@jitenp Jitenbhai any ideal about Cement companies …where they stand in cycle at presently? Should it be better to invest or wait. Q2 was worst based on input cost rise and growth in demand (monsoon) for cement company

Hello jiten bhai what are your views on companies making ductile iron pipes from iron and steel and basmati rice exporters

This should answer your question, as to what I think on cement companies.

3 Likes

Some basmati export players have really been beaten down. Have invested in one. Risk-reward ratio is in favor. One must keep a mid to long-term view, though.

2 Likes

#China trade figures: imports of refined base metals shrug off #TradeWar sentiment - copper, #zinc and #nickel up compared to last year and the country on track to be a net importer of #lead for 2nd year running. Refined #copper imports rose by +20% in first 10mths of the year…

Copper will be in bull run and India needs lot ofcopper for its growth if its want to build scale in Infrastructure and key market in ev.

2 Likes

Have an exposure to LT foods, hoping cash flow improvement in 2019 once europe business is ebit positive. Though margins are lesser than KRBL, valuations have come down a bit far.

2 Likes

@jitenp - Hope you are well! Not sure if you had a chance to check on Citi report mentioned in below news item. Would be very useful to know your thoughts on steel cycle

1 Like

Hello Jiten Sir… Any views on the Shipping Companies… Been on a long downtrend… Any views…

1 Like

Export growth plunges due to high base effect

As said before, I am in wait and watch mode currently. Had exited all but one position in steel sometime back.

1 Like

Check VLCC rates & Dry Bulk rates you will get idea what is happening

2 Likes

@jitenp Sir How about the Paper Industry? Is it at the Peak now and shouldn’t be touched or there is still steam left for fresh entry at cmp?

2 Likes

How does the telecom cycle look?the sector seems to be heavily beaten down.Now that the sector has consolidated with just 3 main players all with sound standing eventhough at alarming debt levels.with jio’s aggressive marketing the pain in the sector maynot be over,but is it time to look into the sector. Secondly ,the recent idea of telecom players like idea and airtel bringing in validity recharges are expected to increase arpu from next quarter itself.

Disc: not invested

2 Likes

An article in business standard about circular economy. India’s current positioning in circular economy. Circular economy will have defining impact on metal sector especially steel and aluminium.

circular economy.pdf (1.1 MB)

1 Like

My article in Economic Times, a couple of days back.

9 Likes

1 Like

Here comes the capacity for Paper in India. At least few years away and with other uncertainties of the project going through in a different political regime.

No investment in the paper sector

Caustic soda price has gone up again above 41 + . lets see how much it sustains

1 Like

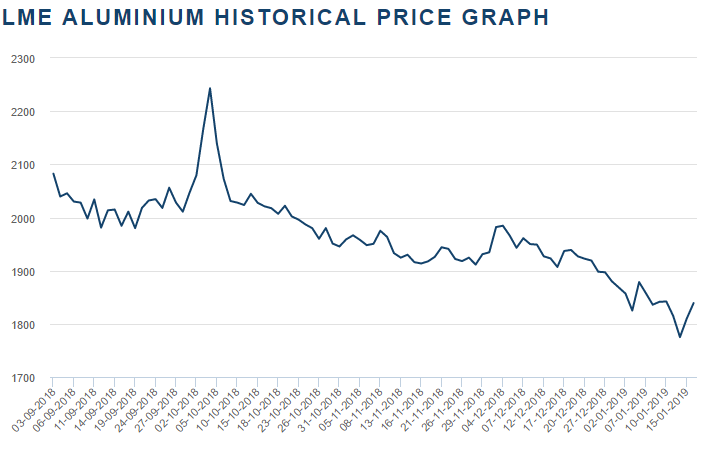

Aluminium prices have corrected by over 20% from recent peak.Which are the aluminium consumer companies that are expected to benefit from it. I could not figure out a company which uses aluminium as key raw material…Thanks in advance

1 Like

Consumer durables … Pressure cookers …Though I am not sure about the time lag when the margins will show less input costa.

Regards

Ps…invst in ttk prestige

2 Likes