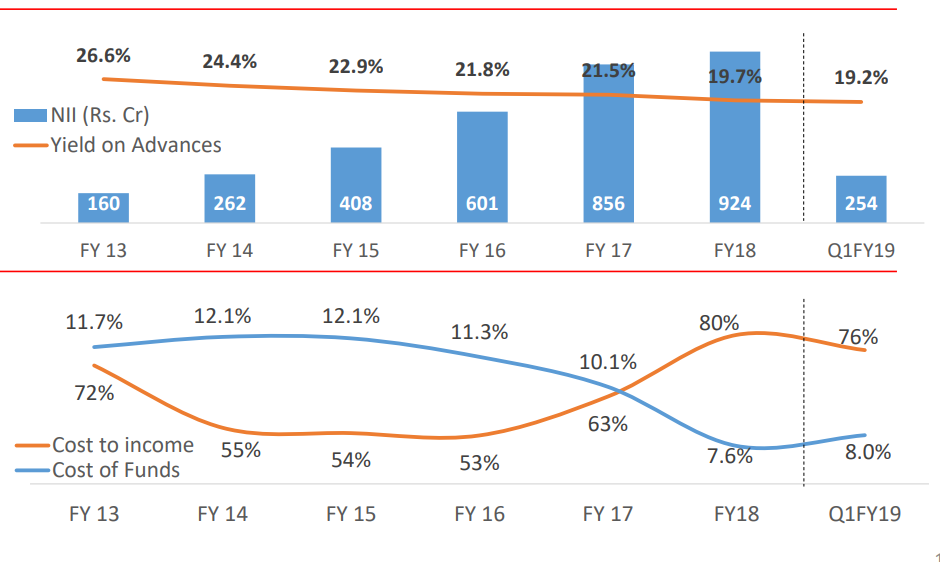

I do not know the age of the Non-MFI book & I’m assuming these are pretty recent products (2-4 years). Please correct me if wrong. In this context, the yield on advances for MFI book was 23% as per management in Q1FY19 conference call. And this yield was similar in FY14 (around 24%). So the cost of funds has gone down ~4% points during this time but MFI interest rates haven’t gone down? Is this correct understanding? Or the other way to ask this question is, blended yield & costs have fallen by 4% but no benefit has been passed on to MFI customers? Doesn’t this amount to still giving opportunity to non-bank based MFI players?

-

Management said MFI book GNPA was at 0.9% while that of non-MFI book was at 3.5%. I do not know how much of this is related to demonetization & how this number has evolved over time. With this in mind, what do you think of underwriting skill of management & expertise in non-MFI areas?

-

On MFI side, I see average ticket size was 29,000Rs. The first post in this thread written in May’16 states the average ticket size was 10-11,000Rs. If these numbers are correct, what are your views on almost ~3x increase in average ticket size? I do not know the data on average duration.

-

The company borrowed more in Q1 in anticipation of probability of interest rate increase & to fund growth. The funding from refinance went up from 1731Cr to 2653Cr. What do you think of this move of anticipating interest rate hike & taking business decisions?

-

Currently there is no overlap between asset side MFI customers & liability side customers. The company plans to try out mixing these activities at both side branches with RBI permission. What are your thoughts on this in the long term, not just for Equitas but overall industry?

On a top level, it looks like Equitas is trying to become next RBL bank as they also have decent MFI exposure. How do you compare the business/management of the two? What excites you in Equitas?

Disc - No investments in Equitas, studying

2 Likes

Hi Rupesh,

Thanks for asking very pertinent questions. It made me think and dig deeper for some questions which I had not asked myself. I will try to answer these to the best of my knowledge.

-

In one of the interviews Mr. Raghavan explained that the client profile of Non-MFI products (exclude some part of Micro-LAP with low size 50K-500K) are better than Non-MFI and backed by security.

-

They have been in business of used commercial vehicle lending, MLAP, MSE and Housing since 2012-13. Other products like agri loans, new vehicle loans, goal loans and Micro Enterprise Loans book are 1-2 yrs old and constitute 15% of total advances. I agree that the benefit of lower cost of funds have not been fully passed on the customers. Ujjivan’s yield for MFI is around 21% compared to 23% for Equitas. Despite this Mgmt continues to guide 30% growth in MFI book.

-

This is their loan book distribution: MFI, Vehicle finance and micro-lap nearly constitute 80% of their book (each roughly 27%). Given that they had experience in used commercial vehicles lending since 2012 gives some comfort. In Micro-LAP they have experience of 6 yrs and PF quality has been very good as per mgmt.

-

The av. ticket size of MFI loan looks similar to that of Ujjivan.

-

Anticipating interest rate hike : In hindsight it seems to me a good decision by management.

Disc: Invested

2 Likes

2 cents…

1.Probably the mix, from above tv interviews, mgmt says that the segment they serve in m-LAP or Vehicle finance or MSME, it is bet. 50k-50L across the segments, so they still serve the under-served & have not much moved up the value-chain but diversified 70% of pf from unsecured to secured

- dont know, i think they are still factoring in the bank conversion cost and this high lending rate might stay for a while until the cost-to-income is improved(?)

3.Yes, the mgmt hasn’t done well interms of managing the non-MFI portfolio where the stress seems high & shows their inexperience in this segment

4.Again, i think the rise in ticket-size is due to migration, un-secured to secured

5.to me, it looks like a prudent move atleast in hindsight as the interest rate has only risen as they anticipated

6.dont understand, leave this qn it to others’

Being a shareholder since their IPO, i prefer them to be Equitas rather than being/emulating someone else

Also, only way i see ahead for the stock to be re-rated by the market is improving asset quality, any slippage on this front alone can take stock nowhere imho.

Looking for more facts & opinions from others as well.

1 Like

Sorry for delayed response as I was stuck in AGM travel schedule and could not revert promptly. Here are my answer to your queries

- In order to answer many of the queries and especially related to venturing into new products and how they will handle the transition to it from pure MFI lending, I think it is important to understand what Equitas is good at and what capability it has built over its earlier MF Avatar. IMHO, most of the good MF institutions, over a period of time, build two capabilities

- Ability to assess the credit profile/quality of the bottom of the pyramid

- Creating cost structure that allows company to collect small repayments with high frequency and still make money

I think both of these are extremely relevant to the success of serving the bottom of the pyramid customers with small ticket size. Based on this context, following are the answes

-

Vehicle and property finance: they are serving similar class of customers but not the same customers. My understanding is that they clearly segregate between their MFI and non MFI customers and there is very little overlap if any between the two. In fact, they are one of the most cautious MFI in terms of increasing ticket size for their MFI customers and it is one of the lowest among the all MFIs. I do not think there is any overlap between micro LAP and MF customers either.

-

In terms of mindset, I do not think it require different mindset as the two essential qualities required for catering to BOP segment is the same. What varies is the product structure which can be learnt/modified over a period of time with experience.

-

In terms of yields, incremental lower cost fund is getting deployed in non MFI business where yield is anyways much lower and hence on blended basis the yield is declining in line with cost of funds. As the legacy/old borrowing get phased out and new fund gets deployed in MF, I expect yields to come down for MF business too over a period of time. for Non bank based MFI, it is very difficult to garner funds at the cost of SFB (6.5%) and hence I do not see how/why they shall be able to seize this as an opportunity.

-

For the GNPA side, I feel it is important to understand what kind of credit costs are baked in the business model. It is not appropriate to treat all types of lending/financing operations as the same and treat them at par. For example expected credit cost in structured financing on portfolio basis can not/should not be compared with that of a home loan portolio. At the end of the day, each management builds a base case assumption for credit cost while arriving at expected RoA. As long as the base case assumptions are as per the business plan and RoA is respectable, GNPA in isolation does not give full picture. Equitas management has been upfront throughout and has suggested that the target segments/population that they cater to, higher GNPA is baked in the expected yields and cost structure. Having said that they did face challenge last year due to demonetization and vehicle financing being a larger portion of their book which was badly impacted by demonetization, the GNPA may look little elevated.

-

On the ticket size, as mentioned earlier, Equitas is one of the most conservative MFI in terms of ticket size. In fact, in Q2/Q3 call, there was a question from analyst as to why they are to increasing their ticket size in line with other MFIs and if they don’t do it whether their growth will suffer. Management was very firm about not increaseing ticket size for getting growth as the cash flow of end user may not support it. In fact they reiterated that they may not increase ticket size as they see enough room for growth with the current ticket size. Having said that increasin ticket size (without commensurate increase in tenor) remains a worry for the whole sector as there is no corresponding monthly cash flow increase (income level) of end user.

-

My understanding from the call was that the primary driver for the move on higher borrowing was visibility of growth and tightening liquidity. They did talk about interest rates firming up however their primary driver as per my memory was that they did not want to end up in situation where the growth in advances is possible but there is not enough liquidity to tap it. In any case, these are tactical calls and every management in banking/NBFC industry take such calls (increasing/decreasing deposit rates ahead of curve etc) and I would not worry too much about it and leave it to management’s best judgement.

-

If you listen to management’s commentary, they are very clear that the mixing of activities will happen on a very small scale and based on learnings/feedback from that only it will be scaled up if they see merit in it. My personal sense is that given the segmentation of customer base that they have on both asset and liability side, such mixing of activities at least on lending side will be miniscule until the asset side customer base evolves to a stage where they move up the per capita income level and start generating enough savings. On the other hand, I do not see why the liability side of customer base can not be tapped for fee based income/product distribution opportunities. However, contribution from such overlap will remain small in my opinion at least in near to mid term.

I am not too familiar with the evolution of RBL bank, however what excites me about Equitas (and in general SFBs) is that they garner much better yields as compared to full scale bank while the cost of fund will become comparable to a full scale bank. Now this incremental NIM, can be very profitable if they manage their operation and credit cost well. I do not see why SFB can not reach 18-20 RoE in next 3-4 years. Perticularly for Equitas, what I like is the prudence that management has shown by making various choices. They were the first among SFB to move towards reducing MFI weight in overall book (As proportion) to ensure that the lumpiness attached with MFI business does not cripple them down (as it did many MFIs during crisis). This would have meant lower growth for them in short term, but much stable business in longer term. They decided to take short term pain in stride over longer term gains. They have also been very conscious about not taking undue risk in MF book throughout the history (and this was further corraborated by one of their peers in MFI days) be it ticket size or tenure of the loan. Lastly, the way they have scaled up their liability franchise is remarkable. 35% CASA for a 2 year old bank is extremely good (while Ujjivan is struggling at 5-6% level and IDFC bank even after years of effort is yet to reach that scale). This shows their ability to adjust to new realities and execute well.

I hope this provides some food for thought and many more queries!!

Disclosure: Holding Equitas @ average price of 140 and forms significant part of my portfolio

26 Likes