In addition, it was mentioned by Bimal that there was mandatory BIS certification requirement for Boric Acid sales which was notified in Q1. The company has finally got BIS certification but, in process full Q2 Boric acid sales were lost this has also lead to reduction in topline in Q2.

any views on the Q3 results. the performance has taken a significant hit… top line down by ~22%… the declining trend has continued from Q2… is this just the impact of global slow-down or any other issue impacting the performance… any insights.

@rohitbalakrish_

1 Like

The performance needless to say was bad. I was able to speak to the company and sharing the below points for everyone’s benefit.

- Demand environment was very bad. Their customers’s customers were not buying. Hence the overall volumes were down. Speciality chem volumes were down more than commodity volumes. However have not lost any market share to the competitor. This is not a representative quarter and the general slowdown across the world impacted. Borax volumes also didnt pick up much.

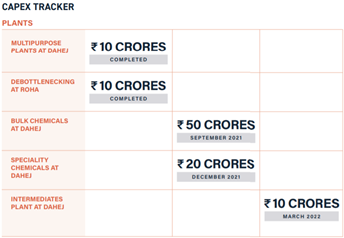

Have started the capex of multi purpose plant and Sulphuric acidin Dahej and working to finish it soon.

Employee costs were up because of bonuses from the last year high profits.

Overall long term story remains. Volumes have come back and expect to fully recover in Q4/Q1.

4 Likes

Rohit Hi,

Do you have an idea as to the possible impact of the corona fiasco on DMCC? Also, why despite being a strong brand in Borax chemicals they have fared poorly in boron even after several years of merger scheme?

Also, why the specialty chemical sales are not picking up ?

Sorry for asking you all this but seems that you can help guiding us on this one.

3 Likes

Hi Praveen, I don’t think there is anything specific owing to Corona Virus for DMCC- overall chemical prices are coming down- that may impact them but apart from that nothing structural I would think.

On Borax their strategy is to get into more down-stream products- like how they did with DMCC in sulphur. Boric acid is a commodity and won’t change the fortunes of this segment. They have been slow on the execution on this segment. But they still seem hopeful on introducing new products.

W.r.t Specialty chemicals - My understanding is that they are growing well. Sulphuric acid prices were up in FY19 and that contributed to the higher commodity chemical sales so as a % spec chem may appear lower. Good proxy to track the spec chem sales for the co are exports

The last two quarters have been tough for the company - hopefully that should reverse soon.

Hope this helps.

9 Likes

Thanks for the summary link! I did not understand this crying about China. They make 35%+ RoE/RoCE so why do they think they are not competitive against China?

As per the concall, Bimal Goculdas mentioned that China has 13 % export subsidy and this makes them more competitive . Apart from that China’s cost are already very low including power cost ,including their interest cost.

1 Like

Well, as an investor you would worry about the returns the company makes and not the selling prices and individual product margins as such. Sure that presents an upside potential for the company when these subsidies get reversed by China. Let’s be clear that no incentive/subsidy can be open ended anywhere in the world incl. in China.

8 Likes

Q4FY21

Investor Presentation

Concall Transcript

Concall Audio

- Impact on margins due to high input costs (raw material costs increased ), these prices are passed on to the customer in the next quarter

- Focus is purely on Sulphur chemistry (Capex of 100 crores on track , Dahej and Roha plant will have identical capabilities )

- Revenue mix will be in the range of 65%-35% (Bulk-Speciality Chemicals)

- Out of 100 crore capex 2/3 will be debit and 1/3 is internal accrual

- Some delays in equipment supplies so the full impact of the capex will not be seen in the FY22 fiscal

- Initially commodity chemicals comes online followed by speciality chemicals

- Purpose of adding sulphuric acid capacity (when asked about strelite closed their plant and Amal their competitor setup 300 tonnes plant ) is not for the sake bulk supply instead it is for captive consumption (50% ) to generate downstream products like Oleum, Sulfur Trioxide, Chlorosulfonic Acid and then react these with organics substances to make speciality chemicals

- From 22-23 moving to new tax regime

- Final Dividend 0.50P per share

Boron business

Raw material crisis and really hard to procure at the moment Availability technical grade boric acid - focus is on downstream stream products for that we have to do backward integration to produce technical grade boric acid

We are not able to import this acid due to government restrictions (not easy to obtain import license ) currently 50% capacity utilisation , impact of 5 crore annually on the bottomline due to raw material unavailability

Sufiric acid

90% capacity utilisation

Some of the specialities are close to 100% utilisation

Amides business

Stable and growing no issues

Thiols

Stables (new capacity addition)

Sulfone business (Very good visibility in the future )

This is very badly impacted, this speciality chemical is used on thermal papers. For ease of understanding, thermal paper rolls are used in the till receipt, a receipt that you get in any of the super market, these receipt printer doesn’t need any ink catrdiges to print, but the paper roll is thermal paper roll. Due to slow down in the hospitality industry like air line tickets, sports etc… there are not tickets being printed since covid started so there is huge impact on the thermal rolls business

Key Learning’s

Sulfone chemical used in thermal paper

Boric acid is used in glass, ceramic etc… , government is not allowing others to import because there is limited availability and to protect these businesses to have the necessary supply. Industry is contesting " But our argument is that the government is losing much more by way of value and revenue by holding back the downstream product especially since there is no raw material of boron available in India. But so far we haven’t been successful. "

19 Likes

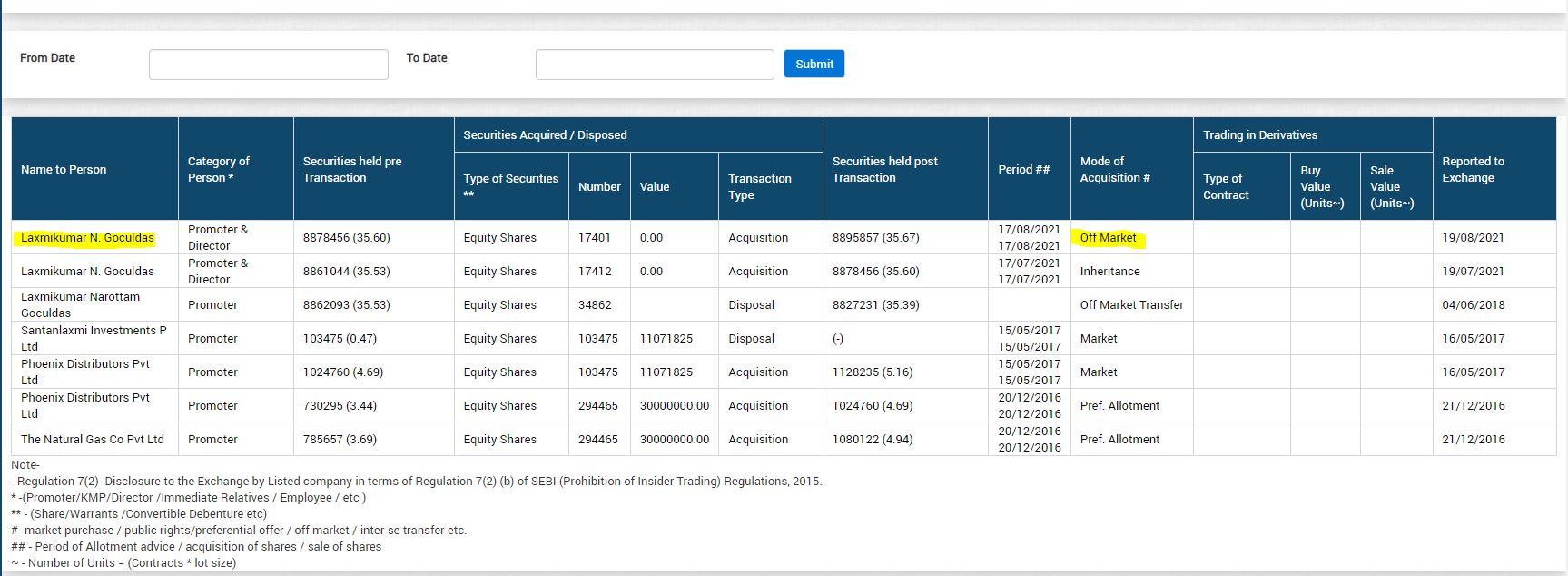

It’s clearly mentioned off-market which is not the same as open market.

An off-market transaction is settled between two parties on mutually agreed terms and the clearing corporation or the stock exchange is not involved.

1 Like

Important Notes from 2020-21 Annual Report

Strong demand for their bulk and specialty chemical products, as well as strong performance, was driven by volume growth, better realizations, and improved product mix, contributed to resilient numbers.

Specialty chemicals business witnessed a good year owing to strong volumes, contributing ~65% to the topline. Strong demand from export markets will augur well for margins in the coming years. The company expects investments worth ₹ 50 crores made in this segment to yield asset turns of more than 2x and the company hopes to achieve optimum utilization by end of FY 2022-23.

Bulk chemicals business witnessed moderate volume growth despite the majority of their customers shutting their own operations in Q1 FY 2020-21. The upcoming 350 TPD capacity shall be the last capacity expansion in this segment for the foreseeable future. However, the bulk chemicals plant will be set up first, which will result in a higher contribution from this segment in FY 2021-22. The company is focusing on chemical intermediates that generate 30-40% of ROCE.

The company has planned to undertake capacity expansions worth ~₹ 100 crores at their Roha and Dahej sites. In Roha, the company will undertake debottlenecking, whereas, in Dahej, we will set up multi-purpose and dedicated plants for bulk chemicals, specialty chemicals, and intermediates.

Focusing only on chemicals, where the Company envisages EBIT margins of more than 30% and a payback period of no more than three years. Planned a capital expenditure at the available land parcel in Dahej to expand its capacity in the specialty chemicals segment.

The company plans to deploy incremental capital only towards specialty and downstream products after the completion of the ongoing CAPEX. Expansion in sulphuric acid will be a one-time investment. It will cater to the captive needs for downstream products for the foreseeable future. For new products, the company has set filtering criteria where margins must be >30% and a payback period of less than three years.

Sulphuric acid is a hazardous chemical and its manufacturing and handling require high levels of technical know-how and skillset. We have been in the business of sulfur chemistry for over 100 years and created a brand name for the company in a commoditized market. The CAPEX will allow us to ramp up their operations and reach optimum capacity utilization for their bulk chemicals plant in less than six months.

The majority of the specialty chemicals sales are under long-term sales contracts, with pass-through clauses (for raw material fluctuations) with a lag of one quarter. The increasing share of specialty chemicals in their overall revenue will reduce volatility and margin fluctuations.

Revenue Breakup

| FY 2020-21 Geographical Breakup | |

|---|---|

| Domestic | 68% |

| Exports | 32% |

Revenue breakup product-wise

| Particulars | Q1FY22 | Q4FY21 |

|---|---|---|

| Sale of speciality chemicals | 55% | 64% |

| Sale of bulk chemicals | 41% | 35% |

| Other Operating Income | 4% | 1% |

Specialty chemicals contributed 65% to the top line as compared to 55% in the previous year. The planned capital expenditure in this segment will begin commercial production with a lag of one quarter from the commencement of the bulk chemicals plant.

The Company has further decided that a major part of all incremental capital expenditure will be done for expansion in specialty chemicals. Strong demand from export markets will augur well for their margins in the coming years.

Key points to sum up

- Great management with a clear vision to grow their business.

- Huge expansion planned up.

- High profitability productivity niche molecules and chemistry.

- Company has marque clients – Alkylamines, Deepak niterie, IPCA Labs, Deepak fertilizers, excel industries, sun pharma etc.

- Major capacites to come online by March 2022.

36 Likes

- Price increase will be passed on to the customers in the next quarter (all the contracts are on quarterly basis )

- Dahej plant expansion is delayed due to floods and covid related equipment supply delays

- Roha de-bottlenecking is done

- R&D -

- Sulphones (market demand is very slow)

- Bulk chemicals it is not easy to pass on price increase

- Specialty chemicals price increase will be passed on in the subsequent quarter

- There is no annual shutdown in this financial year

- New capacities will start contributing to the revenues from the current quarter Q3 FY22

- Topline growth (Price or Volume driven ? ) - {specialty chemicals growth is a mix of price and volume driven )

- Amines good traction , thyoles not much due to RM issue

- Demand side is no issues at all

- Boron side the issues are still persist

13 Likes

Nice article.

One sentence tells about this company is that… “Great management”

Even though it is a micro cap stock, it has a very good corporate governance, visionary management, vast experience, speciality chemical factor etc., all are very important points to consider a stock.

6 Likes

5 Likes

₹ Out of 110 cr capex, 70 cr completed and effect will be seen Q3 onwards

₹ Remaining 40 crs will be deployed before/after Q4.

Plant Commissioning news came out and investors can expect good numbers from Q4FY22.

With thanks

Be and Make

2 Likes