Other holding of Cartica capital India ltd…

Pi Ind …

Page ibd…

Total three scrips only

One other holding: Shree Cement Ltd

Comparison of RE with Harley D.

2 Likes

Complete specs and coverage for Pro1049. This is a crowded space but given Eicher’s distribution, I feel that they may get traction

price of around Rs 7 lakh for BS III and around Rs 8 lakh for BS IV variant

http://www.eicher.in/etb/trucks/pro-series/1000-series/eicher-pro-1049

https://indread.com/37402/eicher-pro-1049-mini-truck

1 Like

Surprised that none of the regulars updated the SIAM figures for April. I assumed that it is old news but just realized that it is not yet updated

Quarterly results are expected tomorrow (5/5/16)…I don’t anticipate any big surprises. Should be another routinely, well executed quarter, going by the trends of SIAM figures in Jan/Feb/Mar

PS - invested; no transaction since an year plus

Quarterly results are out

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/BD4B7DF9_C9ED_402C_942B_2132D695BB4F_141902.pdf

EPS - Y on Y - 122.7 vs 71.68

NP - 334.5 Cr Vs - 195.28

Total income - 3764.87 Cr vs 2568 cr

What can I say, except hats off

6 Likes

Simply no words to describe this company…Just Amazing !

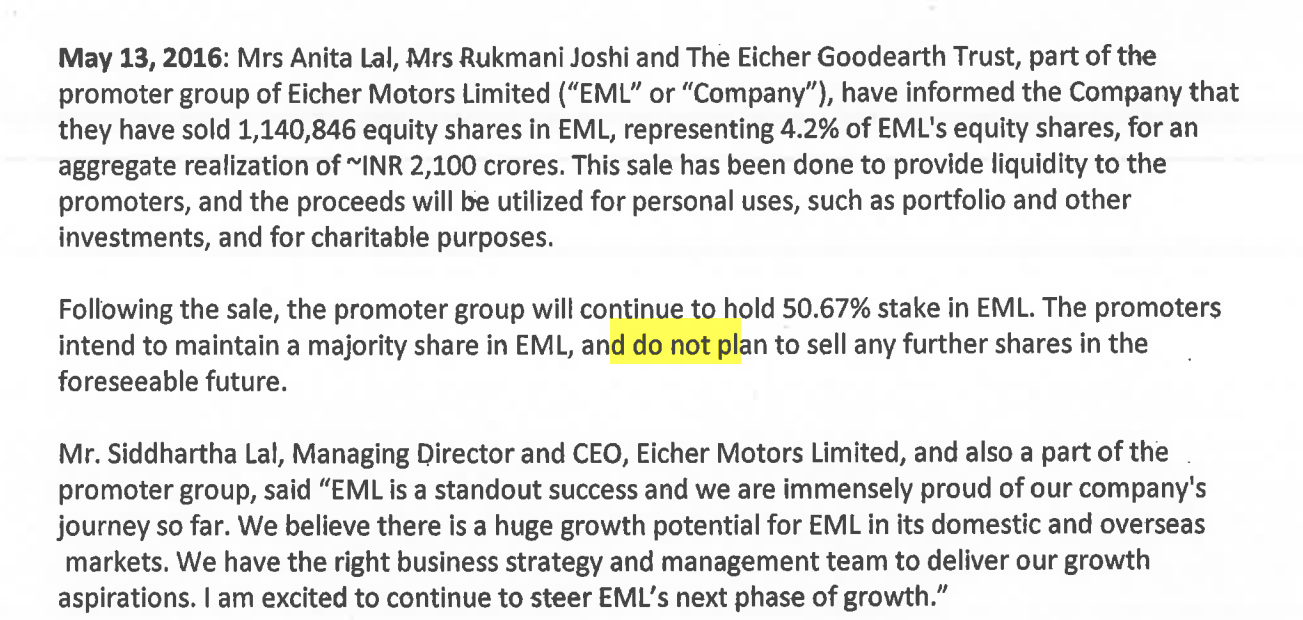

Promoter Group sells 4.2%

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/6DCE3151_25B3_47BD_AF68_1079995DBC1A_104108.pdf

Disc: Invested. Bought today and will buy more on further falls.

1 Like

Promoters sold 4.2 %…that is a big amount…does that mean they feel the stock is trading at full potential and does not see much upside or growth may moderate in future which can lead to correction in stock in future.

I wanted to buy at declines but after promoters selling 4.2% stake. I am confused…how to interpret this…

I agree but with a rider. 2100 crores isn’t a small sum. I think the promoter group is trying to diversify their investments. A lot of established and rich enterpreneurs are these days investing in startups trying to find a unicorn off the listed markets. Returns in such investments are exponential, the kinds that Eicher has seen since 2008-09. It doesn’t necessary mean Eicher is capping out, but isn’t a rosy news either. With the monsoon and rural PP returning allegedly, I think Eicher will meet expectations and corrections can be exploited.

I am not sure whether you guys saw the subsequent press release. I had the experience of a similar thing of promoters selling in PI and over the years in Page…to me the NOT (I have highlighted it) below is the key…I am counting on Lal to make that true…

Promoter selling and that too 4-5% in one go is not a good sign at all. After all who loves to chip the wings of the hen who suppose to lay golden eggs ahead? Its a clear indication that Mgmt feels that story is near “topping out” though it does not mean that story is over either.

We have seen how bad the performance of business where promoters sold on good days e.g. PAGE Ind, PI Ind etc. On the contrary stocks delivered quite well where promoters have bought the shares e.g. Manapuram.

The managements ability to historically grow more or less consistently vis a vis guidance should be respected. The stock at CMP is pricing in future earnings growth and the management has seen it as an opportune moment to create some liquidity. A 4% reduction of stake should be seen for what it is - and the fact that promoters continue to hold 50%+ should also be registered and respected.

As long as demand is robust and management sticks to its plans to produce 900,000 motorcycles in CY18, there should be decent uptick in earnings over the coming couple of years.

4% liquidation does not mean good times are over, and what happened with PI or PAGE has no relevance and is unrelated to Eichers future. Let us keep our discussions objective and factual, and make conclusions based on performance and not speculation.

6 Likes

Page promoters sold 10% stake to Nalanda Capital at 350-600 range (don’t remember the exact price). Mr Genomal has expressed his regret for that sell many times. Often, even promoters don’t know the how future will turn out.

5 Likes

Three growth factors to watch…

**sale of RE outside India…

**CV cycle upturn…

**POLARIS JV playing out…

1 Like

@okmehul I think that you should have provided the link, rather the cut and paste of this article, which came in ET

http://economictimes.indiatimes.com/markets/stocks/news/analysts-sceptical-about-premium-valuation-of-eicher-motors-stock/articleshow/52301487.cms

Unless, you are the author in ET (the author happens to be Ashutosh.Shyam), it is not right to cut and paste like that.

Anyway, coming to the contents of article @ 30 times the estimated FY18 earnings 771, gives it a 23K price. The question is, should we give 30 times. I believe so…here is one, which supports on increasing RE margins

http://eresearch.co.in/eresearchblog/?p=10882

There are many more but I do agree that from here, there won’t be any manifold returns, unless a new trigger emerges.

Given that perspective, the recent sale of promoter group has come as a blessing in disguise since it provides scope for accumulation around 18k.

PS - invested; views might be biased; pl do your own due diligence

4 Likes

No defense or justification…I very well take your point…my context was to share…was not aware of not having included the title link…I am so sorry…I am an infant in this fundamental analytical forum…can’t even think on such depth…I agree with you…in most of the cases actions proves the context…I shoulder on the responsibility…I hope to settle…

I really give credit to Mr.siddharth lal for his commitment and focus to increase the sale of RE…outside India…he has migrated outside India in an attempt to fulfill his commitment. He has taken challenges against big peer corporates…Next one year is vital to prove his efforts…I personally underscore his disinvestment of around 4.5%…IMHO…THIS COULD BE THE BEGINNING OF SECOND INNING…

DOES ANY BODY HAVE ACCESS TO PRESENTATION MADE BY THE COMPANY TO MOSL…on one to one basis…very recently.??