No, I have not. If I do, I will post it in my blog or here.

Of course, I don’t disagree. IndusInd is definitely in the wrong, but they are starting to admit it and do something. My point is that it is available this cheap because there’s been a slip up. When everything is peachy, the bargain will be gone too.

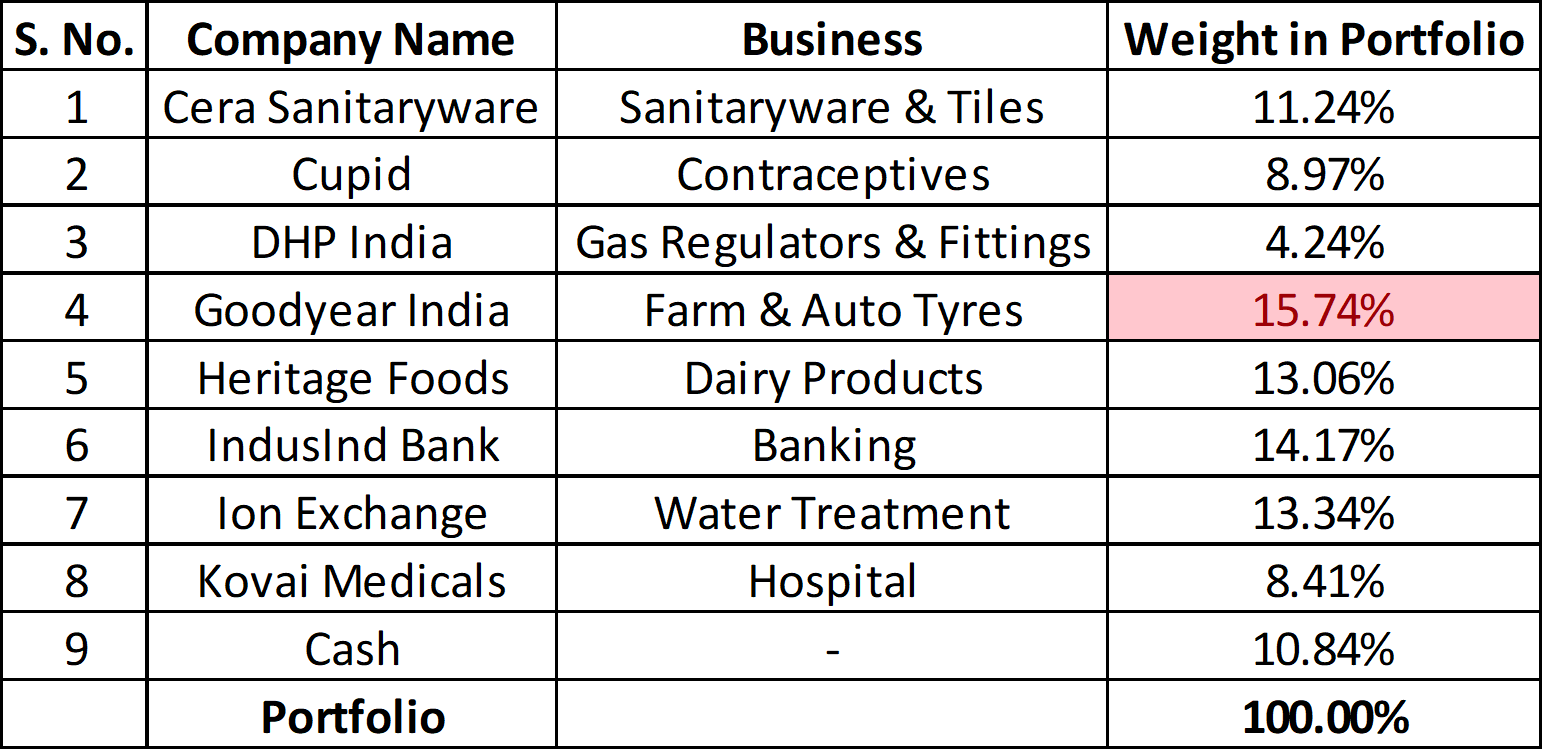

Hi Dinesh, from your posts, blogs and Twitter, I understand that you are a long term investor. From your initial investment (starting of this thread), you have removed hdfc and dhfl from your portfolio and managed to reduced your holding in goodyear and cupid. I don’t particularly mean reduced, but in the context of balancing your pf. My pf is just like your initial pf and I like to balance it out just like the way you did it. How did you manage to reduce your biggest holding: did you sell or increased your holdings in other stocks in due course? Also just like @axiskumar, I am waiting for your analysis on B&A.

Thank you in advance.

Venkatesh

I sold off HDFC Bank and DHFL completely. I have never sold a single share of Goodyear India or Cupid from the initial purchase. I suggest you look at my post about how I invested since 2016.

Long story short, I invested in Goodyear India and Cupid starting from 2017, but with (Competitively) small amounts. The bulk of my current PF (I’d say about 75-80%) was invested only during the last year. So, it may look like I sold and re-balanced something, but in effect I just increased the size of my PF, while also allocating money to other stocks.

I have replied to him already. Please look at the post above.

It’s a Net-Net kind of purchase, attractive solely because of the cheapness. I don’t think either B&A or B&A Packaging are great businesses. They are both mediocre at best. That doesn’t warrant a deeper analysis. There’s not much to analyze anyway.

Hi Dinesh, what was your thought process & what triggered you to invest majority of your cash in a single go, pre-election results?

Do you not expect the prices of the scripts you bought, to go down or at least dip to the same level in near term owing to macro economic factors or major issues such as possible defaults by corporates in Indian economy?

I was mostly waiting for the results from IndusInd. I was convinced that the price was attractive, but apprehensive because they still hadn’t provided enough for ILFS. After the results, I clicked the ‘Buy’ button as fast as I could. That purchase itself made up ~11% of my PF. Heritage’s result was also on the same day. I purchased more of it then. The remaining ~4-5% I allocated to Cupid, Dhabriya and Ion Exchange.

So, mostly it was because my two largest pre-election purchases also had their Q4 results on the day before the election results i.e. Just coincidence.

I guess Goodyear’s loading up of inventory at (comparatively) lower RM cost levels has finally helped them out massively. Let’s see how things play out from here.

Goodyear India also plans to enter the PV segment and other fringe tyre segments soon (They are already trading here… they’re planning on manufacturing). It should be an interesting couple of years ahead for the company.

I don’t think I’ve mentioned this here. While I’m not too keen on using Screens, I do have a couple of Screens which I have built myself. ~80-90% of my investments do not come via Screens, but for instance, DHP India first appeared in a screen and I have since analyzed and invested in it.

My Screens have been public for a while, so I thought I would share them here.

Please note that, for the BFSI Screener, I use the Debt-to-Equity Ratio to filter out Non-BFSI stocks. But sometimes, a Non-BFSI stock with a very high leverage may pop up here. You should ideally ignore it.

I also hope that you see the single most dangerous flaw with stock screens in general: they are mostly based on numbers. Numbers are not everything in investing. Here are some important things you will miss out on if you are obsessed with stock screens:

Information: Screens don’t show every good stock out there. You have to constantly read books, interact with like-minded people and be up-to-date with news. This way, you are in touch with broad industry trends and specific, curious activities in the business world. In fact, you are more likely to generate investment ideas this way than through a screen.

Research and Analysis: A stock is a story with numbers. You have to bring the story about the company to the table and set it against its numbers. Everything ranging from Management Capability to Competitive Advantage show up in the company’s historical numbers. You should analyze them separately (Ratio Analysis), as well as against competitors (Competitive Analysis) and ask the right questions about anything that’s odd.

Circle of Competence: If the numbers and the stories about the company don’t correlate with each other or if you don’t think you can make them, then the stock is probably not for you.

Valuation: Although the screens contain filters for valuation, you still have to value every company yourself, just to understand how the different parts create the value of a specific company.

Margin of Safety: Only if your expected purchase price is significantly above the current price of the stock, it makes sense to purchase it.

Conviction: The stock you chose may disappear from your screen permanently. But it’s you who will be left holding the stock. You should follow the company’s activities and look for chances of increasing the stake or exiting it.

No major updates this month. I wanted to invest more in IndusInd, so I sold down Dhabriya Polywood (Which I wanted only to track anyway). A minor mistake on my part to invest too much (~7%) in a stock I simply wanted to study for a year.

IndusInd has come up with their FY20 Q1 results. Overall satisfactory results. The BhaFin merger is complete and their loan book forms ~6-10% of the bank’s loan book. Synergies to follow in consecutive quarters. Othrwise, a ~18% growth in EPS and most other metrics are stable. The only slip up is that I expected the bank to provide more this quarter for the ~Rs. 2000 Crores NPA still on their books wrt entities like Essel, DHFL and some construction firms. But in the concall, the management was confident that they are still standard assets. There is a recovery plan being drawn up for DHFL, so I suppose they are at least partly correct. Let’s see how things go from here. I’m likely to invest incrementally more in IndusInd if the price falls back for whatever reason (Clearly, the market didn’t like the stock on the day of the result).

I managed to raise some more cash, but nothing to write home about. I expect to raise a few more too in the next one or two months. I’m hoping that the market remains choppy, so I can find opportunities to invest.

Both Dhabriya and B&A Limited are only for ~1% or lesser of my PF now, So I have taken the liberty to exclude them from the above. They will remain tracking positions until I get more conviction (B&A Limited is likely to stay the same. But I would like to see better execution from Dhabriya before choosing to invest more again).

I’ve mentioned this in this thread earlier. I also invest in a couple of Large Cap Mutual Funds via SIP. They form about 25% of my overall investments in Equity. So, my personal PF is always about 70-75% and my MFs 25-30% of my total investments in Equity.

Again the reason for why I invest in MFs has also been mentioned earlier. I don’t know how good I am as an investor. I suppose I will figure that out say 10-15 years down the line. So the MF SIP acts as a buffer, in case I decide I’m better off just investing in MF SIPs (Hopefully not).

Finally, I don’t see a problem with investing in mostly Small Caps. But I understand what it implies - it implies that I may end up investing in mediocre / bad companies more often than in Mid / Large Caps. I should only hope that I get out of terrible investments quickly and hold on to good investments so they can compound. So far, I have been able to get out of terrible investments fairly quickly. I hope I continue doing the same.

I am fully Invested in Equities too. Out of all the asset classes, I understand Equity and Debt the most probably (Apart from Cash instruments). So no surprises there.

Good to see that full investment in equity, do you have a thread on your portfolio? Pls share link as I would really like to read. If not, can you pls share your top holdings? Thanks