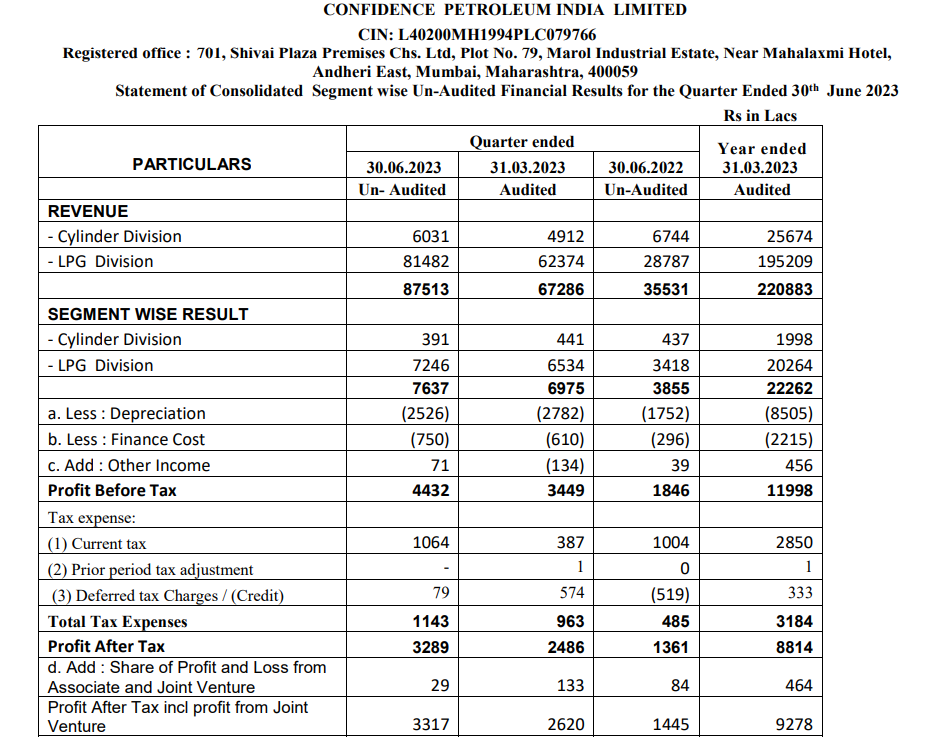

Excellent Results .

Profit Jump from 14 cr to 33 cr (135% growth) YOY

5 Likes

I was doing a quick review of this company for the first time.

For the past 5 years, promoter holding was on rice from below 50% in March 2017 (screener data) to 61% now. However most recent quarter share holding went down by 0.13%. can anyone explain why promoters reduced stake? Will it be a continuing trend ?

Latest interview

1 Like

Confidence petroleum just announced the appoint of ''Go India " as investors relation advisors. This makes me hopeful of the Co starting concalls which would definitely a positive for the Co. ![]()

3 Likes

Hello Abhi

Congrats on the multibgger and bigger congrats for holding this.

Could you describe your investment thesis when you bought ? Management was not giving any guidance at that time. How could make your earning estimate etc.

Did you buy after COVID ?

Did you scale up your position after initial buy and at recent levels of 70rs 90 rs ?

Just asking to learn from your experiences.

Thank you

Praveen

1 Like

Hi Praveen,

I know I will be getting a lot of flak for this as this is almost a pseudo rule breaking of this forum :D.

I hardly listen, read or pay any attention to what management has to say on growth potential of any company. It’s common sense in my view. No management on the earth will say in next 3 or 5 years, my company’s sales will degrow or I am going out of the market. ![]() , So to be very frank, I don’t give any value to what management has to say on the growth potential. Furthermore, how many companies we have in India especially under mid or small cap categories where management has delivered on their guidance. Most of the companies don’t even know what will happen to their sales in next 1 year, leave alone giving guidance to the market for next 3 years.

, So to be very frank, I don’t give any value to what management has to say on the growth potential. Furthermore, how many companies we have in India especially under mid or small cap categories where management has delivered on their guidance. Most of the companies don’t even know what will happen to their sales in next 1 year, leave alone giving guidance to the market for next 3 years.

Having said this, I value company based on today’s standing and what they have delivered in past. I normally use DCF valuation, EVA based valuation and reverse DCF and lot of other things in addition such as their past reinvestment rates, ROIC, SSGR, cash flow ratios blah blah…![]() . I do all these valuation by reducing their historical performance by at least 75% i.e. they will at least achieve 75% of what they did in last 5-10 years. I also reduce all return ratios to bare minimum level of inflation rate in long term (>7-10 years) as mean reversion will kick in.

. I do all these valuation by reducing their historical performance by at least 75% i.e. they will at least achieve 75% of what they did in last 5-10 years. I also reduce all return ratios to bare minimum level of inflation rate in long term (>7-10 years) as mean reversion will kick in.

Ultimately in the FA, Reverse DCF has to make absolute sense to me. In FA, people often ignore the most basic thing which is available to them - stock price. It’s the most wonderful weapon while evaluating the company in my view. It contains all the information within. All expectations of the earning growth, degrowth, companies expansion plans in next 5 years, management quality, change in management, everything is built into the price. In today’s day and age, in my view, nobody has the advantage of having extra information which no one else knows. Implied performance based on reverse DCF has to be considerably lower than historical average for me to think about the company.

Once that’s done, I evaluate technical charts - mainly stage investing and some of the screeners I built over the years. Stock has to be in early or mid-stage 2. I try to avoid stage 3 companies and never invest in stage 4, no matter how good the company is in terms of fundamentals.

Once all my criteria and checklists are done, then I spend one or two days reading about the management (not their guidance), any corporate jugglery they are involved in etc. (Valuepickr is a great resource for that). Once that’s tick-marked, I take a position and that’s it ![]()

8 Likes

Yes, I bought around that time when there was a lifetime flash sale in the market ![]()

Nope, I never averaged up or down after my initial buy.

1 Like