There seems to be some rally happening in the basmati rice stocks. Chaman Lal even after today’s run up looks attractively priced. LT foods has been showing improving financials and the stock has been on an uptrend. GRM overseas, a smaller player has had a phenomenal run up as well.

It is getting listed on NSE source:https://www.bseindia.com/xml-data/corpfiling/AttachLive/9ed531c4-fa91-4e36-bffd-ac983bdee686.pdf

2 Likes

The price has run up. Has the rerating started of the stock or markets are pricing in agri inflation?

This is one of the businesses market is ignoring purely because of its commodity nature. But I am yet to figure out a commodity business with ROE consistently above 20% over last 10 years. PAT moving from 8 cr. to 80 cr. without much of a variation over this period confirms this is not a typical commodity business.

Besides, if the management can build a brand around it then market perception will change. But that’s again a long exercise. Nothing heard from mgmt. on that

Disc: Invested.

3 Likes

The issue with Chamanlal Sethia is that it is unable to generate free cash flows mainly due to high working capital requirements.

Apart from this there is no other issue with the financials.

They do generate good cash flows. There is an error in their cash flow statement as they have deducted value of investments from operating cash flows

Disc: Invested in family and client accounts

8 Likes

The question one often asks why is the stock not being appreciated by the markets. It has been a long time since these financials are being reported. Does Mr Market know something which we are not able to understand?

As someone who has been tracking this industry (and stock) for a while, let me share what I think is the problem with this industry. This is a commodity and cyclical business meaning the margins are thin and unpredictable. Basmati rice requires ageing which means the working capital cycle is terrible (like one year). It is very hard to brand this business as after all it is just rice packaged and sold and on top branded basmati rice is penalised with additional tax. It is very hard to scale the business as basmati rice is GI tagged and produced only in limited geography. There are difficulties in getting back money from customers in Middle East (Iran). This is a very hard industry where most players get bankrupt ( just look what happened to some of the older famous basmati rice brands). This is a mature industry with limited growth opportunities. Probably the only way to make money here is to buy at the lower end of the cycle and sell high.

3 Likes

if you re read what you had wrote that is moat of another category. You well said the industry is very hard only some will survive the bad times… i am not saying CLS is best in it’s class yet a good contender . the balance sheet is good … the promoters has good vision … and it is one of the integral part of ROTI KAPADA MAKAN theme … the growth is slow yet anything beyond 15% per year is good for me so different lens different views…

Disc : invested so my views may be biased

8 Likes

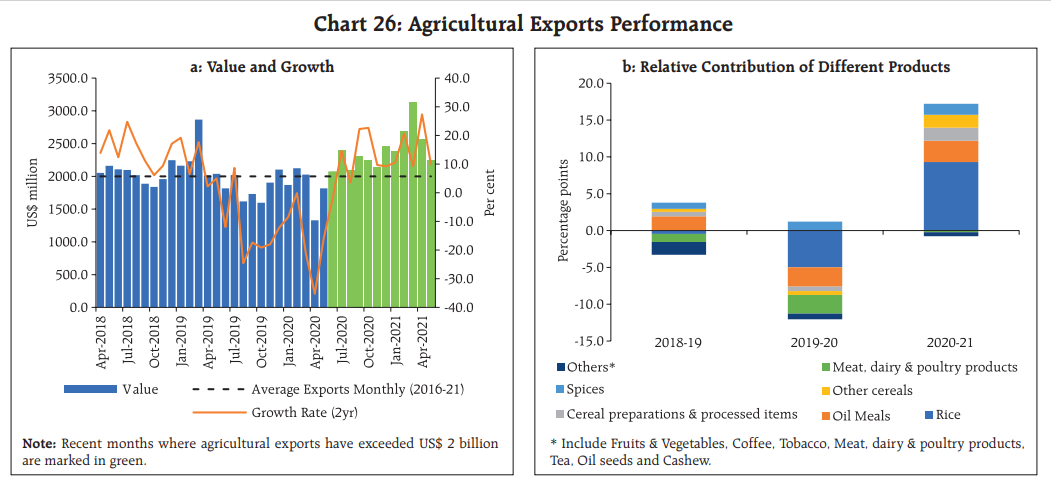

Sharing snip from the RBI Bulletin highlight the agriculture export performance , RICE has greater pie of export …

for full report one can see https://rbidocs.rbi.org.in/rdocs/Bulletin/PDFs/0BULLETINJUNE2021E400EB7F44C349599BC13755EC3111EF.PDF

disc ; invested

4 Likes

Stock has seen recent fall, but after recovery of midcap and smallcap this still is near low of recent fall, any known reason that is keeping price undervalued?

Looose hands selling, if you see volumes are not that much , If you see results they are pretty good no issues with the results.

1 Like

Hi All,

Sharing my notes from Chamanlal’s latest credit rating. It has several good insights.

Regards,

Yogansh Jeswani

Disclosure: Invested

4 Likes

Only one thing that put me out of Chaman lal is Cash Flow

Last 10 years their net profit is 344 crs but their Cash Flow is only 36 Crs and Capital Expenditure to generate this cash flow is 73 Crs all are funded by debt.

if you compare Cash Flow with KRBL the story is totally different

@jalalfunds I feel the cashflow the way it is…is due to the nature of business. They need more and more inventory to grow their topline. If you look at 10 years history, the company has been able to grow its topline by roughly 5x and PAT by roughly 10x. Also in terms of debt-equity break-up in the earlier years the inventory was more funded by debt vs now wherein the equity portion is higher…which overall makes it a stronger company in the 10 years span.

In case of KRBL while there is no denying that the brand and margin it is able to command in the market is commendable but in terms of growth they have been lagging behind…now one reason could be because of the overall size and scale that they are working at…also if we compare chaman vs KRBL on other efficiency and return ratios then Chaman stands out on most of them.

Overall, I feel Chaman’s business is linear and can grow only with more investment back into the business…so the company can do well for investors if it is able to grow its topline and bottomline at a faster pace.

Regards,

Yogansh Jeswani

4 Likes

CRISIL Ratings has revised the outlook on the long term bank facilities of ‘Chaman Lal Setia Exports Limited (CLSE) to ‘Positive’ from ‘Stable’ while reaffirming rating at ‘CRISIL A-‘.

Chaman Lal sales growth and profit growth are commendable no doubt in that but look at their cash flow and conference call transcript of KRBL will reveal the truth.

It is very strange that people are dumping this stock because of results, If you see they are sitting of 240 Cr of cash with Inventory of 81 cr where market cap is 900 Cr , where prices of rice is at top.

News on Lift ban of export of Rice by Many other country, This is a temparory problem not fix.

PE at 8/9 is good for this stock.

1 Like

Sir , Now this Q , they have 240 cr of cash and 80 cr of inventory , whats the take now ?

3 Likes