So assuming ur projections are more conservative than mine…let’s say for arguments sake we work with a figure of 80 crore PAT in 5 years…this is a non secular stock and hence an exit multiple of 15 should be fair,.

Hence we land at 1200 crore market cap in 5 years…

So that’s like a doubler in 5 years or a 14% cagr

Is there any meaningful upside then.

Also we seem to be working with a Blue sky scenario…

Not sure if this investment is as simple and lucrative

When I first posted on Chembond I did see a sufficient margin of safety and from thereon the idea has always been to focus on business.

Generally I don’t like discussing valuations since they are very subjective assessments and if you see most of my estimates in terms of margins are derived from broader industry averages. Through my posts I have tried to understand the business and also to put across how I visualize it. As for entry/exit multiples I think it is very difficult to make any assumptions and it is more defined by FCF generation/RoE/moat/longevity and a lot of other things.

As I said I dont expect the business growth\performance to be linear and ofcourse there is always a chance of some business falling apart and it does make sense to track the evolution.

Finally whether a business makes sense at these valuations is again a very subjective assessment and the intention of posts was never to suggest what are right valuations but an understanding of business can help to take a call when the valuations are right (subjectively) and if someone likes it.

Discl.: Chembond forms more than 5% of my portfolio. My views are biased. No transactions in last one month.

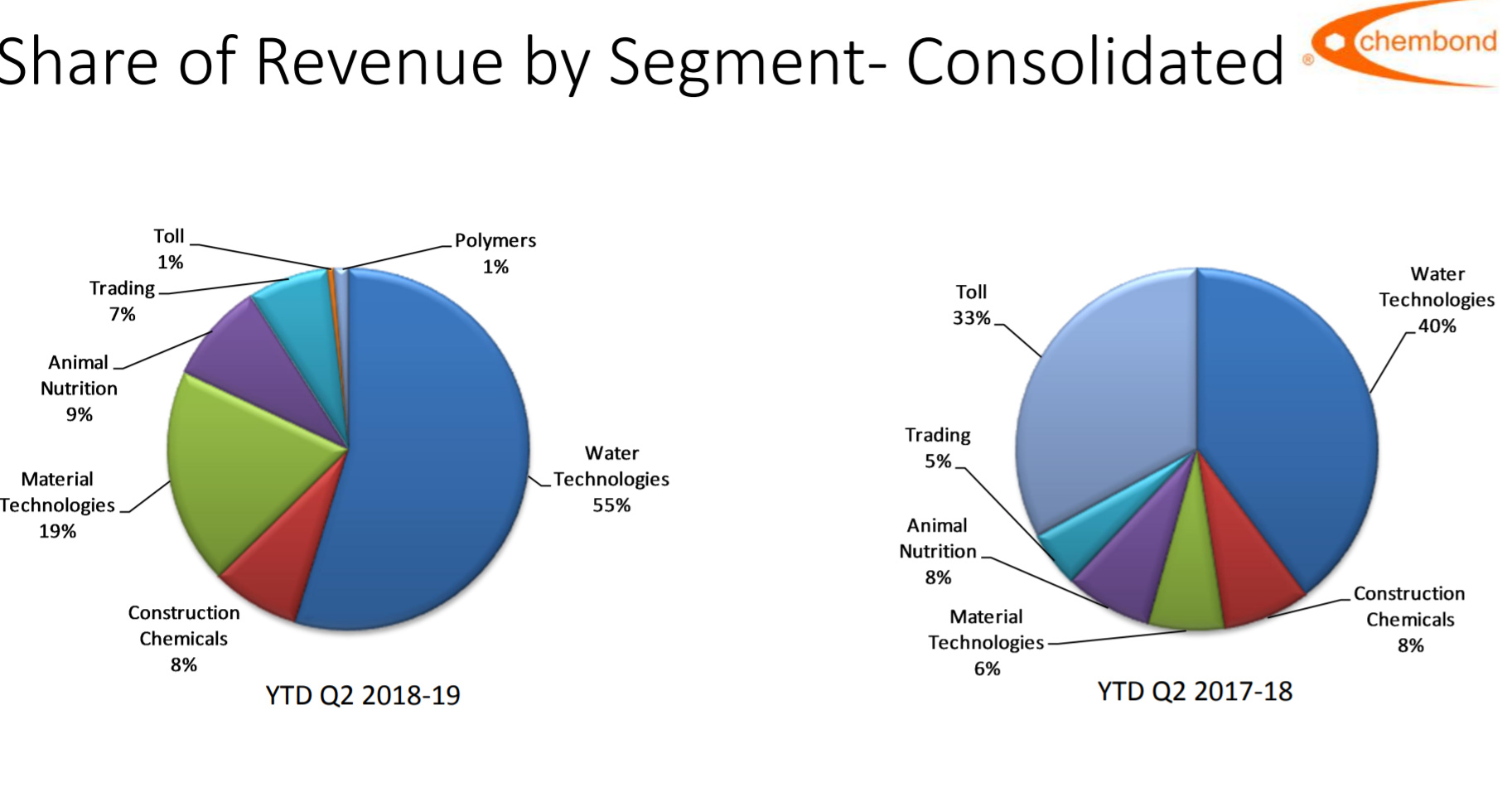

I think my note has been misinterpreted. Sir, the management said that 30-40% of whatever they do sales in the water segment, is done to the public sector for which they can’t pass on the increased RM costs. The management failed to mention the proportion of sales of water segment to the total sales.

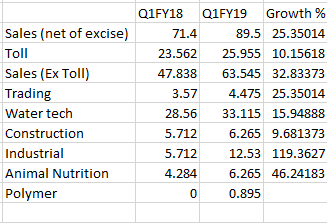

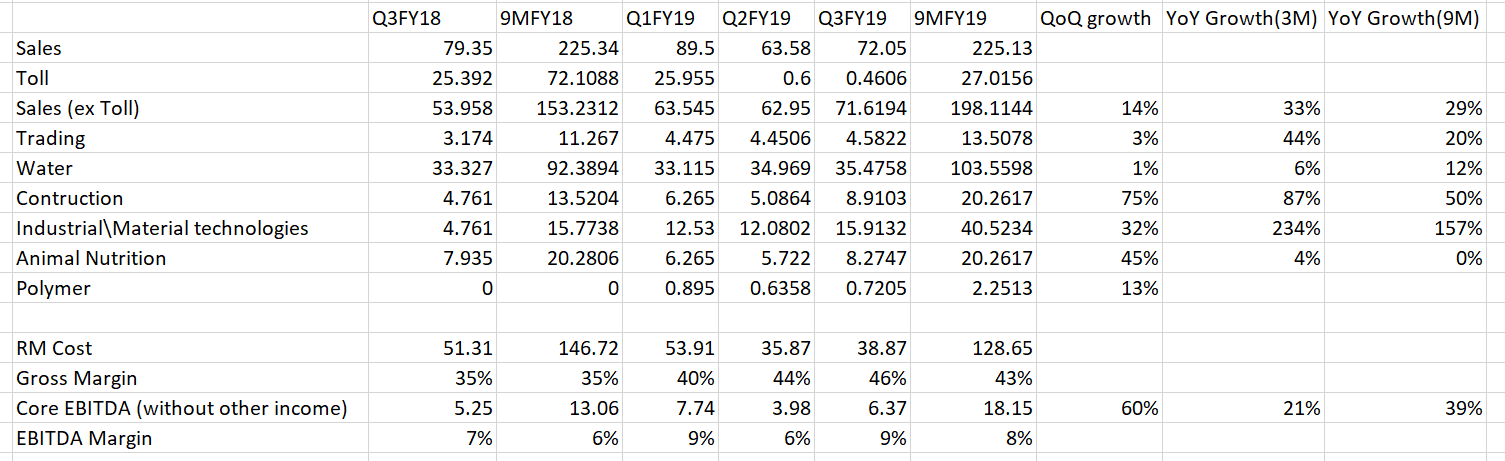

a) Growth in Industrial is driven by PSPL acquisition. PSPL Consolidated sales for FY17 were 28.01 cr. So growth in industrial ex PSPL is muted. Industrial Segment will show further growth from next quarter due to toll going away and company starting to supply in this segment.

b) Animal Nutrition is growing at a very healthy pace. Since Animal nutrition is seasonal it makes much more sense to look YoY instead of QoQ.

c) Polymer division has started showing up in sales numbers.

Just curious about trading (division) and what it comprises.

As a R& D firm, is this more to do with distribution within subsidiaries?

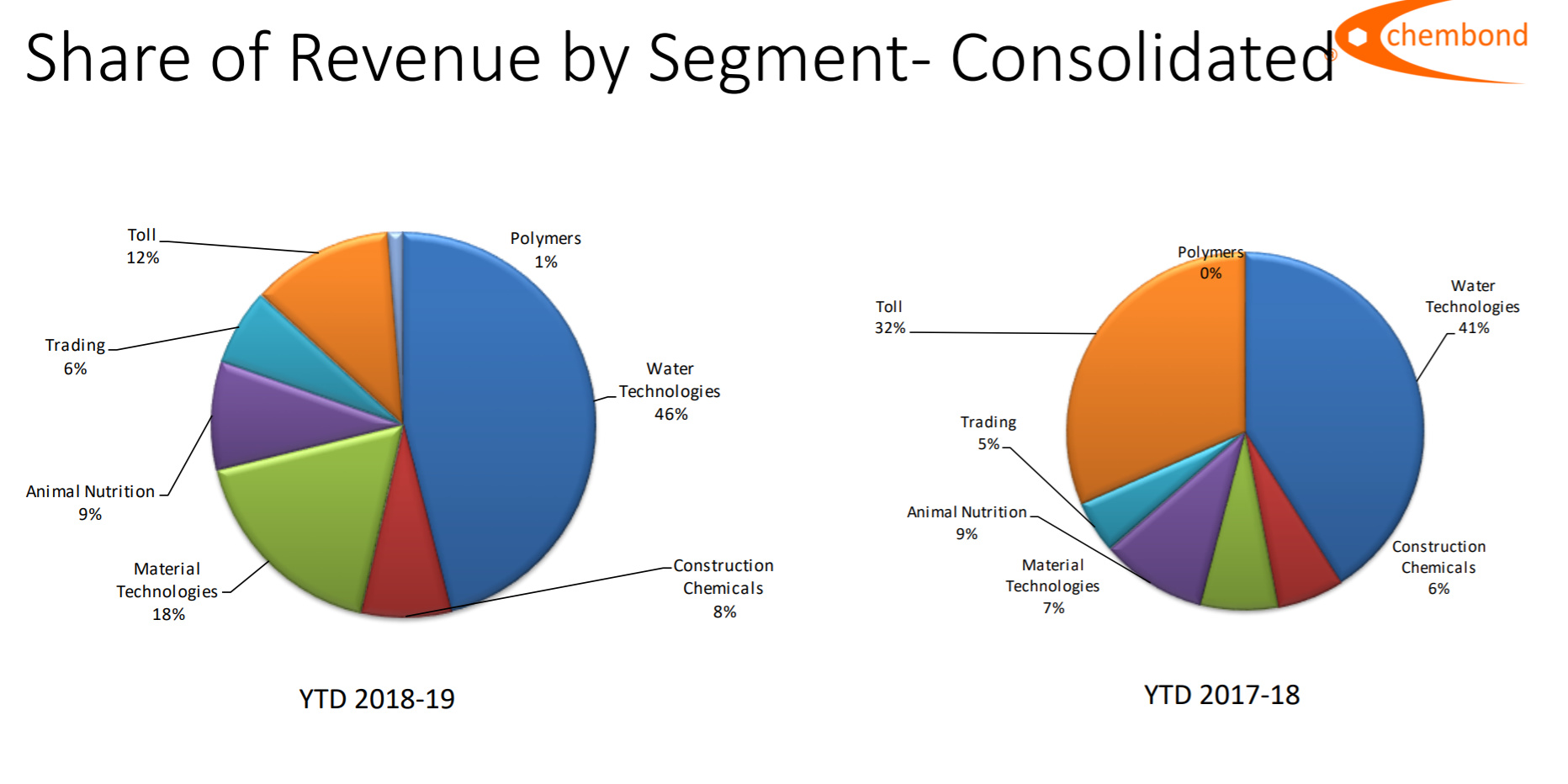

Also between q1/18 and q1/19, majority of “events” have happened within this company, so comparison shows overall 25% jump in sales. In the next 2-3 years, animal nutrition and industrial ( as you mentioned) may be the only contributors ( showing growth qoq).

Also, would you agree/ disagree that animal nutrition is a low margin business with biggies like godrej agrovet/ venkys/ and others dominating.( unless they are able to develop some enzymes, probiotics etc in animal field which gives them an edge)?..and why should Chembond be able to develop something which the biggies are not able to do ( in animal nutrition )?

Also, what does Intermediate stage of Polymers mean. This word keeps cropping up in their AR 18… Like pharma , do Polymers have to go through initial, intermediate , final stages etc. before it gets commercially launched? Can they makes sales in intermediate stage etc.?

In personal opinion , this company is a brilliant pick! He who has patience can reap rewards.

As it was said, management seems to know what they are doing …

Water division has grown consistently around 12% yearly. Polyamide should start contributing.

They do not compete with Godrej Agrovet/Venkys etc. They actually supply to the feed manufacturers. Some of their competition is Kemin/Altech. Kemin & Altech have very good margins, what kind of margins Chembond generates is yet to be seen. A little understanding of their product portfolio tells me that they have products ranging from Commodity & easy to make (mineral mixtures) to difficult ones which are probiotics and enzymes. The company refuses to give margins and will be interesting to see how this evolves.

It is not the intermediate stage of Polymers but an intermediate stage Plant. Depending upon what capacity or the capex involved you can classify the plant as pilot/intermediate/global scale. If you go through FY17 AR it says the following:

‘During the year under consideration, the company has commissioned its pilot polymer plant, at Dudhwada.’

It is a gradual evolution of manufacturing capabilities where each stage of the plant is first stabilized before risking incremental capex.

Thanks!

( playing devils advocate - i am risk averse)

Chembond broadly may be a bet on management ( or rather their R & D capabilities- marketing is no rocket science once you have the right product/ molecule/ enzyme)

Besides what has been discussed in VP as future possible revenue streams, what may favor them is the overall thrust towards GREEN products/ processes ( and managements foresight to prepare products for same)

Water chemicals- bioremediation/ power plant cooling ( dont know how much clean Ganga & other such large central and state govt schemes may favour a small western India focused player)

Industrial- GREEN coatings (low VOC products …

Polymers- GREEN - castor extracts

However, i would like to point out some less-successful JV/ ventures of Chembond to highlight that all that they may touch may not turn to GOLD:

Construction chemicals division is one of their oldest and inspite of same, has not been a cash cow ( forget star)

They had a JV with H20 innovations and the JV was called off after a few years for not getting requisite sales.

Henkel is a world leader and what made them go seperate ways inspite of a such a old relationship

On the face of it , POLYMERS is a very very bold step for a company of this not so big size(Chembond)…

Overall, i continue to be impressed by Chembond and its ability to form JV/ Subsidiaries/ Alliances/ acquisitions/ backward and vertical integration/ not give up when Wockhardt does not go ahead with it but develop its animal nutrition business out of it / make a bold move into Polymers

The company claims to be the only producer of polyamides in India but I came across this article of Business Standard -2014 in which companies like BASF, Rhodia specialty chemicals etc. started making PA 6,10.

So it turns out the market overall for polyamides is going to grow at a good rate but there are big competitors already present with their tie-ups for castor oil procurement.

Report on a pump manufacturer (listed company) WPIL - .waste and wastewater segment, municipal sectors continue to generate business. - backlog of order …

I think the company said that they are the only manufacturers of PA 610 in India and not worldwide. Company seems to be targeting import substitution. They will supply to domestic customers (like toothbrush manufacturers) who currently import from global players.

Peers like BASF, Rhodia and others import RM from India and then export part of finished product back to India. Chembond will be able to supply at lower rates due to localised manufacturing and savings in freight costs.

I think if Chembond’s cost of manufacturing is lower, then they will be able to even compete in global contracts.

Disclosure: Not invested.

EBITDA in lacs

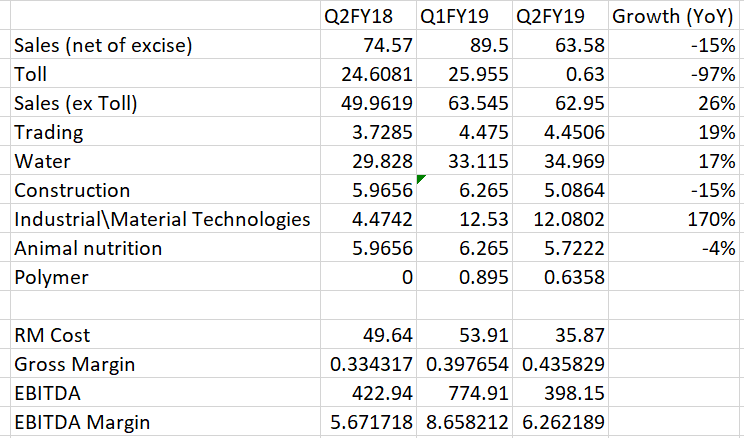

Overall looks like a muted quarter in terms of organic sales growth. Industrial Technologies has been changed to Material Technologies and the growth is due to PSPL and some sales starting out in the erstwhile toll segment. Also although the GMs have improved due to toll going away EBITDA margins have come down due to the continued operating expenses incurred in toll and toll revenues going away. Going ahead it would be interesting to see how Material Technologies ramp up. Also the animal nutrition business is seasonal so next two quarters are bigger quarters relatively.

Following post is a copy of Mr Dhwanil Desai thoughts on this forum (dated Aug 18 - learning/ key takeaways at a meet).

Here are some of my(his) key learning( copied and pasted)

Another interesting takeaway from above discussion for me was that as an entrepreneur, the first prioroty is always survival, growth comes later. This again made me reflect as to how we as investor should mould/rein our expectatation on growth first appraoch. It is important to appreciate businesses that put in place a business model that helps them survie for long, even if it means sacrificing growth in the near term. Eventually, businesses that survives longer and grow at decent pace may generate much better returns as compared to businesses where the sole focus is on hyper growth while the sustainability of business is a question mark

Another interesting point being discusses and that has stayed with me (at least till now!) is the important of focus and not being distracted by working on too many investment ideas at the same time. It is important to focus on one idea and do a deep dive until we really understand the business dynamics very well.

Another takeaway for me was that many of the great practitioners of investing, they focus on business first and valuation comes into play only after business quality is appealing to them. They do not make investing decisions based ONLY on valuations or rather valuation is never starting point for them. Also once they find good quality business, they patiently wait for the business to trade at valuations where they are comfortable buying.

What Mr Desai has put down are his key takeaways from his experiences at a meet…his thoughts/ writings are not at all linked to the company chembond in any way… ( but i see great similarities in what he has written and what i perceive management approach at chembond is ).

If interesting one may read his full posting.

This posting of mine adds no value but in an indirect way is rebutting some of the critics of the story of chembond

Chembond has come with better Q3 numbers.( compared to Q2)

Operating profit % has improved. Operating profit and net profit are showing better numbers.

Toll division has been engaged in the metal treatment division work.

Need to see how the animal nutrition business is shaping up and if more baby steps are being taken in the Polyamide division.

Stock ( even without the new business ventures) has been a compounder is the past. If their new business even do moderately well, compounding should sustain.

disc: invested

Good to see the operations stabilizing and core EBITDA and gross margins increasing QoQ… Material technologies business growth is probably due to the growth in surface technologies business coming. This could be the major revenue/EBITDA driver until polyamide kicks in. A minor dampener is the Animal Nutrition segment not growing, which I guess is due to Vit. D prices shooting through the roof.

Overall as expected the other income is moving to the operating side this year and this quarter should set the tone/base for things to come.