There has been recent purchases also from promoter group.

Thanks,

Deb

Hi,

Godrej industries is going for NCDs worth of 750 crore.

Anyone having idea why they are raising 750 crore in this way ?As I think they have good cash reserves l,which they are also using now to buy shares.

Thanks,

Deb

Hi.

Completely agree about the undervalue story of GIL.

Being a group holding company and family trusts holding most of the shares, it can generate value when one family wants to control the whole of it.

The difference of opinion among the different family groups about the land holdings in Mumbai can be a precursor to that.

In any case, its current P/BV of 1.2 is deeply undervalued considering its holding in Godrej Properties, GCPL, GAVL, etc.

Hi,

I have one doubt,

The new Housing Loan unit will under godrej industries directly or Godrej properties?

Thanks,

Deb

The firm is currently funding its loan book from capital infused by parent Godrej Industries.

Hi,

Godrej industries granted to start financial business.

Thanks,

Deb

Holdco discount is now at 68.5%, and it has been calculated only on the basis of market cap of GCPL, GPL & GAVL, without taking any value of Godrej Chemicals and Housing Finance.

Nice past discussion here on Godrej Industries. I was looking at this company and put together my thoughts in a blog post, sharing it with the broader group in case you find something of value. I have tried to compute the discount. over the past 10 years which can be useful for people on this thread.

[Godrej Industries — Business Class Seats at Economy Price]

Godrej is a well-known brand. The group has many businesses, and it’s important to highlight what all come under the ‘Godrej Industries Ltd’ (or GIL) name. First, a disclaimer - when people hear about Godrej, they always think about almirahs, locks, furniture (Godrej Interio) and appliances like refrigerators and washing machines. These businesses are not part of GIL. They are in a separate company which is privately held.

GIL is a holding company (more on it later) that has stakes in other companies of the Godrej group.

Godrej Consumer Products is a company that owns many of well known FMCG brands that we use. The snapshot below shows some of the top products. This is an excellent company with a strong presence in markets outside India and a DNA of constant innovation through new products. It’s also part of the smallcase portfolio as a momentum pick.

Godrej Properties is a real estate developer with properties in all major cities of India. If you have ever done house hunting – you would have indeed come across names of some of the Godrej properties in your city. The company has a good brand name as a reliable developer with properties of premium and low-cost/affordable category.

Godrej Agrovet is one of the new ventures that are involved in commodity/farmer related products - including palm oil, dairy, poultry, animal feeds, crop protection and more.

The great thing is that the three businesses above are mature and listed on stock markets individually. Apart from this, Godrej also has other businesses in chemicals, finance and other domains with 100% ownership – but they are relatively small. GIL, in essence, is a holding company – that holds ownership in different companies.

What are holding companies?

A holding company’s primary business is holding stakes in the shares of other companies without essentially producing goods or services. You must have heard of Warren Buffet’s Berkshire Hathaway and Masayoshi Son’s SoftBank - these are holding companies. Similarly, many holding companies have been created in the Indian stock market over the years - some examples can be seen below. Godrej Industries is one such holding company.

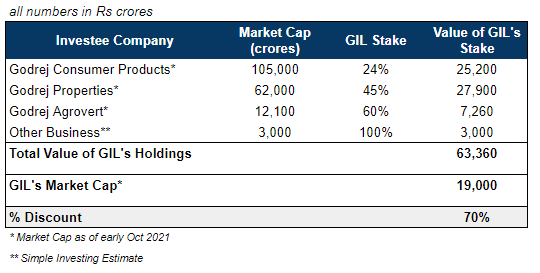

My central argument is that GIL is undervalued. Let’s go through the arguments why. Calculating the value of GIL should be fairly straightforward - take the valuation of the investee companies, multiply by % stake held by GIL and add them all together. In the table below, we did this exercise and realised that in an ideal world the value of GIL should be around Rs 64,000 crores. While a holding company always has some discounts because of different reasons (discussed below), we would have expected the traded value of GIL to be close to Rs 50,000 crores.

However, you will be surprised to know that the stock trades at 19,000 crores only — a whopping 70% discount to its value or in other words, the “valuation ratio” (GIL’s market cap/holding companies value), is just 30%. This is why GIL is a way to get business class seats at an economy price. The great thing is that I also like the underlying businesses. We even have Godrej Consumer in the smallcase portfolio as a momentum pick.

This 30% valuation ratio is a compelling enough reason to buy the stock, but we will briefly dig deeper.

There are legit reasons for a holding company to trade at a discount. The top ones being double taxation, conglomerate discount, presence of cash guzzling businesses that require capital and trustworthiness of the management. Some of these reasons are applicable for GIL, and some are not - I will spare you the details. The important point is that I don’t expect GIL to rise 3x till the discount becomes zero.

Some discounts will always be there, and looking at how this discount has trended over time will give us some clues. GIL’s valuation ratio has been around 60%, whereas the current ratio of 30% is half of that. So the discount is wide even when considering recent history.

One of the reasons why the valuation ratio has decreased is because GIL entered into the retail business through Godrej Natures Basket — a gourmet retail chain selling high-end grocery items. This became a cash guzzling business that did not become successful. However, now the company has sold off that business and this should help improve the valuation ratio.

Last year even the owners of GIL — the Godrej — felt that the stock was super cheap and bought some shares in the market to increase their stake. This serves as a vote of confidence that even the company owners find the stock to be cheap.

The key risk is if we see the value of the underlying holding companies decline too much — or if GIL starts investing in some business that becomes a money guzzler.

GIL first entered Simple Investing’s portfolio early last year and has given 2X returns (performing slightly better than the market). We like the underlying holding companies and the discount that investing via GIL offers.

Hi Board Members,

Anyone tracking this stock. The recent quarterly results seem to be good on consolidated terms.ROE for full year has jumped to 13.54 from last year of 5.85.EPS now stands at 29.PBIT margins are also improving.Overall good results except the debt levels which is because of the godrej Capital financing business.But stock price has not apricated as per the results.PFA for teh Qauterly results.

00206B47B51A230519142957 (bseindia.com)

What am I missing what market already knows? Please comment.

Thanks,

Debadutta Das

As per the video, Macquarie believes that even if the promoters don’t go for voluntary delisting, the discount at which the holding companies trade should get reduced.

How do you view Godrej Industries now @nav_1996 & @ranvir ? Brought to my notice due to upper circuit on Friday

These are slow growers. Best bought cheap and ignored at upper circuits. 400 is what I would be happy with and not buy beyond 500. As this is holding company if market keeps reducing holdco discount it can keep rallying more with momentum but I don’t understand momentum.

Just looking at it over last few weeks.

Forget the capital investments, holdco investments(as they will not be sold) and looking at core chemical space it looks set for rebound.

Any trigger you have identified

The areas where it produces specially surfactants and fatty alcohol and acids is in low demand and prices are expected to be low this year.

I think all holdocos are running up. Tata sons effect. It happens in bull markets.

These are tactical plays. 2007-8 peak was 400+. it came to 600+ in 2018 bull market and at 800+ in 2024 bull market.

Any slow compounder or largecap MF could have beaten above returns in both phases with lot less volatility and certainity.