Anyone tracking this company right now? I did a quick look-up based on request from friend. While company continued to struggle, it seems Covid induced IT spending gave it a shot in arm. As per the latest presentation available on company website (Nov’21), their recurring revenue has been on a consistent uptrend in past 3-4 qtrs indicating growth is back for now. Whether it is sustainable needs to be studied. Company’s share price has zoomed over last year.

1 Like

I am tracking this company for the past year and have invested as well. I am quite interested in seeing how this plays out long term. The previous issues of client concentration seem largely behind and the current global scenario make it quite an interesting play.

My initial interest was due to Data Localization and foreign control over the data. This seems to be coming to fore this past year. I suspect, the company will be slingshot several times over the next year.

I am still tracking the company and trying to understand the following:

- Given the nature of business and the expected growth, what is the extent of capex required on regular basis? If the capex required is very high then profits will be lumpy

- Globally what are the profit margins for PaaS players and where does E2E stand? It is tom-toming its lower costs compared to larger players, so would be interesting to see how its margins compare vs bigger players

If you have any links to their concalls (I could not find any) or management interviews, do share. This company does look interesting!

E2E Networks posted excellent results with PAT of Rs 2 cr for the quarter ending March 2022. The monthly-recurring revenue has been growing continuously QoQ since March 2020 from Rs 2.2 cr (per quarter) to Rs 4.9 cr in March 2022. The sector seems to have strong tailwinds and a long pathway with the growth of cloud computing, gaming, machine learning and AR/VR.

Disclosure: Invested.

2 Likes

Alternate cloud seems to be gaining traction even though Hyperscalers continue to grow at high rates. According to some reports almost 1/3rd of developers are turning towards Alternate cloud providers. E2E has positioned itself as an alternate cloud provider by focusing only on IAAS with focus now turned towards SMEs vs startups.

1 Like

I am disappointed that the company revealed a lot of Unpublished Information in a non-public concall.

1 Like

My recent summary about the company

Key points

- Cloud computing industry has strong tailwinds, growing at 20-30% per year.

- E2E targets SME companies and startups as customers.

- E2E Networks offers much lower cost offerings (2.5-3 times cheaper, the company claims) versus the ‘hyperscalers’ AWS, GCP, Digital Ocean and Azure.

- Revenue has been increasing every quarter since March 2020 from Rs 2.2 cr to Rs 4.9 crores now.

Details

- Investor Presentation (May 2022) is the main source of information about the company.

- 2021 Annual Report

- Screener page

- Began in 2009 before cloud computing had taken off. Developed its service for start-ups.

- SME IPO in 2018, which was oversubscribed by almost 70 times. Transitioned to the NSE main board in April 2022.

- Shareholding Pattern (June 2022):

- Promoters: ~59%

- Tarun Dua (Promoter and Managing Director): ~55%

- Blume Ventures Fund: ~11.8%

- Airavat Capital: ~4.8%

- Holding of major shareholders has not changed much since the IPO.

- Promoters: ~59%

- Focus has moved to SMEs as opposed to the startup ecosystem.

- One of the big customers transitioned out in 2020, resulting in big loss of revenue. The client concentration since then has reduced. No customer contributes more than 3-4% of the revenue. There are nearly 2000 active customers now.

- R&D costs are lower since they target customers who pay less, and enjoy simpler user experience UI and UX. R&D costs are a major component of expenses in such companies.

- Depreciation is high because computer systems have a low lifecycle of around 3 years.

Pros and Cons

- Pros

- Strong tailwinds in the industry. India is traditionally a price-sensitive market and E2E’s offering is among the lowest.

- Track record of working with a number of startups while they were small.

- Minimal customer concentration risk now.

- Cons

- Less trusted player compared to the hyperscalers. Will be severely affected if the hyperscalers reduce prices.

- Change in technology may render E2E’s current technology obsolete and require them to make substantial investments which could affect the Company finance and operation.

- Competitive industry. Company may be severely affected in an industry downturn.

- Key person risk—may result in strategy bias.

Disclosure: Invested from lower levels.

4 Likes

Good results posted for Q1 FY23. PAT of Rs 2.5 cr. Both the revenue and the PAT increased QoQ.

1 Like

I have been tracking this company for more than 12 months now…two main problems

- Annual reports do not give any worthwhile input

- Float is very low which results in wild swings in both directions.

If some big player buys out the business (like Tata bought Tejas), this can get re-rated big time…But that is just hope (and hope is not a strategy).

I have token investment for tracking purpose. It is a capex heavy industry, and depreciation will also play a big role here…Let us hope management starts sharing more information going forward to help build enough conviction.

1 Like

does the current CMP justifies the total sales ??

cmp=₹ 172

sales ony rs 51.87 cr

The no. of equity shares is relatively low. Jusr 1.45 cr. This will give per share sale of ~35 Rs. P/S comes to around 3.8. If we consider the latest quarterly report annualized, which is safe to do as the sales have consistently grown QoQ from 2020 onwards, annual sales will be 60cr (15cr Q1 FY23) This will give an sales per share of ~41 and P/S of 2.9. Based on these numbers it’s not too cheap and not too expensive either.

The thing imo is that no one invests in this microcap stock keeping in mind the current numbers and stats. This is too risky a bet to make sense of via current performance. This is a bet/speculation on the future potential of this business. Different people have different ways of arriving at that future value but it’s potential value all the same.

Personally I am holding from price of 65 and not expecting any big upticks anytime soon unless some hanky panky stuff plays out. But I’ll bestaying invested all the same.

5 Likes

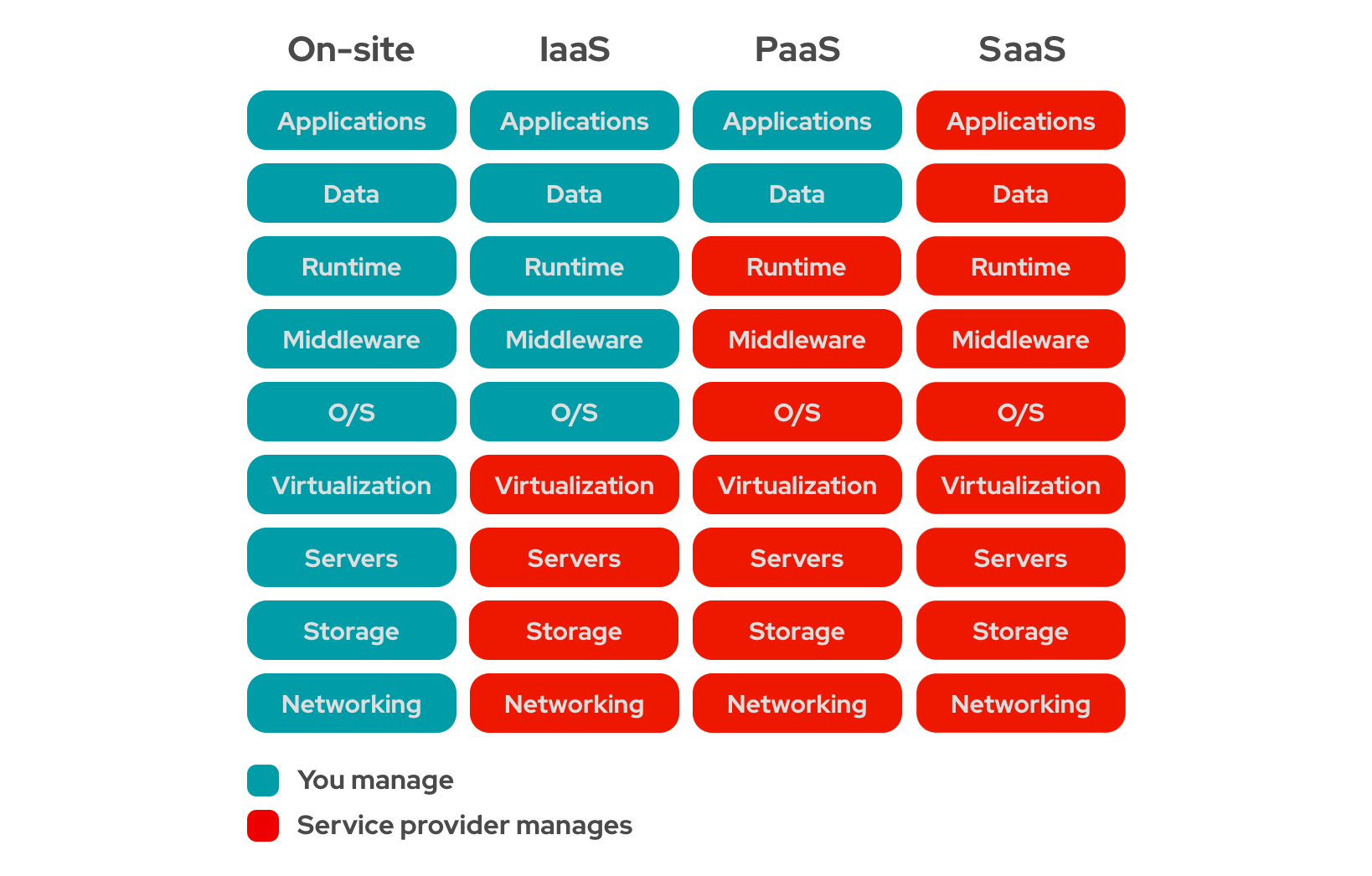

IaaS is asset heavy business here with AssetTurn of less than 1.

With OPM of 50%, they can keep adding assets (which are considered as having 3 years life on books giving ample cash saving to buy more assets)

Company can grow at (OPM-Tax rate) 'if demand is there".

I am not a technical person in this field but this seems a value chain

source : IaaS vs. PaaS vs. SaaS

More services you add, more revenue can be generated with lesser assets.

If co improves AssetTurn , this can be a very good investment and I think managment also knows the same.

Someone in AGM asked question mentioning co as a provider of Equipments on rent (Balance sheet shape similar to recent SME IPO of silicon rental), management answer was like consider us as a technology company and not rental co. Strong dollar is good when AssetTurn improves and bad if AssetTurn remains below 1.

Following this…

6 Likes

My two cents on the Co and management having followed the company since 2018. To start with SME platform is a very risky bourse to invest in. There have been companies that have been utter frauds and one can’t take big bets on one’s capital.

Coming to E2E Networks. I got interested in this company because it was one of the few startups in the tech space that was IPOing that too at such a small scale which is not usually the case. It was profitable and was listing at reasonable multiples (I think it was 5 times sales) and as usual popped on listing. The purpose of the IPO was very clearly stated that the it was an exit for the VC investors who had I think 30% stake in the company. Another interesting thing was that the VC firm wanted to partly unload their stake at the IPO and if I am not wrong continues to hold it.

I don’t buy at companies at IPO’s so stayed away but continued tracking. As is always the case the stock dropped almost 80-90% post listing in a years time as problems of sales concentration started emerging and sales.

I had already started buying the stock when it was 60% down and continued averaging down. My thesis on the company was this. You can compare E2E to Digital Ocean. Digital Ocean is a global IAAS/Manage Cloud computing business with a revenue of close to $300Mn with a MCap of $2.3B. Their sales is just above 1% of the global market for IAAS. If apply the same metric for E2E for the Indian market sales then it is less than 0.2% with lots of room to grow. If it gets 1% of the market then it can easily be a 150cr+ company with a MCap of 750-1000Cr.

Now for the margin of safety. The whole company was at one point available for 25Cr MCap with a sales of 30Cr. I started loading up and my Average Buying price of INR 27. At this point the CEO/Founder starting buying furiously from the market which gave me confidence to hold on. Although its not been easy holding it.

Now for the business model. This is a self serve model for customers they can buy compute power on demand without a lock in which is flexible enough for someone to not get into long term contracts but also at the same time at risk of discontinuation. What I wanted to see is how the recurring revenues are playing out and as you can see there is growth every quarter.

The other important things to notice is have a clear market strategy. When they had client concentration issues they were focused on the startup sector where there is fierce competition from the likes of Google/Microsoft/Aws which they have now pivoted to focus on SME’s which is not that attractive for these 800 pound Gorillas.

So all in all one has to monitor the management execution and track it for the next couple of years with all the tailwinds of data localisation, movement to cloud and generally competitive costs. Moreover most IaaS business is going to be commoditized to the point that features will be similar and price will become the decision point. This is where I believe that E2E is best placed.

18 Likes

Did some digging up on E2E networks. Here are the key takeaways:

-

Cloud computing market in india is Rs16000crs. AWS caters to Rs8000crs. E2E is focussed on the price sensitive Rs4000crs market which is a large TAM.

-

E2E Networks has no local competition and faces competition from international players like Digital Ocean (DOCN), Vultr Linode (Now owned by Akamai ) in India in the price sensitive segment.

-

Larger global players are AWS, Azure and Google Cloud

-

E2E Networks has scaled up and is a strong agile player in the public cloud infra.

-

Currently has 2200 active clients out of its 15000 customer base it has serviced till date.

-

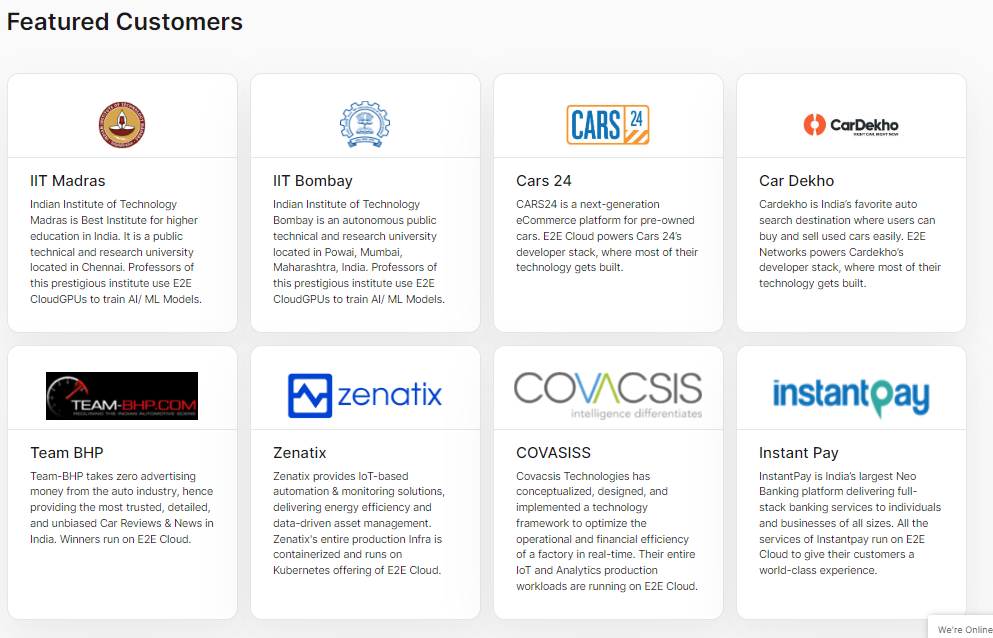

Some of the clients the company has serviced over the years

-

Company is guiding for Rs200crs of revenues in 4 to 5 years v/s Rs52 crs in FY22

-

Company is expecting to grow revenues in a band of 30-50% per year over forseeable future

-

FY22 EBITDA margins at 44% in FY22 but will go up as revenues scale up. PAT margin in 1HFY23 were 16-17% which will also go up as revenues go up

-

Depreciation very high as according to accounting norms. Computers and servers are depreciated in 3 years even though useful life is 5 years

-

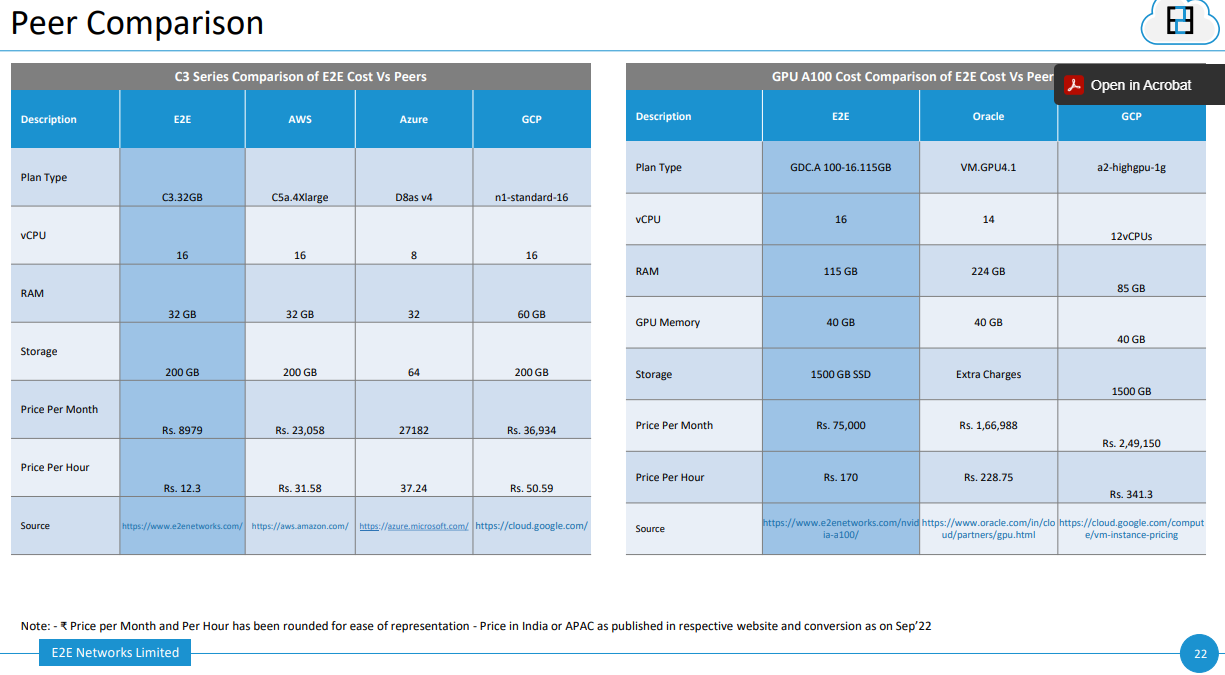

Key USP is it sells the cheapest cloud infrastructure in India

-

Key large investors are VC fund Blume Ventures with 12% stake and Airavat Capital with 3-4% besides promoters Tarun Dua and family with 58% stake

-

Investment portfolio of Blume Ventures here Startups - Blume

-

Company will do profits of Rs11.5crs in FY23 which implies it is trading at a P/E of 26.8x FY23E at current market cap of Rs309crs

-

Company is net cash with 26% RoE in FY23

-

Company has moved from SME to the main board.

Some of the current featured customers

Disclosure: Invested

7 Likes

My view (from earlier discussions with mgmt) was that the infrastructure was also useful for 3 odd yrs (and not 5) only as post that either the energy consumption also went up or technology would have upgraded by then

Seems like an imposter.

There are only 3 listed “internet/ e-commerce companies theme” in India which are profitable. Indiamart, Affle and E2E networks. Of the three E2E is the cheapest and growing the fastest.

Please correct me if I am wrong. I know its not an e-commerce company. But it is linked to the same internet/ mobile/ e-commerce theme

E2E can’t be considered e-commerce player as they are into cloud computing platform services provider similar to AWS.

1 Like