they mentioned during concall that they getting around 2000 cr per months as EMI collection so if we take 12 months and avg 2000 cr pm , it comes to around 24000 cr for a year approx.

but that means no new lending activity no growth so even if it does not default there is nothing much that’s left from investor perspective I guess

-

No serious institutional investor will buy or sell on cobrapost or any other leaks. Investors and Promoters are often a call away. Looking at last few days, there is institutional selling happening. So that raises serious doubts.

-

I will not trust any auditor (speciall big 4 and the extended large ones) and Credit Ratings ( they are no different than mainstream media) . Last but not the least, Investment offices of Banks, Lending departments, Pension Funds, Family Offices etc are most gullible. They are run by boys in suits who work on salaries and incentives. They will do whatever it is required to earn incentive. If lending target earns incentive and there is enough cover ( like AAA), great.

There are enough and plenty of examples of failing, failing en masse . It is a herd. Just like Top VCs, Top Law Firms and everyone else is swept in a hype wave. -

Last but not the least, there is nothing from management which helps. Rather each of their reactions so far are shades of grey.

I am provisioning for DHFL loss in my portfolio.

How do you provision for losses??

1 Like

https://www.morningstar.in/posts/50930/investors-need-not-panic-dhfl-essel-group-news.aspx

Let’s stay calm and stay away from noises, and hope dhfl comes out of these difficulties…

1 Like

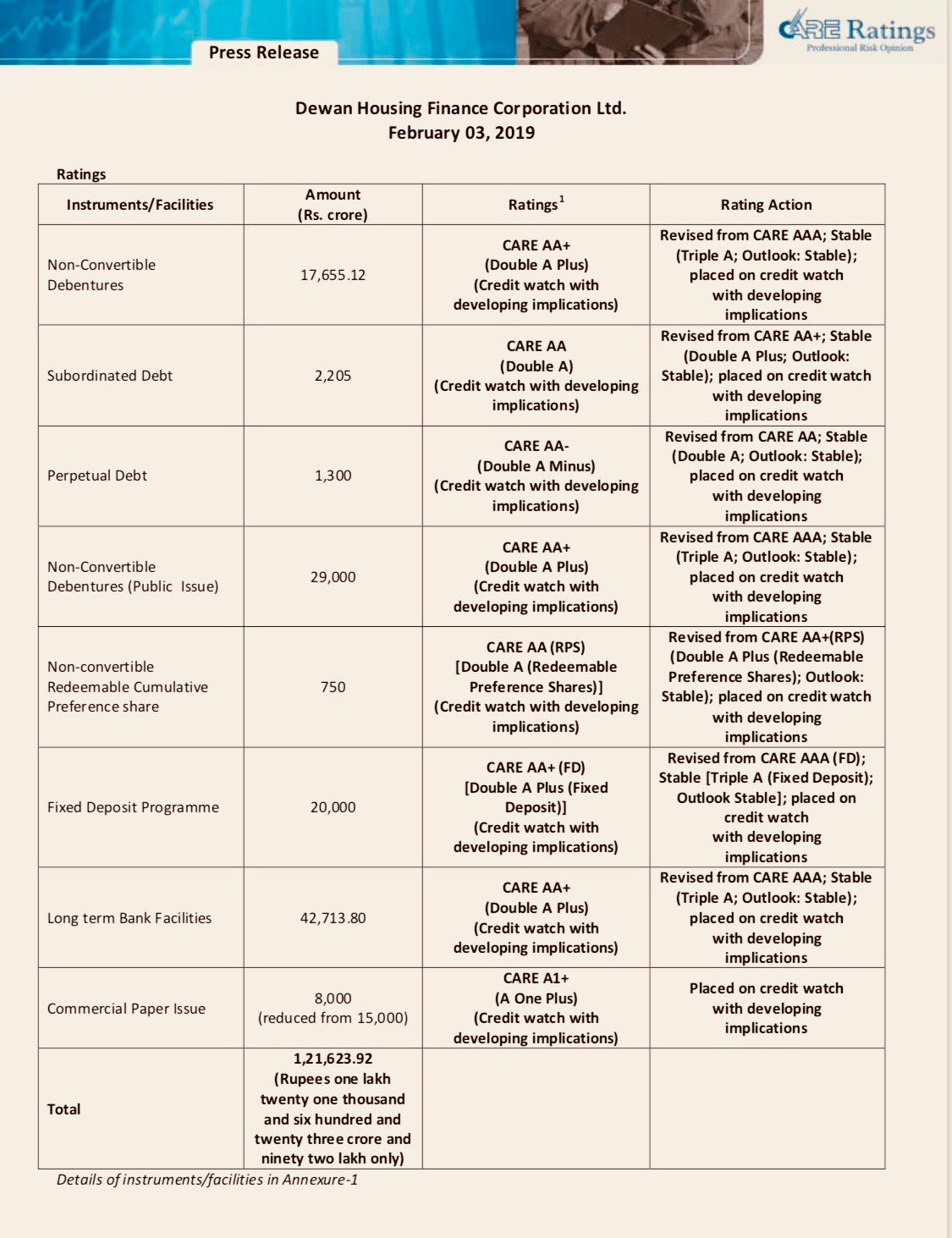

Rating update by Crisil

Crisil added it to watch list with negative implications. They did not downgraded yet. But this is bad enough to further spook the market.

If you read the report based on analytics keeping noise aside. Data doesn’t look so bad.( provided there is no real fraud)

This is now more integrity ethics corporate governance issue. Will dhfl be able to gain the trust of institutional borrowers or not?

1 Like

Hi Guys, Can anyone please throw some light on is there any hope for NCD holders in such situations that there capital is protected if there is no fraud and company survives this bad time? I understand shareholders have to wait a long long time now if no fraud

Also, If one can see, the DHFL NCD are trading at 25%+ YTM? and that too is a AAA rated?

Guys, the ground level situation is not good for DHFL. Got to know this from one ex employee of DHFL who has recently joined another NBFC. As per him, DHFL is not disbursing any loans for past few months, especially after the fiasco of IL&FS. They had decided to start loan bookings in the last week of Jan, but again the current problems erupted. I think they are suffering cash crunch. The immediate future looks bleak. If you have friends in DHFL or in any other NBFC, please verify this.

1 Like

yes ground level very bad.I am last person to get disbursement of loan sanctioned in September but received in December(lucky!!)This is Kolkata br.position,I asked sales agent n knew that no more payment to be released in December(very few of previously sanctioned loan disbursed).Regardingvestment he told to wait and see next quarter…he was seeking opportunity to leave dhfl at earliest!

1 Like

This is the list i was forwarded. Look at the size of non-bank borrowings and their ratings. One big crisis is looming if RBI does not step in. Additionally I would have shorted these rating agencies too.

Ideally market should follow the rating on the contrary rating agencies are following market…what a mockery by rating agencies…

2 Likes

I heard there is a conference call Monday morning. Can anyone pass on the details please, if you received the invite.

2 Likes

Why do you think RBI needs to step in? This is not a Lehman like situation requiring a central bank to step in because one default leads to another (a big if that too). All those non bank borrowings are mostly held by MF’s which in turn is held by large investors or corporate treasuries. Similarly with banks, it’s just another NCLT case like Essar or Alok - mostly PSUs are involved in any case so they will most likely be capitalised by the government if there is a problem or merged into SBI! If push comes to shove, it will lead to write offs and tightening of yields once again as ratings are questioned like the ILFS crisis. However, I simply do not feel this is domino effect kind of situation. It would be interesting to see the earnings and performance in the 10 years since Lehman of the various rating agencies such as S&P and Moody’s to get an idea of whether they are likely to face issues.

All this is still a very hypothetical situation as there is no confirmation of any such default or fraud. The status quo as of now is that DHFL has over the next 1 year more assets maturing than liabilities until some fraud is proven.

1 Like

There was no fraud proven in PCJ either. That did not stop its share from losing 90%. Once the perception of a company has taken a dent, it will take years for price to recover even if there is no fraud.

Anyone attended today’s call? No details on how to join the call

I am on the call , its still going on Q&A part.

may get over soon.

1 Like

can you please summarize if possible?

sure,

basically they are denying all the allegations,

they also said along with external CA firm there also will be independent auditor suggested by Bankers who will do audit of things alleged by Cobrapost

they also trying to onboard strategic investor in DHFL by strategic stack sale.

All the projects mentioned by Cobrapost are real slum rehab projects and work are in progress for them.

Total amount for all allegation /wrong doing comes to 23500/- cr and not 31000/- cr.

liquidity situation is comfortable for next 6-9 months.

the shell companies mentioned in cobra post article was not in list that govt prepared/declared in 2017 so they aren’t shell firms.

they engaged with all the lenders.

rating down grade is purely based on the share price going down etc.

3 Likes

Authentic!! Forget growth for the foreseeable future. They might be selling high quailty assets as well. Exited with a loss, but have peace of mind!

The concall was very positive. They gave the full details of the loans. They are willing to show the documents to anyone who wants to visit their office and wants to see them. They have ample liquidity to service the liabilities for next few months. Post Sept 21 they have shown the details of loan books to the banks & mutual funds & they were satisfied with the quality of loan book. I do not think the quality of loan book would have changed in last 1 week. SBI chairman was also on CNBC & he also said that they are satisfied with their lending to DHFL. I may be biased as I am invested in DHFL.

1 Like

is there any way i can listen to the audio since i wasnt able to hear it live.