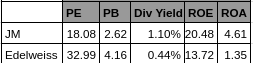

Great result by Edelweiss. Growth has been captured in the price though. P/B is 4.16 and PE 33.

Disc: Invested in JM.

Great result by Edelweiss. Growth has been captured in the price though. P/B is 4.16 and PE 33.

Disc: Invested in JM.

I am not sure if Edelweiss and JM are directly comparable, although they are in similar industries. Edelweiss is more than double the size of JM. For financial companies, size is important as it becomes easier to scale with size. Also their business segments are very different. ARC, Insurance are unique to Edelweiss.

Results look good overall but few chinks i see in their lending biz -

NPA: despite no adequate seasoning and very high growth in loan books, NPA has risen steadily to 1.75% now. Absolute NPA has grown 91% yoy vs. 51% growth in loan book. They shoud provide segment wise NPA. I think corporate book continues to accumulate higher NPA.

capital adequacy - it has fallen 17% and fund raising should be due in 18-24 months only compared with 10 yrs gap for the recent one. They allocated substantial amount in the insurance biz which they would need again for launching health insurance and ramping up general/life insurance.

I am also slightly concerned they provide unsecured lending to SMEs also.

Disc : remain invested

Did you include NPA recognition change from 120 to 90 days?

sorry, I thought this was the case all along at least in FY18.

The ARC business offers such big non-linear payoffs in such cases.

Next big trigger will be the Essar Steel resolution!

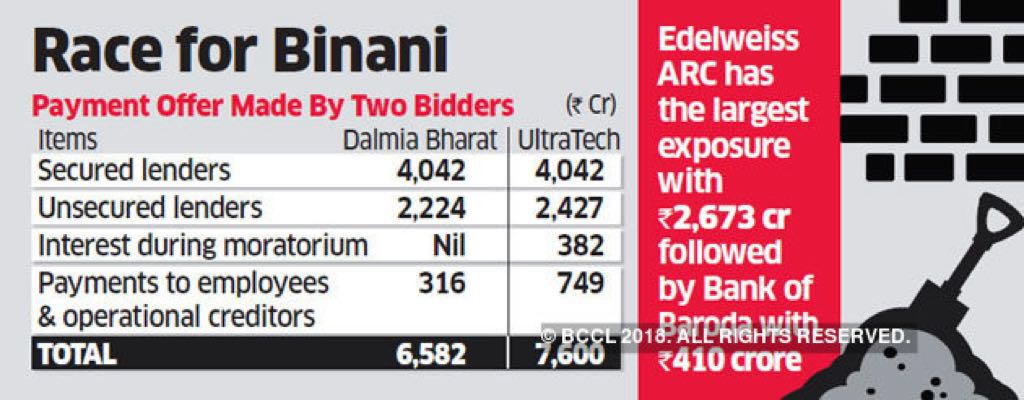

How much will Edelweiss get against their investment of Rs 2673 Cr.How much profit will Edelweiss make on this transaction ?

Thanks. This could imply that for Q1 FY 19, Edelweiss could have a pre tax profit of about 700 Cr compared to about 335 in Q1 FY18.

Saw in twitter that w. e. f March 23, Pwc resigned as auditors and SR Batliboi and company has been appointed, should this be of any concern?

There is no such update on BSE website from company anyways SR Batliboi is part of EY one of Big 4 auditors so shouldn’t be a big concern but given the manpasand and vakrangee episode market could take this negatively.

Could have something to do with this. They are banned by Supreme Court for 2 years? Can anybody please put some light on this ?

PWC has to mandatorily step down as auditors. Hence, Edelweiss has moved to another auditor.

The article is dated Jan 2018 and the matter is still not settled. If indeed PWC is banned, they will have to give up all of their Audit assignments which would have been a Front Page Headline news.

Changing auditors for Large Listed Companies is not unusual especially now since rotation of auditors is made mandatory as per Companies Act and SEBI guidelines. However, the usual procedure followed is that the new firm is appointed at the AGM while the old firm continues till then. In the case of Edelweiss, the old firm has resigned and it has created a Casual Vacanacy which is filled by the Board subject to approval by shareholders.

PwC has also resigned from audit of another listed company- Atlanta. The communication does not paint a good picture for Atlanta. The point to note is that PwC has stated the reason for resignation in this letter unlike so in the case of Edelweiss.

I have worked in S R Batliboi for 3 years in the past and I am aware of the efforts taken by Partners to get new audit clients, and it is the same across the industry. Therefore I do not see the change in auditor as a reason to worry for investors, without any reason to suspect.

Disc- tracking Edelweiss. Not invested

What I know is Edelweiss changes their auditor every two years which is a good practice. BSR and associates was the auditor in Jan 2016.

PWC received a 2 year ban. Now, they have a reprieve till March 2019. Pwc and most good companies they audit will plan accordingly.

https://economia.icaew.com/en/news/february-2018/pwc-india-gets-leeway-on-two-year-ban

Bank of America Merrill Lynch, Edelweiss, JM Financial, KKR, Lonestar-IL&FS, Resurgent Power, SC Lowy, Torrent, Varde Partners, SSG Asia, Worlds Window EXIM and NIIF are some of the financing agencies that may bid for the three stressed power projects that PFC has put up for sale.

Amit Jeswani on Edelweiss

PwC has resigned. They have already appointed S R Batliboi (Indian member firm of E&Y) as their auditor.

Q1 Results: https://www.bseindia.com/xml-data/corpfiling/AttachLive/e4b3e48f-2f8b-4115-8604-fb5abae5f2b4.pdf

Investor PPT