Added Natco Pharma, Abbott India and Thyrocare over the past few weeks. Increased cash % by booking profits in some counters.

Low oil prices demand buying OMCs but am concerned about buying PSUs in an election year.

Added Natco Pharma, Abbott India and Thyrocare over the past few weeks. Increased cash % by booking profits in some counters.

Low oil prices demand buying OMCs but am concerned about buying PSUs in an election year.

AFAIK, oil plummeted once the world came to know of waivers given to the two largest importers of oil.

Since the waiver is only for a few months (till Mar-Apr 2019?), oil should start rising in a month or two. And then OMCs’ margin will decrease. Shouldn’t this be a stronger reason than elections to not buy OMCs?

Accept that there are more variables here. Lower demand from US, pace of electric vehicle adoption etc. I was just getting interested in OMCs as nobody talks about them now due to low oil prices. Dividend is key attraction.

Btw, OMCs are slowly expanding LPG network which will hit almost 100% Indian households soon.

Still, pricing is subject to the pressure from Govts.

Hi ,

You have very good set of Companies. Though lot of companies like Avenue Supermart , Asian Paints , Britannia , HUL , Bajaj Finance , HDFC bank are expensive . These are great portfolio business which may go through price or time correction and these should be bought in SIP over 1-2 Years.

Your recent additions are also good. Thyrocare is a good business with great return ratios and a very big market to address and available at good price. Abbott is also a good pick. Portfolio looks well diversified. Some reduction in Financials can be done.

My suggestion would be to keep your stocks limited to 14-15 and give it some time rather than churning it fast. Re-invest the dividends into the same names and let your money compound for long.

I read your interest in OMCs due to low crude prices. You can also look at IGL or MGL. I have seen huge demand for CNG in Delhi. It is cheap than the Petrol and it is still unclear whether EV can disrupt them or not. Households are getting PNG Connections for Gas with latest 10th round of CGD Bidding. Govt plans to expand natural gas share in its energy mix to 15% by 2022 from current 6%. I personally like Business of IGL/MGL where they pass on the increase in price of raw material to the end customer. Also it is not easy to disrupt their business with the kind of infrastructure required and they have Moat in their respective area of operation.

Regards

True for now.

But the issue of pricing will come out sooner or later. I have to admit I lack the courage in this sector. Unless I have a high margin of safety, will not enter these companies.

Definitely , they do not offer any margin of safety at CMP. Looks expensive but i think people tend to ignore the entire sector due to fear of regulation. IGL has given absolute returns of 200% in last 4 Years , 400% in last 5 Years and 1200% in last 10 Years. Return on Capital Employed are above 30% over all these years which may be due to the negative working capital. Though the past results does not give any indication for future but my thesis was on the ongoing developments in the energy market.

Though it is good to ignore if one does not have the confidence in the sector or is very vary of the government regulation and controlling of pricing.

Here is my current stocks portfolio:

| Stocks | Portfolio Weight | Avg Price | Total Gain |

|---|---|---|---|

| Bajaj Finance | 17.44% | 1873.6 | 114.49% |

| HDFC Bank | 14.38% | 1040.41 | 17.38% |

| Reliance | 10.64% | 1150.18 | 19.35% |

| Avenue Supermarts | 8.7% | 549.8 | 240.35% |

| PSP Projects | 8.5% | 411.38 | 33.34% |

| Abbott India | 6.78% | 7503.98 | 45.73% |

| Ashok Leyland | 6.66% | 83.66 | (14.36%) |

| Asian Paints | 4.92% | 1230.77 | 43.46% |

| Britannia Ind. | 4.92% | 2683.4 | 18.41% |

| Nestle | 4.45% | 10338.8 | 38.78% |

| HDFC AMC | 4.22% | 1818.5 | 49.61% |

| Pidilite | 3.37% | 1134.73 | 19.89% |

| HUL | 3.21% | 1594.2 | 29.96% |

| Zee Learn | 1.82% | 16.36 | (10.44%) |

| Overall Portfolio | 39.71% |

Return comparison with Sensex:

• 1year: 23.09% vs 10.98% of Sensex

• 3year: 24.92% vs 40.21% of Sensex

In the hindsight, I have done well when I reduced portfolio churn and increased weightage to the steady compounders.

Financial Services space only HDFC Bank and Bajaj Finance.

Exited PEL, Edelweiss and Avanti Feeds.

New Buys since last portfolio update: Abbott India, Nestle, HDFC AMC, Pidilite and Zee Learn.

Strategy:

Have less confidence in Zee Learn, will wait before adding more.

Watchlist: Thomas Cook India, Powergrid, Nalco, HDFC Life, GMM Pfaudler.

In addition to this, started an SIP into NIFTY 50 and NIFTY NEXT 50 ETFs. Also increased cash holding.

Happy to buy more if the market tanks tomorrow.

Excellent Portfolio. But your recent additions such as Ashok Leyland & Zee Learn does not look good. what makes you bet on these 2?

Hi Dev,

The portfolio is excellent the quality of the companies is top notch this is a typical coffee can type portfolio no one can dispute that.

But the question is, from this point forward, what will this portfolio deliver.

My expectations are that this portfolio will deliver slightly better returns than Nifty 50 itself.

If Nifty Falls 10% this portfolio will fall five.

If Nifty gains 10% is portfolio will gain 15.

If this is what u aim for then you are the right spot.

Hi

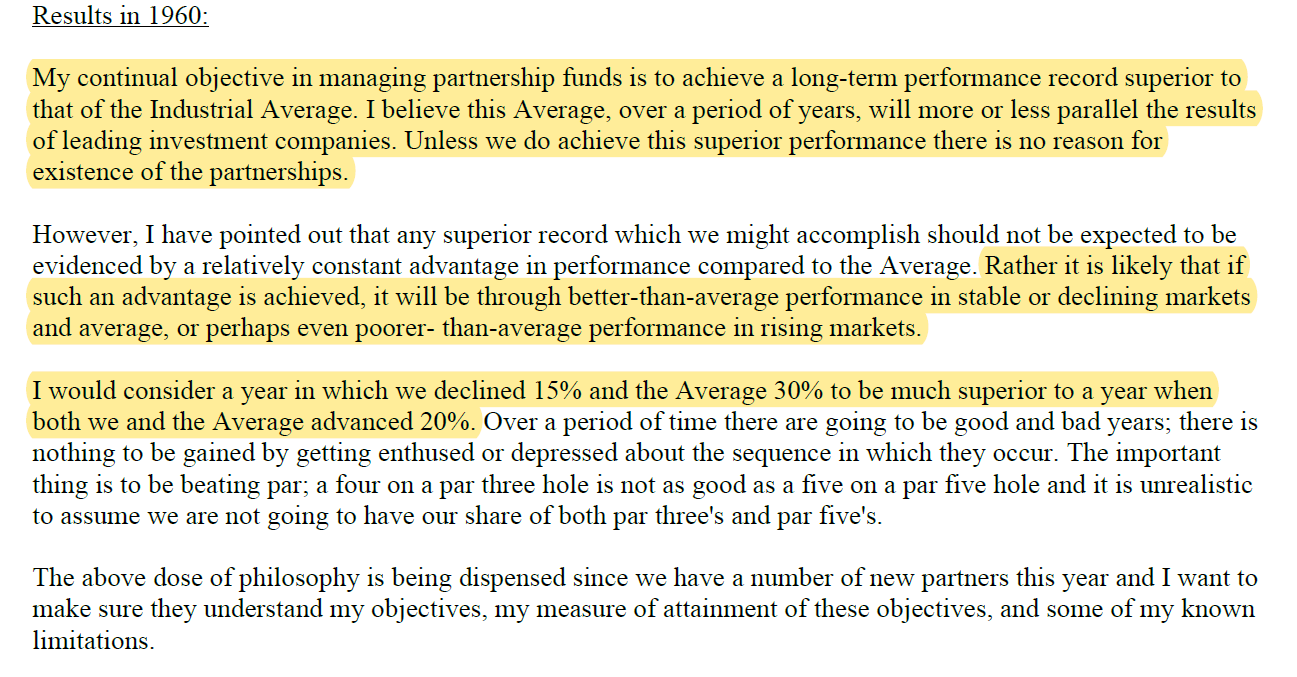

This reminds me of exactly what Mr Buffett has written multiple times. It is something which I think @devarajank would be emulating in his portfolio construction. Pasting what the 1960 letter says.

I have a substantial overlap with this portfolio in my large cap one.

Regards

@deevee: Thanks for sharing the 1960 letter. My first priority is to not lose money, second is grow it slightly better than the index. Rest all, I believe, is pure dumb luck.

@jamit05: Idea is to build a core portfolio that beats index and offers downside protection. Plus I am researching to create a satellite portfolio. If I am not able to find good opportunities, I buy the index ETFs (75:25 -> Nifty50:NiftyNext50)

Rationale for Ashok Leyland:

Industry:

Auto sector is at a cyclical low or may be close to low. DOnt know when it will recover. There are theories that the market is near saturated for passenger cars and two wheelers. Not an expert to judge it. May be a maruti or tvs be value buys. But I am not sure about a recovery soon.

On the other hand, Commercial Vehicles is bound to do well when the economy picks up. Whether Uber/Ola kills passenger cars or not, we will have Buses (diesel, CNG, Electric) and heavy and light trucks.

Competitors:

Tata Motors is facing issues in Passenger vehicles segment and is in not a position to offer deep discounts to beat Leyland. Anyways, Leyland is not in the low price game and they have actually increased their market share in previous downturns.

Negatives:

Net-Net I am willing to ignore the negatives and go for it.

Zee Learn

Industry:

If you are a parent and have searched a good playschool/school for your kid, you will know how recession proof this industry is. People are willing to pay for quality.

Company:

With the Kidzee brand and others like Mount Litera, Zee Learn is well known in the market. They have adopted more of franchisee model which will drive further expansion. Company has been posting good results too.

Concerns

I believe the organized players will benefit from Govt regulations if any. Zee Learn is a drop in the ocean for Zee group. Dont think they will exit, even if they do it shouldnt be a big issue.

Anyways, watching the company performance to add further.

Can you please share your reasons for PEL exit. That’s my largest pile in PF (due to appreciation not original allocation).

@anandrkris: At one point in time PEL was my largest holding. I also had a good position in Edelweiss. I gradually exited both thanks to the NBFC crisis, which I believe will lead to the bigger and more efficient players like Bajaj Finance (and HDFC Bank) getting bigger.

This made me switch to Bajaj Finance and HDFC Bank which are my only picks in Banks/NBFC space.

Specific to PEL, I think Mr. Piramal underestimated the liquidity crunch in the market and one could see the gradual decline of optimism in his interviews/statements.

As of now, I am good with Bajaj Finance and HDFC Bank.

Thanks, I share same concerns but hoping Ajay Piramal will figure a way out. ![]()

Hello,

Iam studying IGL for investing. Could you please share your current views on the overall gas sector and the company given COVID impact and also increase of belief in EV segment.

Hii , Sorry for the late response.

Regarding the Gas Sector , it is a priority sector for Government considering the announcement for Piped Gas for households. It is a Big Market and very difficult for new companies to enter as it required huge infrastructure. My thesis is still intact for IGL which has some sort of pricing power and is available at good valuations with Good Dividend Yield. Regarding disruptions due to EV , definitely it is a challenge but still not any meaningful impact has been seen due to EVs. Moreover the Piped Gas for Household is a big Consumption Market which can mitigate the impact of EV.

Definitely the sector has Government Interferences and Regulations (Latest Being Price cut for GSPL Pipeline by Regulator) and thus these companies will find it harder to get valued richly. Disc: I hold IGL