True, and I think management also mentioned they have already passed on around 60+bps since April. So, while some of these concerns may be valid, they appear bit overblown, and does not justify the kind of price action that is being witnessed in the past few days.

identifying something like this is not practical and not possible.

it is only times like this that test a investor’s patience and conviction in his own research and hard work.

the basic premise on which the fall started has already been addressed by the mgmt and by dsp. rbi and sebi to have agreed to step in if required.

it would be foolish to cast aspersions and doubts on thr mgmt, though i agree that in India nothing is black and white, everything is a shade of grey.

1 Like

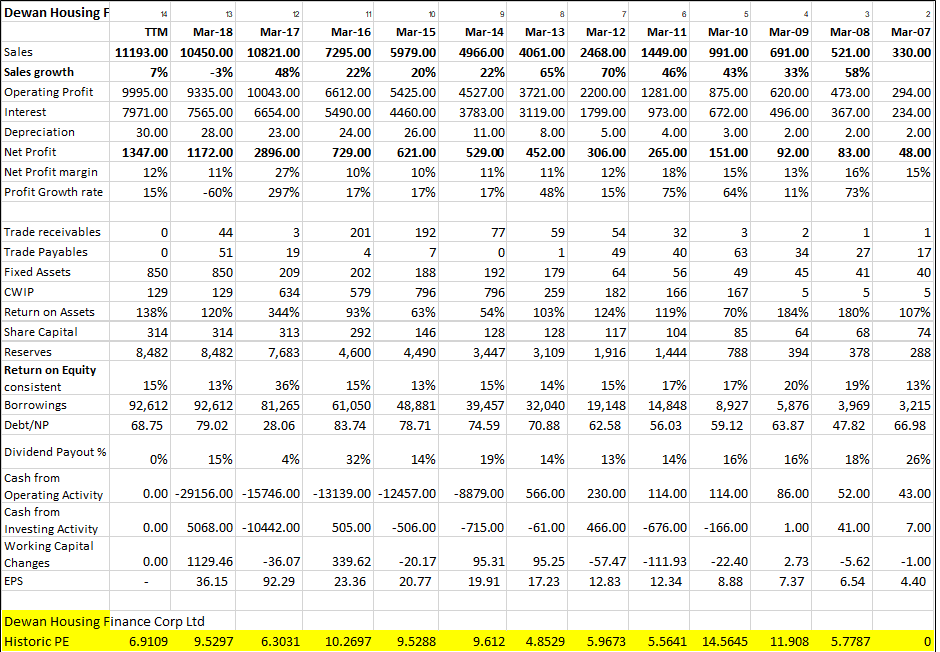

Historically, during last time interest rates were going high, the markets did discount Dewan more than they should have. On the attached below, you’d notice, the P/E (the rate the market thinks profits will keep up, increase or decrease) did go down significantly. However Dewan was able to maintain EPS and the markets did eventually value them at a higher PE.

However when further interest rate increases were capped, Dewan from figures looks like were able to do better by delaying the time the pass those interest rate reductions to its customers.

Bear scenario:

If they can achieve the same going forward - as there are now substantially different market conditions because of housing stock, new regulations.

Case for Bull scenario:

Also during 2012-13 when rates were going down, the markets discount P/e equally of all companies not just Dewan so all things being equally, Dewan might be available at a bargain

3 Likes

Am afraid that’s not the right way either as the market cap reflects the equity while the operating profit in this case being an NBFC is driven mainly by debt, as the leverage is over 10 times. The right things to look for are P/B, growth in book over time, NIM, RoA, RoE, Cost of funds etc.

I suggest you go through this thread.

4 Likes

BNP Paribas bulk deal is irrelevant since they seem to have bought it for their arbitrage fund. An arbitrage fund manager only looks at the difference between the spot and futures price, in order to create a risk-free arbitrage trade by either selling in futures and buying in spot or vice versa.

Regarding RJ, we have to wait for the Q2 shareholding pattern to be published, to check if he is still holding on to his shares.

Disclosure - Holding (10% of my portfolio).

2 Likes

The article added nothing new than we already know. Yes there is liquidity issues and Interest rates are going up.

The question we all need answer for are:

whether Dewan Housing can successfully pass on the interest rates? No reason why not as 99.5% of loan book are floating rate

Whether it will face liquidity issues? My feeling is it will not as it has multiple avenues of funding and AAA rating

Whether it can keep growing at the same rate? Most probably not. But the valuation have been beaten down so much that even at a conservative 10% growth rate, this looks attractive.

Could it handle NPA issues? This management has been in this business for 3 decades and seen many such cycles. Have to trust the management that they can successfully go through this cycle too.

Are there corporate governance issues which is a big red flag? As far as I know, we still do not have a convincing proof that management is not working in investors interest. At least Yes Bank can be called an aggressive bank which is. Risky bank.

It is very ironic that bears are targeting yes bank, Indiabulls Housing and Dewan Housing which are all run by skin in the game promoters who are more likely to work towards the long term good of the company than professional managers.

2 Likes

Hi @SlownSteady

To pass on floating interest rates seamlessly the maturity gap has to match perfectly which is ideal and cannot be achieved.

When advances are on floating rate and the interest rates are rising , you want a large positive gap between the assets and liabilities to be able to benefit from the rise so that a large number of assets can be repriced and a relatively less number of liabilities come in for a similar repricing.

Longer tenured assets or liabilities have a longer time gap between resets and thus it in the event of an adverse interest rate scenario you want to be able assets faster than liabilities.

Below, is the maturity gap of DHFL and one can clearly see that 46% of the most recent (1mth - 7 yrs) assets that it holds have an adverse or negative gap ( Liabilties are more than assets in that time bucket) which is the case with all HFC’s and not just DHFL. This indicates that it may not be able to protect its margins as much as it would like to even tough it has most of its assets are on a floating basis.

An excerpt from RBI

“9.4 The Gap is the difference between Rate Sensitive Assets (RSA) and Rate Sensitive Liabilities (RSL) for each time bucket. The positive Gap indicates that it has more RSAs than RSLs whereas the negative Gap indicates that it has more RSLs than RLAs. The Gap reports indicate whether the institution is in a position to benefit from rising interest rates by having a positive Gap (RSA > RSL) or whether it is in a position to benefit from declining interest rates by a negative Gap (RSL > RSA). The Gap can, therefore, be used as a measure of interest rate sensitivity”

source : https://m.rbi.org.in/Scripts/BS_ViewMasDirections.aspx?id=10568

| LIABILITIES | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1mth | 1mth-2mth | 2mth-3mth | 3mth-6mth | 6mth-1yr | 1yr-3 yrs | 3yr-5yr | 5yr-7 yr | 7yr-10yrs | >10yrs | ROW TOT | |

| Deposits | 10,735 | 29,915 | 66,060 | 137,736 | 223,841 | 472,022 | 74,161 | 5,723 | 13,374 | 381 | 1,033,949 |

| Bank | 249,912 | 36,284 | 79,234 | 154,522 | 310,595 | 1,402,974 | 1,079,513 | 547,532 | 298,859 | 45,468 | 4,204,894 |

| Borrowing | 19,655 | 414,227 | 205,383 | 125,436 | 137,845 | 1,108,250 | 315,614 | 701,059 | 590,486 | 118,270 | 3,736,226 |

| FCL | - | - | - | - | 14,794 | 14,794 | 131,357 | 135,531 | - | - | 296,476 |

| COL TOTAL | 280,302 | 480,426 | 350,677 | 417,694 | 687,075 | 2,998,040 | 1,600,645 | 1,389,845 | 902,719 | 164,119 | 9,271,545 |

| % of ROW TOT | 3% | 5% | 4% | 5% | 7% | 32% | 17% | 15% | 10% | 2% | 100% |

| ASSETS | |||||||||||

| Advance | 170,086 | 45,856 | 46,240 | 141,019 | 291,821 | 1,237,280 | 1,409,463 | 1,065,563 | 965,054 | 3,820,850 | 9,193,232 |

| Investments | 687,908 | - | - | - | 17,285 | - | - | - | 66,526 | 35,931 | 807,650 |

| Assets | - | - | - | - | - | - | - | - | - | - | - |

| COL TOTAL | 857,994 | 45,856 | 46,240 | 141,019 | 309,106 | 1,237,280 | 1,409,463 | 1,065,563 | 1,031,580 | 3,856,781 | 10,000,882 |

| % of ROW TOT | 2% | 0% | 1% | 2% | 3% | 13% | 15% | 12% | 10% | 42% | 100% |

Source : Annual Report 2018

Views welcome , not an expert & learning.

Best

Bheeshma

6 Likes

I agree that they cannot get out of the liquidity issues easily. But being AAA listed and having multiple avenues to raise funds, they could get out of the liquidity issues eventually.

To pass on the increase in interest rates, they do not have to wait too long as a home financier can increase the variable rate interest rate any time. Only fixed rate interest will have a 2 year or 3 year timeframe. As the increase in interest rate will be across board for all home loan companies, the customer will not have much of a choice to shop around. This may aggravate NPA issues as some customers may not b able to afford the increased rates and this could also reduce the pace of growth going forward. But at this price, PB of 1 and PE of 6, all risks look priced in.

Bheeshma

There are few caveats in that assumption

Firstly, Deposits taken from public have a fixed rate so in the times of rising interest DHFL’s cost with respect to interest expenses are fixed whereas what “they charge”/Revenue is likely to go up

Secondly this is not the first time DHFL has witnessed a rate increase. I am attaching their profit and loss since 2005. You will notice during the last interest rate changes they have handled quite well. I am also attached interest rate changes over the period. However bear in mind that market moves 2-3 months in the direction before rbi changes interest rates

Dewan historic figures

Historic interest rates

8 Likes

Hi, would just like to add that rate increases / decreases are part and parcel for a credit business and especially so for a long tenored asset book like a mortgage book - so this per se is not a concern. Imo, in a commoditised market like mortgages, market share is a more critical factor in terms of growth - it is preferable to sacrifice margins to grow, particularly if it allows one to access better customers as the cumulative life time risk reduction is significant, and the collateral itself will be superior. This is imo the main commercial risk. The key prudential risk for mortgages and long tenored asset books is liquidity - it really is not possible to match ALM to 20-30 yr assets beyond a point, so the question becomes the ability of the business to refinance periodically. This is unfortunately v opaque and difficult to make out - and requires deep and constant study of the money and bond markets. The global financial crisis was sparked by the confluence of the commercial and prudential risks in the US mortgage market - rates kept falling while customer quality kept worsening, and the constant need for liquidity led to layers and layers of opaque derivatives to adjust for the rising risk levels and falling return - eventually the underlying assets soured due to rising rates, triggering a wave of defaults, the super structure of derivatives imploded and liquidity froze completely. This was hard to see unless one delved into the structure of US money markets and the exact instruments being traded. In India, we don’t have such complex markets, but we have something equally opaque and incaculable - insider relationships and private information - Indian markets (debt markets) are concentrated and shallow, and moved easily by key market makers so any small signal (rightfully so) gets amplified many times - there’s a large information premium attached to discrepancy in Indian markets. I would guess there is more pain to come.

2 Likes

Do you have conclusive proof that Funds and Investment Managers will remain largely invested or out of DHFL, say half a decade from now?

We do not know that. We should definitely research about a company doing activities that harm shareholder’s value. But it’s useless to speculate on how millions of people will think about an event that may or may not happen.

The best we can do is discuss fundamentals, discuss value and discuss business activities. And understand all of it. Ourselves. Borrowed knowledge hardly lasts.

4 Likes

SEBI now has written to. Mf about dhfl n ibhf.

Raising suspicion.

Make your own view and read this.

" The sources also said that the regulator has advised mutual funds not to roll over their current exposure in these two companies. "

It seems implausible that regulator would give such advise.

3 Likes

Would this help calm the market a little bit …??

Edward,

Thank you for supporting your point of view with data.

An nbfc is never killed by an asset side, it is killed by its liability side.

Santosh Kamath of Franklin templeton Debt management said”MF will lend to NBFC’s but stronger ones” & A’s per him as of today

strong nbfc has following characteristics:

-

Not more than 6 times D/E

-

Above 18% CRAR

-

Strong parentage

-

No corporate governance concerns

-

No ALM mismatch

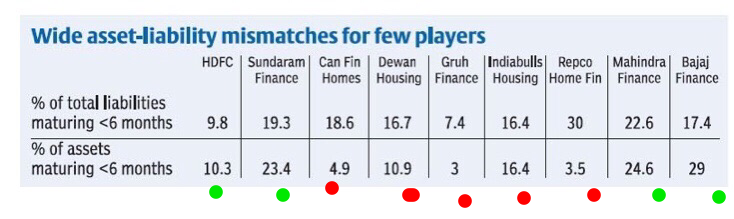

If we look at D/E of all NBFC, we would find DHFL is at top worst quartile. You may argue that it has always been so. It has survived so long. Well that’s correct. Some may argue if tide turns, companies with highest debt relatively would face an issue.

Look at ALM mismatch table, see they are again at worst quartile. I understand if you include their investment + undrawn banklines all is well. Correct but still there may be reasons why good companies have positive ALM mismatch.

- you add promoter perception issues.

Now I am no way suggesting that dhfl is in trouble. This just justifies that if nbfc sector will face pain, company with higher debts may be in more trouble than others.

They have seen 2004 cycle, 2008, 2012 cycle. And grown in all interest rate cycle. There has to be premium for this advantage.

So my bet is they will survive. Just that considering not so great ratios. 7/8 PE (based on your comfort level)sounds good to me. Now if profit will increase, let’s give 8 pe and try to find valuations. 8 pe is way lesser than others and it has included all negatives of company. Any ratio less than that is undervaluing the company and anything more is happy ness.

Two survival conditions

-

They should survive liquidity crisis

-

No fraud comes up

Disclosure: I am invested in dhfl. I am taking a hard look at the mirror now.

18 Likes

NHB permits NBFCs to have upto 16x D/E

Will that help ? As issue is whose going to lend them ?

To be honest it is very difficult to monitor these short term mismatches even if one is alert. What we could do is to select top quality management and trust them to handle these issues effectively. As Rashesh Shah mentioned, these are industry wide issues with mid-term implications. Edelweiss which manages issuance for almost all NCDs has also fallen 40% due to liquidity issues. Market doesn’t trust that they can manage their own debt schedule.

1 Like

Yes i agree , as in their case the ALM is positive for next 12 months , more assets maturing compared to liabilities.

Puneet

Thanks for your analysis

We all are in the same boat as holders

Banks and nbfcs take huge loans/debt

Their efficiency is measured by net profit over debt

Dewan is not great there as well

But let’s say as their annual report says, their non performing assets are low

As it’s a commodity, in theory they can increase the rates on housing loans to above average market rates

What this will do is force some of the debt/mortgage to be redeemed

Very recently they actually wanted to get more debt that could mean either they need liquidity or their model works

Having said that indiabulls and hdfc also are/were in the process of increasing debt via debentures