Q1 2020 earnings call.

Needless to say all Q are on the employee cost & expenses

Q1 2020 earnings call.

Needless to say all Q are on the employee cost & expenses

“India has approximately 55 school boards, 359 state universities, 123 deemed universities, 47 central universities and 260 private universities. Apart from these, there are 107 other institutions such as IISc/IITs/IIMs/NITs/IISERs/IIITs/NITIE and 12 other centrally-funded institutions.”

“Upto September 30, the registration fee, as well as annual maintenance fee, has been waived off. For students, the annual usage fee and first download of an academic certificate download will be free till the age of 27.”

I have gone through the Q1’ FY20 con call . PFB my summary of understanding ,

Revenues

Consolidated Revenue of 73 Cr in the first Q vs 50 Cr Y-O-Y . The split on major heads

Issuance charge - 15.66 Cr to 19.22 Cr

Corporate Expense - 5.55 Cr to 5.32 Cr

Transactions charges - 9.67 Cr to 9.86 Cr

Online income - 6.85 Cr to 7.64 Cr

eVoting - 57.85 L to 44.86 L

CDSL has received IT refund of 2.2 Cr for assessment year 2012-2013.

Expenses

Employee cost revision is about 30% across board . the last full scale revision happened in October 2016. Yearly around 2-3 percent increase was given. The employee cost is expected to be 10 Cr-11 Cr from now on in every quarter

CDSL major expenses - system maintenance cost up by 71 L , doubful debt 1.62 Cr , KRA Charges 60 L.

Business Statistics

CDSL have added net 6.38 L new accounts VS NSDL 2.18 L incremental markets share is 75% for this quarter.

National academic depository records up from 40.41 L to 1.71 Cr records.On track

to generate revenue from Sep’19. MHRD is expected to notify the charges shortly.

Insurance repository around 5,000 health insurance added. Total 2.5 L insurance policies as on 30th June.

New unlisted companies added is 633 taking total to 2050. This trend is expected to continue.

CDSL run rate of adding unlisted companies is ~200 vs NSDL ~500

Others

Cash at end of Q1’20 is 715 Cr , 50 Cr goes to dividend & 30 Cr is refundable deposits . the net is around 650 Cr.

No Impact on inter-clearing corporation in business.

There is an employee count increase on account of the government project & for the upcoming plans including unlisted companies addition.

CDSL has not approached SEBI for annual issuer fees revision . the last was revised on 2015.

Out of 65,000 unlisted companies , 2000 odd is with CDSL & around 4,000 with NSDL . Still 60,000 companies to be added.

On the buyback & action on utilizing the cash , it will decided after new MD is appointed.

Lastly about one specific government project

CDSL is working on government project under guidance of supreme court committee .CDSL has maintained it to be confidential but I think it must be related to PACL.

In management words,"this is a lower margin business as compared to some of our existing businesses, but because it is a government, we are doing it because it is like mandatory.

“The work is to ensure refund to investors in a particular company who are defrauded by the company and we have been appointed to create a database of these investors, call for their certificate and receipts based on that we will decide on the refund and then we will credit the refund to the investors account. So, once this is done it is a one-off event.”

The potential revenue billing based on the number of applications i.e. per application basis so it all depends on the number of applications which come in because it is an old matter many of the applicants do not have their certificates, they do not have their receipts so those type of challenges remain.

Because of the government project , Expense related postage, telephone & communication increased by 62 L & Expense related to electricity is 70 L.

These are expected to be reimbursed at actuals

The contract is for one year, but there are large number of investors about 4.5 crores investors.

This is carried out by CDSL Venture Limited

Thanks to analyst team for questions asked & management for answering all the ones except a confidential category related item.

Disclosure:

CDSL is part of my portfolio & and individuals are requested to do their analysis before investing.

Special Mention

Thanks to all VALUEPICKR FORUM Members. I dont remember spending a long time with full concentration in reading any report summarizing it. The entire credit goes to this forum and its members.

You can find a detailed blog by aditya kondawar above in this topic itself. It was posted by @bhaskarbora67.

First time in five years CDSL has shown lower numbers. Its TTM Sales is lower than Mar19 figures.

I suppose, it being the only depository the market does not know how much to value it. It is unknow whether in the near futures the sales will rise or fall, because these things are not predictable.

IMO, the economy is not doing well, I do not expect throngs to open Demat accounts. I expect the sales to fall further, and due to absence of growth this stock’s EPS would plateau. This is a cyclical stock, and to be bought when the price consolidates, when market discovers a reasonable price.

Yes, the TTM Sales is lower but at the same time TTM EPS is higher.

It’s tax rate is low at ~20% and if started giving at regular rate (~30%) then it may dent its profit in future. Even at current PE ratio of 24 this stock is looking expensive considering last 2 years EPS growth.

Agreed it is cyclic stock but if we consider the broader market has picked the top in Jan’18 then we are coming to lower cycle of market and picking up CDSL at lower cycle will give opportunity to buy low. We need to watch next 5-6 years results and based on that data one can make his views in next bear cycle.

Disclosure: Invested from IPO and added later so views can be biased.

I have been spending some time on the company. I have a few questions, if any one can help resolve them it would be great.

While CDSL has been aggressive in adding BO accounts and has a dominant market leadership position in the incremental account openings. They have been quite slow in adding ‘live companies’ under their fold. CDSL has grown at 8% CAGR over the last 6 years while NSDL has grown at 15% in the same time. Given this dynamic wouldn’t NSDL have a much stable source of annuity revenue?

When we see the revenue mix of NSDL- from FY13-FY18 (FY19 break up not available yet), transaction revenue has grown at a CAGR of 24%, for CDSL this number is just 12%. Why is this the case? Given the market share has increased for CDSL, wouldn’t the growth be similar, as pricing is also determined by SEBI. Does it mean that the # of trades happening in the accounts that NSDL has is much more than CDSL?

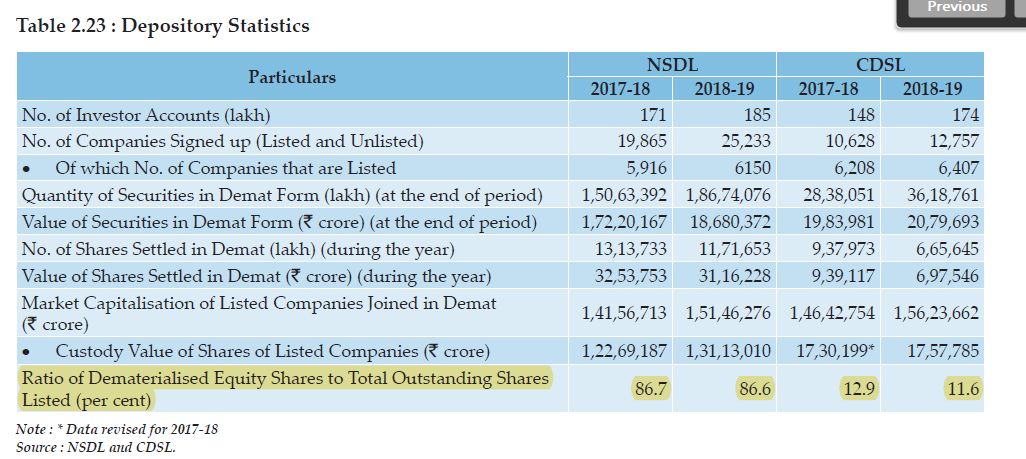

SEBI in its annual report comes out with a table talking about depository statisctice. Thanks @bozo_investor for pointing this out. Within the table there is a stat which I don’t understand. Can someone please explain to me the highlighted portion and why is CDSL’s % so low here?

Discl- Not Invested

hi Rohit

with respect to point 3, NSDL has a very large market share of institutions (has almost 22 banks as its demat clients), while CDSL has more retail investors. however, pls note that the revenues are not dependent on value. if a promoter pledges its holding to a bank, they will hit the NSDL account of the bank, and thus the value share of NSDL would be higher to that extent. but the trades in the pledged would be miniscule, so NSDL does not earn any revenue from it.

further NSDL is the only depository mandated by regulators to service demat accounts for FPIs.

on point 1, a large number of unlisted companies have demat arrangement only with NSDL since NSDL provides cheaper rates. CDSL started following NDSL rates from last year. in the table shared by you, it can be seen that more listed companies are on CDSL platform.

no idea with respect to point 2.

hope this helps.

Hi Umang, Thanks for your answers.

On Point # 3. I understand that the revenue is not dependent on value of stock traded. What I don’t understand is why is the % of demat shares to O/S Shares so high for NSDL and so low for CDSL. It has been the case for many years. I don’t understand what this implies and what does one infer from this data

hi Rohit

would you not agree that a large of DIIs and FPIs on NSDL platform would skew the number of o/s shares in favor of NSDL? i think this is the sole implication.

In my opinion, this number although important, is not valuable to arrive at an insight about the 2 depositories market shares. Number of BO Accounts might be a better proxy.

hope this helps!

Yes, Umang I would agree with you

They have got good reputation among value investors community.

Why is the board so lazy to fill the seats or to appoint an MD. This is a serious concern. They want to run CDSL like the old BSE?

Q2’20 Results out

Key Highlights Y-O-Y

Earnings Call

Key highlights