Then it has to show up in Goodyear India’s numbers, for me to take any meaningful action. You can see in my model that the growth estimates I have made are very nominal. As mentioned, I don’t try to predict anything.

If Chinese tyres start taking market space from Goodyear India, it will deteriorate their fundamentals. And on a half-yearly and yearly basis, I track the cash flows and fundamentals of the companies I invest in. If there’s a sizable change, I will notice. Of course, then I have to decide on whether it is a temporary or permanent phenomenon. I guess that’s why Warren Buffet said “Investment is simple, but its is not easy.”

I am learning and had learnt a great deal from your comments on various threads as well from others VP’s however there are certain points which i would like you to consider

Cupid -> depends on rubber & processing, uneven material cost as a % of sales, in 2015 it reports around 85% revenue from export in march 17 it shrinks to 20%

Good year -> depends on rubber & processing

Ion exchange -> Machinery susceptible for technology disruption depends on price of cyclicality of raw material low technology sector

Kovai Medical Center & Hospital Ltd Healthcare Services it has high Depreciation on medical equipments and localised customer base

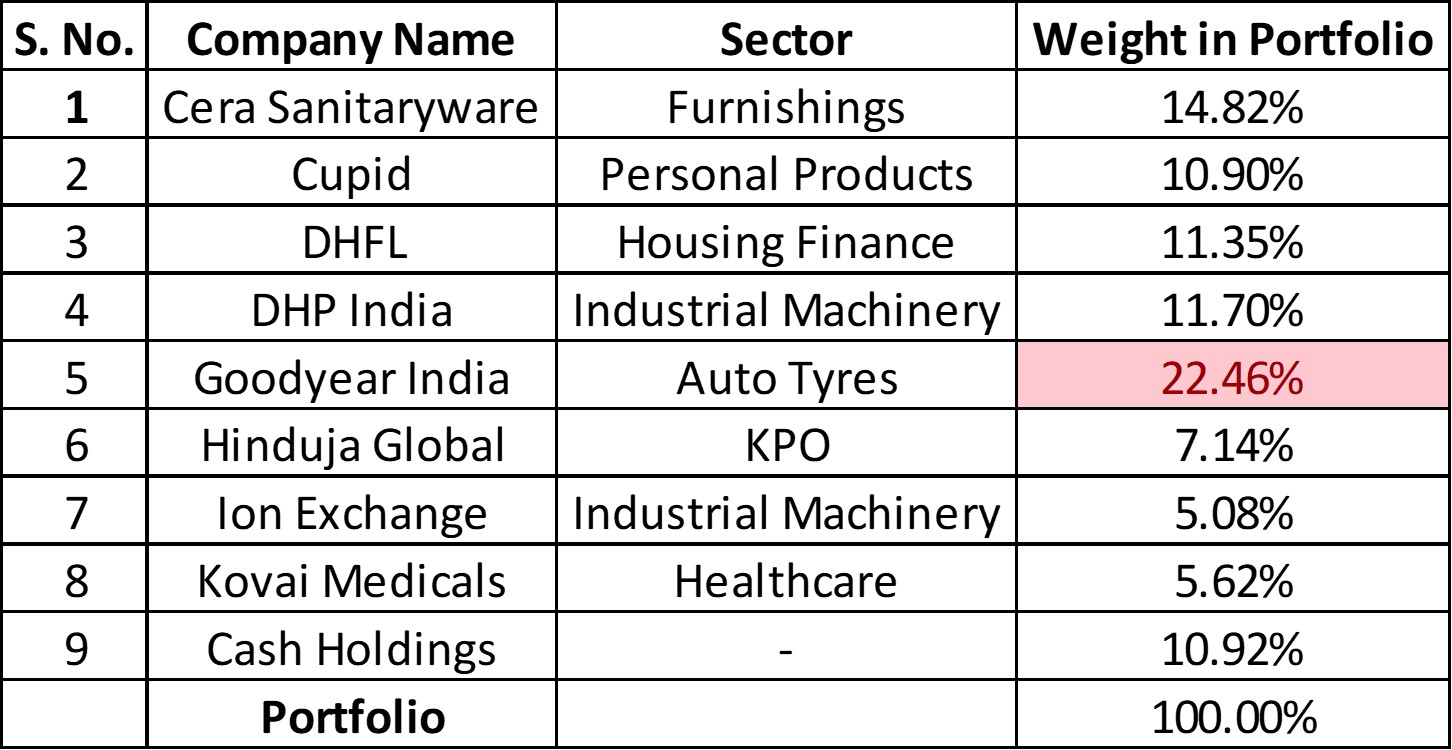

Only things in your portfolio which i like and appreciable bet is on DHFL and YOur cash holding %

What i learnt so far in this forum that select the industries where there is less dependability on crude and with few input variables so i try to stay away from processing industries and the industries which has high cost of operations with lots of debt e.g Banking / Airlines etc.

Since you are sitting on cash so you can take focus on ROTI KAPDA MAKAN Medicines and MONEY (Finance)

ROTI (depends on weather, international regulations, R&D )–Rice /Seeds /Agro chemicals (stocks are corrected )/Sugar stocks

KAPDA (depends on weather, international price of cotton, R&D ) — can be challenging as the textile is cyclic as you were exited the Kitex and had enough exposure to cotton /textile sector

That is exactly my concern. They have not shown agression in the past and the probability of changing past action is certainly not very high. Hence I would prefer investing based on proof of action. As Rome was not built in 1 day, we know nothing will change in 1 year. If we see positive action from management, we can increase stake even when price of stock surges ahead. This could be a risk averse alternative when we know management has not proved agression in the past!

Thank you for your suggestions. I will look into them when I get time.

However, I disagree with you line of thought regarding raw material prices. While the inputs prices definitely have some hold on the profits of a company, they’re the worst for commodity types businesses. In franchise-type businesses, the company can more or less pass down the price impact (Except when the raw material prices are abnormally high).

Regarding your specific questions:

You can look at Goodyear India’s historical OPM, which is has been fairly steady regardless of fluctuating rubber prices. As I have discussed several times in this thread, the management of Goodyear India is hell-bent on foregoing sales in order to control cost. This shows how prudent they are. Here is a snippet from their last AR:

Cupid is kind of iffy, because 3-4 years back, the company was a financial mess. I invested only when they turned their business around with good fundamentals. The uneven profits part is already discussed. They are an order-based business. It’s normal for them to earn lesser profits in one year and make up for it in the next 1-2 years. The management regularly addresses the raw material price point in their con-calls and they have systems in place where they purchase in bulk when required and reduce when they don’t.

Again, please look at Ion Exchange’s OPM history. If raw material price volatility should impact them, why is it not showing up in their finances? It’s because they’re a franchise and so, able to pass on raw material prices increases.

You will have to visit KMCH at least once to realize what kind of hospital they are. It’s a mammoth of a hospital and commands absolute brand recall in the city of Coimbatore. It also attracts people from other parts of the state (and world) because of increasing medical tourism in general. Their future expansion plans are a medical college and a new hospital in Chennai. Given the management’s expertise and experience in this industry, I’m sure they will succeed. I’m glad they chose to expand into their own circle of competence. You can see many companies these days purchasing or expanding into businesses they have no expertise in. KMCH is smart that way. Finally, for an Asset-heavy industry, their Working Capital Ratio is pretty small. You should check it out (For 2017, their WC Ratio was negative).

I don’t understand what you mean by ‘aggressive’. It’s not growth per se that creates value. It’s growth at a reasonable cost that creates Value. As I mentioned earlier, I don’t mind if Goodyear India pays out their Cash as Dividends as well. But since the management has actively started getting into the commercial tires segment, I would give them a few years.

That is not to say that I don’t like any other companies in this industry. I like MRF, obviously. TVS Srichakra, to a lesser extent. But these are not available at a good discount to my value. If they were, I wouldn’t mind diversifying into them. After everything is said and done, Value becomes the final frontier.

I think using DCF in companies with lumpy earnings like Cupid may not be too appropriate. DCF could probably work with companies with consistent and predictable earnings which I dont think is the case with Cupid.

My main point was that if I was to buy only a handful of companies in my portfolio and if my portfolio consists of a large part of my networth then I want these companies to be very stable and solid companies. I want to be absolutely sure of where to slot these companies. The best I can say about Cupid is its a dark horse and if thats so then I would not allocate too much capital to it.

Unless of course my total equity portfolio is a very small part of my networth and doesnt materially affect my financial status either way. If thats so I can go about experimenting in whatever way I feel suitable as it doesnt affect my overall financial health.

Regarding opportunity costs, once you remain in the markets long enough you begin to realise the importance of it. :Being patient is a big virtue in equity markets but there’s a thin line between being patient and being inflexible. In stock markets its very prudent to be flexible with one’s views if facts and environment chage or if investment thesis fails to play out.

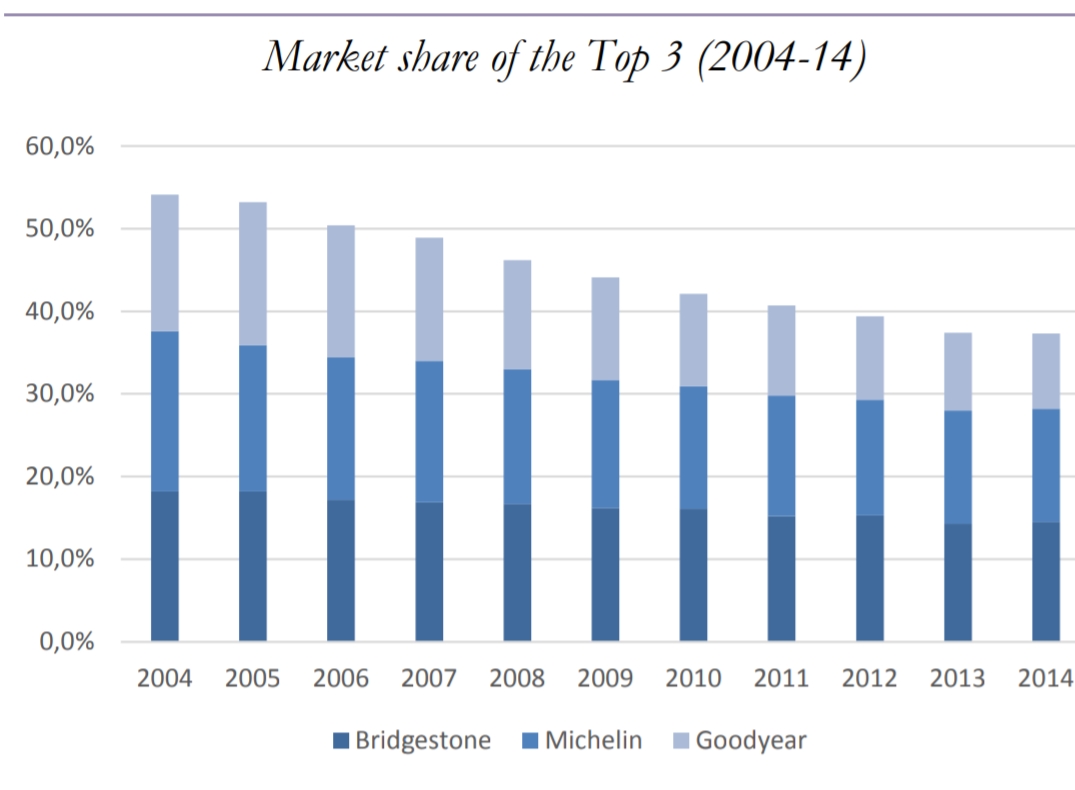

Let me explain some background on what I think about Goodyear. They have been de-focussing on farm sector which is one of their biggest revenue generator.Godyear globally is doing bad. Goodyear globally lost 17% market share between 2005 and 2015. The India business lost 15% market share in the last several years. They sold their Agri business to Titan in South America and Europe markets too. Losing market share in a segment that grows is not very good. Please look at both Goodyear India and the parent to see what is happening!

Please help me understand why Goodyear Inc., de-focusing on Farm Tyres businesses in some places affects Goodyear India. South America and Europe do not pose an opportunity to the level of India. India has a large opportunity for Tractor Tyres going forward. Plus, the company has additional cash to foray into the other segments to boot. India is too big an opportunity to ignore.

Do you have sources saying that Goodyear India lost so much market share in the Tractor Tyres segment? As far as I know, the Indian Tyre Industry was about 535 Billion in 2015. Assuming a nominal growth rate of 9% (Suggested in the report), we could say that it is currently around 700 Billion.

Farm Tyres form a very small part of it (Around 3-5%). Even assuming 5%, that makes the Farm Tyres Segment in India worth 3500 Cr. Goodyear India’s TTM Sales were 1664 Cr, which shows that Goodyear India has a 47.50% Market Share in the Farm Tyres segment in India. I would be happy to see real data pointing otherwise.

Precisely, I agree. I do not see that it has happened with Cupid as yet. As mentioned earlier, I pay more attention to cash flows and fundamentals than Accounting Profits. If those deteriorate, I will not hesitate to take action.

The loss of market share I mentioned includes farm as well as trading business. So that includes all the categories. Tractor tyre sales in India is less than 4% and hence getting data may be hard. I am sure if we dig hard, we could get a ballpark. I don’t track this segment and so I don’t know.

If parent is not doing well, the R&D support to India will be affected. After all, the PV segment drives R&D budget for most companies and the outcome flows to farm segment. The parent has control over India operations and the global mindset flows eventually to India. We have seen the indirect impact on many companies controlled by MNC process flows. Some examples I can think of are whirlpool, GM, Carrier, etc.

Tyres Market Size in India = Rs. 70,000 Crores (Rough assumption based on ICRA report).

Farm Tyres Market Size in India (Less than 4% of total Tyres Segment, as mentioned by you) = 70000 x 0.035 = Rs. 2450 Crores

Goodyear India TTM Sales = Rs. 1664 Crores.

Goodyear India Production/Trading Business Split:

This purchase hinged mostly one 2 things (Which are almost always the same 2 reasons for many of my investments): business longevity and valuation comfort. There’s a lot of headroom in the Sanitary-ware space. Kajaria Ceramics was another company that I considered, but I found Cera to be in a better financial position.

Even for a company their size (3500+ Cr), their R&D is still focused on controlling Margins (Annexure to Director’s Report in their latest AR). God knows I love companies that control costs like an obsession.

2. DHP India

A no-brainer kind of investment, I’d say. The company produces Gas Pressure Regulators for domestic and industrial use. I’d been tracking the company since a year back (When it was Rs. 350), but got around to investing just now. They could do a lot more to improve the presentation quality of their AR, however – it’s just plain confusing.

3. Hinduja Global Services (HGS)

The company used to be a BPO for companies in the US/UK. Recently, they’ve upped their game by providing Healthcare Analytics as a service. Since I work in the Analytics industry, this is falls right under my Circle of Competence. However, this sector is prone to constant disruption and only the most vigilant survive. This justifies my comparatively smaller stake. I might increase the stake here based on further inquiry.

My top 5 holdings form 75% of my portfolio and I’d mostly like to keep it that way. I still hold 11% in cash and accumulating more as I go along.

DHP India looks very interesting, loved the clean balance sheets. My question is mainly related to the growth opportunities in the segment. It’s top line for Fy18 is similar to what it did in FY14. Are there any triggers which say growth can pick up in coming years? With low dividend pay-outs and low past growth- what would be key triggers to unlock value here for minority shareholders?

I don’t go by business triggers or “P/E Re-rating opportunities”. For almost all of my investments, I ask very few baseline questions before diving into Valuation (Which is a final frontier for me). I’ll perhaps answer them with DHP India.

1. Do I understand this business? Yes, their business is fairly straightforward. They produce Brass Regulators for domestic and commercial gas cylinders. Your regular B2C and B2B business. Nothing fancy. I don’t see opportunities for disruption in regulating a gas cylinder.

2. Does the company have good long term economics? As per my understanding, yes. There’s still a lot of headroom for growth. Apart from the growing poor-to-rich population, LPG being touted as the next big thing in day to day consumption (Next to Oil). You can search online and verify the numbers, should you require. Also attached to this point is the company’s moat. It’s very difficult to evaluate the moat of supposedly ‘boring’ companies like this. But the consistency in Financial Ratios are a good indicator (Specially the OPM and excessive return ratios) offer good clues.

3. How well does the company operate? The necessary Ratio analysis checklist. I usually do a common size analysis and otherwise check the most important Ratios. The only red flag I found for DHP India is that their Cash & Cash Equivalents form 15%+ of their Market Cap. Well, this is actually a positive, but the question remains whether they can reinvest all that quickly (Doubtful) or return it back as dividends (More plausible).

4. Does the company have an appreciable work culture? I found it very difficult to get online reviews of the employees in this company. However, I also didn’t find any complaints or otherwise as well. The salaries they seem to be offering fresher candidates for data entry jobs seem to be sufficient (Range of ₹12k-21k). In their AR, it’s suggested that the hike in general employee salaries is around 20%. So I’m assuming that the employees are at least satisfied on that front.

Of course, a disclaimer is that I place a great deal of importance on financial analysis and Valuation over everything else.

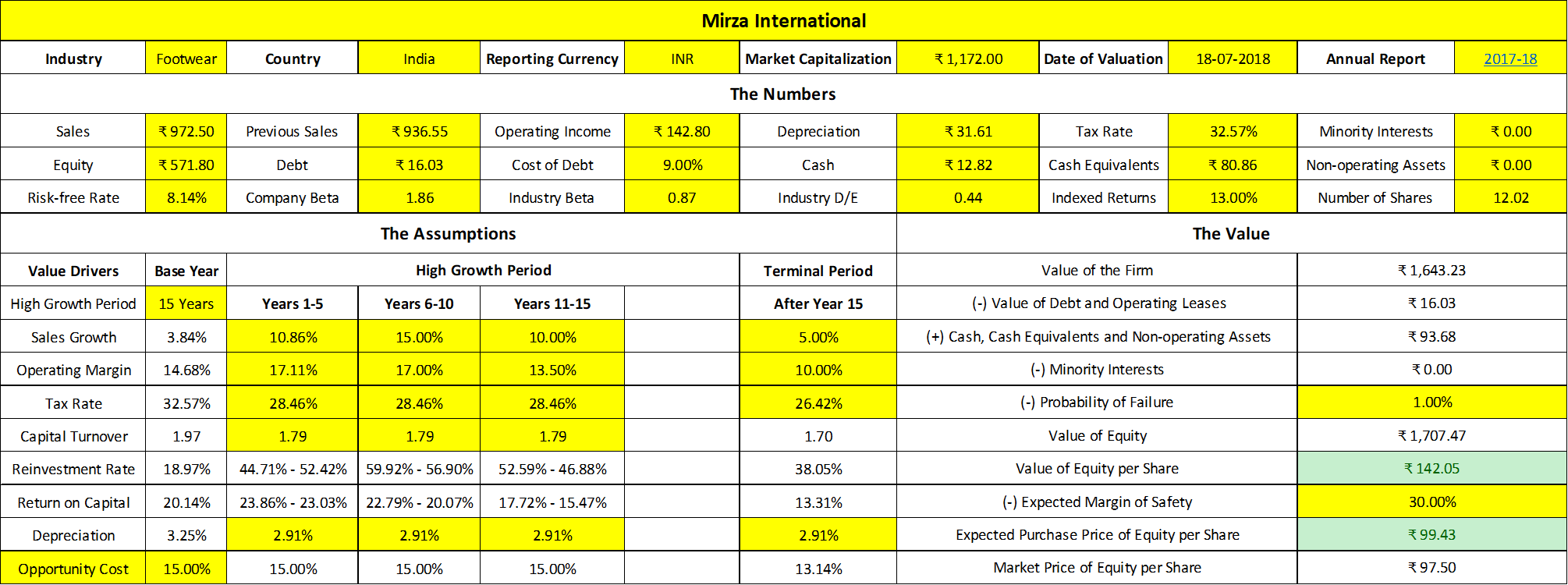

Let me confess by saying that I’d much rather buy Bata India than Mirza, but the only thing preventing me is Bata’s overvaluation. However, Mirza is no slouch. Creating a new, re-callable brand of footwear when Bata is still very much a household name is no mean feat. I think the footwear industry itself has a massive demand to fulfill in the coming years. Regardless of Bata being a vastly more dominant player, Mirza will have its fair share of feet to protect.

I’m not very gung-ho about their foray into retail and the abuse of the RedTape brand for selling products other than footwear. So, this is my one concern about the company. But I won’t pretend to know how to utilize the company’s capital better than the management. I see no downside to giving the management more leeway.

I don’t think I’ve ever posted my Valuation of a company here. But here’s how I Value Mirza:

Hence, I feel comfortable having bought Mirza at a decent Margin of Safety (30% is usually my base requirement for MoS, unless the company has a long history of consistent numbers).

Bhai, if the share price of Mirza reaches Rs. 145, say 4 months from now… Will you sell it, since it’s at fair value (acc to your model)? Or would you run your model again - though I’m not sure how many “fundamental” levers in a multi-year model you would really change just 4 months down the line.

P.S: For simplicity’s sake, let us assume the share price rise was simply due to P/E expansion (or equivalent)

That’s a very good question. I won’t. And here’s why.

Imagine that you have a super-computer that stored data related to all the asset classes and products in the world. At the click of a button, you could re-allocate your portfolio so that you always earn the best returns and enjoy the full benefits of diversification. As an astute investor, that’s all we’re trying to do. Except, we’re not super-computers. We work extremely slow (In supercomputer terms).

I purchased Mirza at Rs. 99 and demanded that I earn at least 19.5% on my investment (Excluding the Margin of Safety). If it goes to Rs. 145, that could mean that my expected returns for say, the next 10 years, could drop to 18% instead. Now, what action should I take?

In an ideal world, I should try to find a stock (Actually, I should find any asset):

Which is as good as Mirza in all objective/subjective factors (Economic Comfort)

As well as providing a return higher than 18% at the least (Valuation Comfort)

While being in a industry I understand (Circle of Competence)

And as much as possible, also does not have the same procurement/supply/demand pattern as any other company I hold (Diversification benefit)

If I was a supercomputer, I would immediately identify that opportunity. Since I’m not, it takes me a lot of time to scope for it… maybe 4-5 years, maybe a decade. All the while, I also have to track my earlier assumptions for Mirza actually playing out or corporate governance issues popping up. Instead, if Mirza actually starts performing wonderfully, the benchmark for my objective/subjective factors for scoping would increase, making it even more difficult for me to find a replacement.

This answer is actually confusing if you think about it in the short term, because of course, you think about the short term only if you have the trading mindset. The better approach is to focus on the long term, like the owner of the business would, and ask yourself these questions. You will also realize that price isn’t only thing that drives sell decisions. The objective/subjective factors also matter. Little things like transaction costs and taxes also matter, although to a small extent.

The most important thing when talking about long time periods is compounding for sure. What if I knew that Mirza will return 19% over a decade? I might invest a small part of my portfolio. Two decades? Three decades? What if I somehow knew that Mirza will return 19% over my entire investing career? I would most probably invest my entire portfolio in it. You see, while 19% isn’t such a great return for 5-10 years, it is a phenomenal return to earn over 35-40 years. If, after holding Mirza for a few years, I find that kind of RoIC consistency, that will also restrict my selling process.

With all that said, it doesn’t mean that I will never sell Mirza at all. Based on Mirza’s Credit Rating, I would judge it to have a Cost of Debt of around 8-8.5%. At that level of discounting, Mirza’s value becomes Rs. 350 (Rough estimate). If Mirza goes to Rs. 350, even 6 months from now, it means that the market thinks Mirza’s Debt and Equity have the same risk, which is ridiculous. So, I would probably sell into that ridiculousness. Of course, I would also sell if Mirza isn’t performing as I expected it to or if the promoters turn shady, but the Equity-Debt risk equivalency is a mechanical sell limit I always have in the back of my mind.

If you’re still reading this, you might as well read some wonderful articles on the ‘art of selling’:

As a concluding note, I would say that everything in investing is a function of Opportunity Cost. For the most part, Opportunity Cost is a percentage. However, Opportunity Cost is also subjective in many important places like management capability, financial acumen, economic roadmap and so on. If you’d like to hear more of my rants on the topic, click here.

Thanks mate, got it. Btw, did you use 19.5% as cost of equity for your DCF model (since that is what you demand), rather than use all those beta-sheta?

The other thing I noted is that you are saying (though not explicitly) is that you have some margin of safety built into the discount rate, not just the price.

I suspect the debt-equity equivalence will be a very rare thing…more likely the fundamentals and cash flow expectations will improve so that the equity component becomes more valuable. In model terms, since your cash expectation goes up, the thing that you discount (even at 8%) goes up and your “all debt value” will not remain at Rs. 350 anymore. The problem comes when you don’t judge those cash flows properly…which is always the most difficult part, isn’t it?