Read his tweets for a possible hint

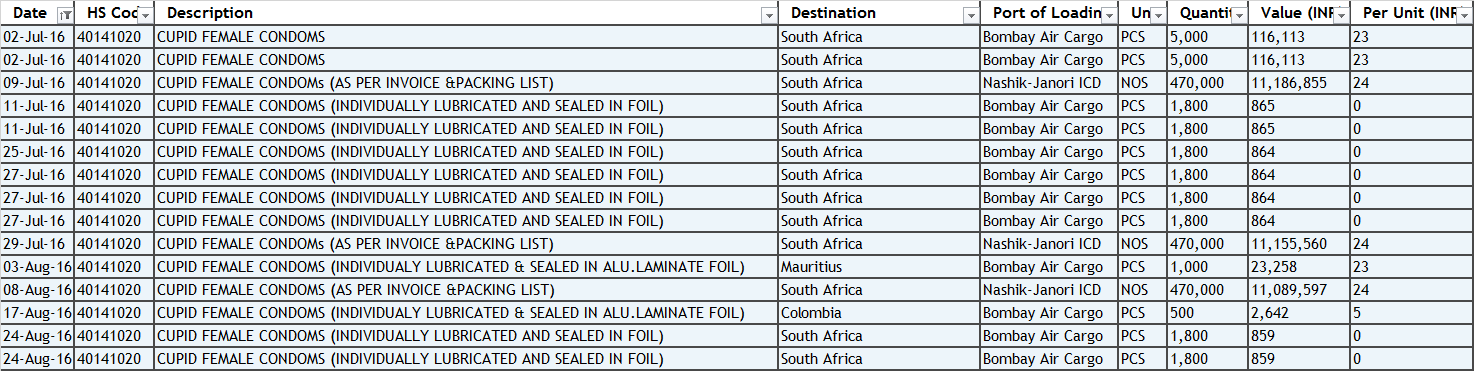

https://www.zauba.com/export-female-condom-hs-code.html this link may be useful to the investors of CUPID LTD. to track the export data of FC.

HLL gets its first bulk export order for female condoms(1.3 million pieces of female condoms to Gambia and Burkina Faso in Africa and Dominican Republic in Caribbean Islands). Any ideas how we can figure out at what price point they are executing this order?

Other point to note is HLL has a capacity of 25 million female condoms per year.

Disc: Invested in Cupid

The bulk orders emanating for the sub-Saharan region has always been a priority issue for Cupid.

In my understanding., Not bagging this order will surely be a setback for Cupid., as bagging & execution of this order gives HLL a boost to bid & bag other orders too.

& Cupid was in urgent need of a bulk order of FC.

Discl : Invested in Cupid

2 Likes

FC orders from Africa starting to flow seems to be good news.

The market size for FC is quite big in contrast to the order size awarded to HLL. The major issue was the slowdown in FC orders from African markets due to lack of funds.

Most of the African health department reports mention procuring FC as part of their 16-17 budget / strategy. However, that has not translated to orders yet.

This, I construct as a positive news and could be just a matter of time before orders start flowing.

Disclosure: Invested since 2 years

Any idea, which product is better - HLL one or Cupid in terms of quality and price?

Dear Vishal,

I had done some study online regarding the acceptability of FC & also comparative analysis vis-va-vis Cupid’s competitors.

Here’s the complete report providing acceptability & rejection rates of major FC products in the market.

Cupid, HLL & FHC are almost at par in all major qualitative, functional & other parameters.

Final Report.pdf (1.4 MB)

2 Likes

Thanks Mukesh, this is a great report.

1 Like

What is the market share of Cupid in B2B segment? I understand that FHC is big player and also its cost is too high compare to Cupid. If Cupid has cost advantage, can we expect it to eat into market share of FHC? And how big that would be?

Disclosure - Recently entered. 3.3% of my holding - Learning more about company before increasing the allocation

Just read one of the Transcript whereby Mr Garg told that the Water Based Lubricant will be introduced commercially by Q2FY17 and also that it would be one of the Growth trigger for the company as reported in its Annual Report

Can someone throw light on the Margins offered in that product. Is that product margin accretive for the company ?

Disc : Initiated small position and wish to add more gradually

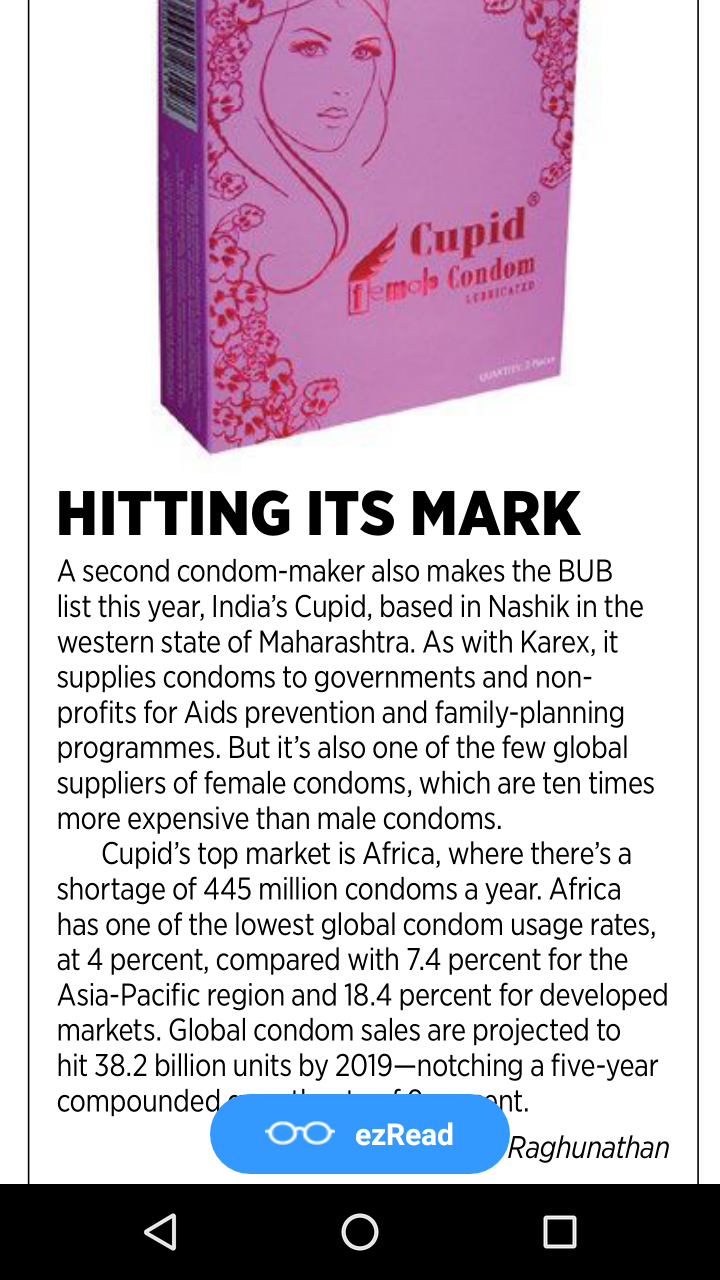

Good article on Karex, world’s largest condom manufacturer, in forbes india september issue. Karex of malaysia entered best under a billion club this year. The company makes 5bn condoms and has 15% market share. They earn 3 cents per piece. They do contract manufacturing for durex and are trying to develop own brands. They acquired a UK based company recently. Plan to increase capacity to 7bn by 2017.

Also…cupid found a place in the list

With HLL bagging a huge order for FC’s do you think a correction is up on the cards? What are the next growth triggers for Cupid? I was under the assumption that only Cupid and FHC had UNFPA approvals. From this link - http://fcmi.org/fcmi-product-briefs/who/unfpa-prequalified-fcs.html now we 4 players with HLL in the list as well.

There won’t be a correction just because HLL has bagged an order. The market size for FC is huge and there is room for more players to operate. What HLL has bagged is a small pie and a drop in an ocean.

Growth trigger: With the budgets now decided and into action, we will see a spate of orders for FCs and hopefully one of these will translate into a huge order for Cupid.

1 Like

Isn’t this just another day in free market economics?

When a few entities make outsize profits in a particular sector, other entities enter the sector and eventually the profitability declines to a mean level where entry and exit of entities is more or less equal. The entry of HLL and other global condom makers in this segment could be the beginning of such a process.

I am just playing the devil’s advocate, so don’t kill the messenger.

3 Likes

CUPID-BOB-IC (1).pdf (723.8 KB)

Cupid Ltd Initiating Coverage Research Report By BOB Capital Markets

Thanks @rinkupranjan for the link. Really valuable

Q2 numbers look pretty weak. I tried to match Q1 no by assuming 70% of total revenue contributed to SA and got Rs 10.8 Cr compared to actual Rs 11.15 Cr which is pretty accurate.For Q2, in 2 months passed, it is hardly Rs 3.36 Cr

It is old report ( August - 2015 )

The Mgt. has indicated for a 15-20% growth for the year. So far it has walked the talk. Perhaps it may be wiser to wait for Q2 results, which should logically be good.

5 Likes

@RajeevJ Agree, even if results are not good for this quarter, i wont be surprised, not expecting a uniformity and consistency in order book flow and that still remains a risk in B2G type orders . Keeping fingers crossed. Any idea if they supplied jelly last quarter or from when they will start dispatching lubricant jelly and any guidance on that give to get a sense of calculations?

Disc : Invested below 300 recently