Q2’2019 results.

Income up by 26% Q-O-Q.

Expenses nearly same Q-O-Q

Net profit up 36% Q-O-Q

Q2’2019 results.

Income up by 26% Q-O-Q.

Expenses nearly same Q-O-Q

Net profit up 36% Q-O-Q

Q2 Concall summary (source: capital market)

The company has posted 11% growth in the operating income to Rs 62.89 crore, while the net profit moved up 12% to Rs 30.15 crore in Q2FY2019. The other income has increased by 7% to Rs 9.74 crore.

Among the key revenue segments, the annual issuance charges have increased 18% yoy to Rs 16 crore in Q2FY2019, transaction charges 3% to Rs 10.26 crore, online data charges 54% to Rs 10.17 crore and e-voting charges 19% to Rs 3.21 crore, while IPO corporate action charges declined 27% to Rs 6.16 crore.

The company has continued to gain market share with incremental demat account share was higher at 64% in Q2FY2019 and 47.57% at aggregate level end September 2018 up from 47% end June 2018. The aggregate demat accounts with the company increased to 1.60 crore end September 2018 from 1.54 crore end June 2018.

The company has added a new revenue segment called VDR (Virtual Data RoM), where companies listing through IPO stores data to be used by merchant bankers, auditors etc. This segment has made revenue of Rs 3-4 lakh, while its expected to increase once more IPOs enter the market. There were no big expenses for setting up this service.

NAD which provides services for online document storage has tied-up with 460+ universities.

MCX Menthol settlement has been facilitated through CCRL in October 2018, while the company expects to facilitate non-agriculture and non-metal commodities clearing and settlement in Q3FY2019.

The employee base of the company, on consolidated basis, has increased to 238 end September 2018 from 226 end June 2018 and most were recruited by CCRL.

After Supreme Court verdict restricting use of Aadhar Card for E-KYC verification, the company is planning to go for verification through QR code, which does not require additional expenses.

As per a new regulation, the MD of a depository and market infrastructure cannot serve as an MD for more than two terms of 5 year each. The MD of the company is completing his two terms of service as MD and he may not continue in service after 31 March 2019.

Out of 64000 unlisted materialized public sector companies 200 companies are in the pipeline of CDSL so far for the dematerialization of shares.

The market share in KYC stands at 60% in Q2FY2019 and the company has 1.7 crore KYC records with itself.

The capex of the company stands at Rs 5-6 crore for FY2019.

MCX decision to settle the contrac through CCRL is very good milestone in the CDSL lifecycle. I consider MCX being a mature player in exchanges and they would evaluated quality/technology/realiablity and not only cost while taking decision. When CDSL gained this business, it is major competitive lead CDSL has taken in my opinion. I am not aware about MCX working with other clearing corporation as well and if any member can provide insight on same, it would improve my knowledge for sure.

Secondly, managing higher incremental share in demat account also working well for CDSL. Like the development in the company.

Disclosure: I am invested in BSE due to superior Dividend yield offered at current price, which has around 24% equity interest in CDSL and hence my view may be biased. Investor shall do his/her own due diligence before making any investment decision.

Another reason for MCX to settle with CDSL could be because they recently bought stake in CDSL. So they are giving business to sister concern.

Q2 concall clarified the new rule that SEBI has bring into , floating a depository will require 100 cr as capital and corporate house can hold maximum of15% stake.I think this will soothe investor concern on CDSL will face increasing competion on its core depository business. Some competion will always be there in form of Kyc business from Link-intime and all.

Q2 Conf call details.

looking at the price and volume pattern,It seems that smart money is buying CDSL at lower levels

They may be selling also. Can you please share the logic for it.

First major up move in recent days came on 19th Dec 18 with Voulme of 37 Lacs shares. CDSL has not yet broken the low of that day. After that day, the stock fell with less volume and moved up with higher volume. This is coupled with positive divergence in RSI. I think major up move will come after 238.90 which is the high of 20th Dec 2018.

One should wait for confirmation before taking any buy decision. The stock should close above 233 (50 DEMA) level for at least a week because a lot of people have stuck in this stock at every higher level. They may want to get out at every rise. Sustaining above 50 DEMA and breaking above 239 level will give confirmation of sustained buying

Long post alert

I am a fan of businesses which have revenue streams which are certain and recurring and CDSL seems to be one such business. I have started looking at its 5 year financials and the first part which I want to shed some light on is the Operating revenue.

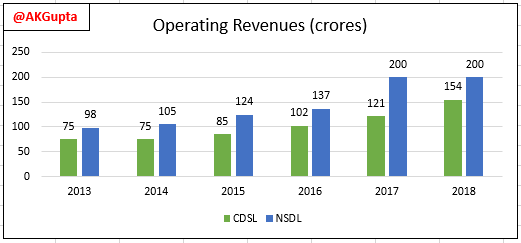

Firstly, refer to the below graphic (shows standalone numbers):

The above shows that the 3 biggest streams of revenue, making up 85% of standalone 2018 operating revenue are: Annual issuer charges, transaction charges, and IPO/Corporate Action charges.

Out of these 3, IPO/CAC revenue stream did not exist in 2013. In 2018, it contributed 20% to revenue!

The other 2 categories (Annual issuer and transaction charges) combined have almost doubled between 2013 & 2018 but their weight in the overall pie has reduced because 3 new revenue streams (IPO/CAC, E-voting & ECAS charges) have started contributing meaningfully to topline! This shows mgmt is active in exploring new revenue streams and growing the business.

CDSL mainly earns revenue on the basis of number of demat account holders registered with the Depository and on the basis of the transaction volumes generated by the demat account holders.

As has been pointed out above, maximum charges that CDSL can levy are regulated by SEBI.

So this business is mainly about maintaining cost competitiveness & leveraging economies of scale by expanding the breadth of network.

This is also mentioned in the RHP (Refer below extract):

Further, as a monopoly, NSDL used to charge higher transaction charges from users before CDSL came in and NSDL was forced to cut its prices drastically to compete:

This further proves the the depository business is about maintaining cost leadership with limited scope for value differentiation.

Financialisation theme is real: The demographics of our country (young population, growing awareness of the benefits of investments in financial assets) means that both the DPs have enough room to grow the combined revenue base of approximately 350 crores (standalone) as of FY18.

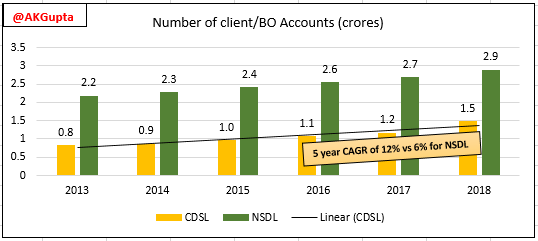

Note in the above, CDSL has been growing revenues consistently while NSDL has flatlined in the last 2 years implying that CDSL has been winning markets share. This is also attested by the growth in incremental client accounts at both the depositories (shown below):

Growing revenues on a fixed cost structure means healthy PAT CAGR on the back of increasing operating leverage! ![]()

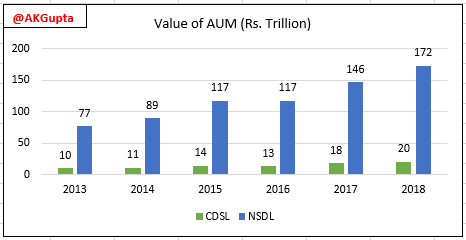

One area of concern I have is the gaping difference in the value of securities held in custody by NSDL in comparison with CDSL (see below chart):

Knowing that:

Charges per transaction between the 2 depositories are not very different, and

Operating revenue difference between the 2 depositories is not a lot as well (as shown above),

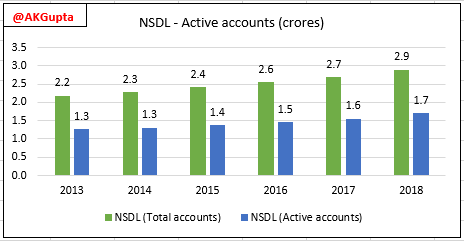

this implies that NSDL has lower number of actively trading members as a ratio of total members as is also attested by the below graphic:

Ratio of active clients to total clients is ~1:2. But the fact still remains that NSDL is managing ~8.5x times money as CDSL which could turn out to be a competitive advantage in the long run for NSDL. (More on this below)

The Network Effect:

The depository business is dependent on the typical network effect, which is measured by the following 4 factors mainly:

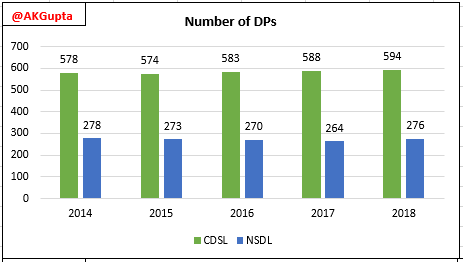

Number of DPs (mostly brokers, banks) enrolled (CDSL leads but that could be because it attracts smaller brokers (with net worth of 1-2 crores) to its fold as well)

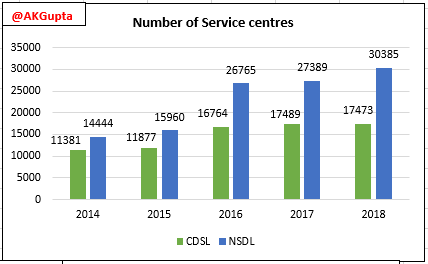

Number of DP service centres/customer touch points (NSDL leads here even with lesser number of DPs…could be because its DPs have a larger branch presence compared with CDSL)

Number of client accounts (NSDL leads but CDSL is fast catching up)

Value and volume of securities held in custody (CDSL is far behind but both the players are growing well)

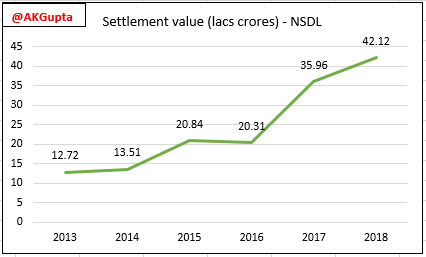

Value of securities traded or settlement volumes (NSDL reports this number in its AR but couldn’t find similar statistic for CDSL…if anyone here comes across this stat for CDSL, kindly share)

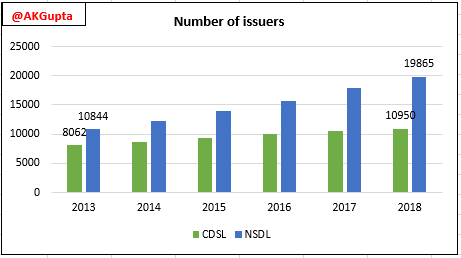

Number of Issuers registered with the Depository (NSDL is leading and growing faster than CDSL over last 5 years):

Clearly, CDSL has a larger number of DPs and a larger number of client accounts but it lags behind NSDL in terms of customer touch points and value of AUM. Clearly, NSDL has a better network (bigger brokers are likely to be in business for longer and will have more affluent clientele). Look at the below extract from the 2015 AR where CDSL mentions about the launch of “Limited DP” focused on small brokers.

Summary:

CDSL is run by an ambitious mgmt which clearly shows up in revenue CAGR and advent of 3 new revenue streams in last 5 years (diversification of revenue streams is a very good sign!).

Depository business is dependent on transaction volumes in capital markets, network breadth & assets under custody. NSDL leads in terms of these metrics but CDSL is playing catch up well in terms of expanding number of DPs, number of issuers and number of client account on its platform. CDSL needs to work on growing its AUM.

Depositories don’t have much room to modify prices because of inherent competitiveness and because charges are decided by SEBI so a strict control of costs is necessary. This lends operating leverage when revenues are growing on a fixed cost structure.

There is significant room for the overall market to grow and it is already happening and should continue to happen given the dynamics of our country.

Disclosure: Invested recently with a long term outlook. The stats are taken from ARs, RHP for both the depositories

Just to add to above, going by the business model, it’s not a space many corporates will be interested in even if SEBI allowed them to open up a depository. Mainly because there’s no pricing power, limited scope for further innovation and high regulation. The only thing a new depository will do is make existing depositories further reduce transaction charges and make the economics of the business less attractive for everyone.

Plus, the relationships and network built by existing depositories over a period of 20+ years of operations will be hard to replicate. Just my opinion…

SEBI is open to new depository.But its not attractive to promote new depository. As per new SEBI directive it needs 100 cr as capital and promoter group can hold maxium 15% max.

Thanks for sharing.

Can you direct me to the source/link of this SEBI directive?

I got this info from Q2 Concall where management mentioned it. Please go through the Q2 concall transcript

CDSL’s listing price was Rs. 260 and IPOs are designed to be overpriced. The whole machinery works to make sure this. Now, the price is 20% below the IPO price, and it looks interesting.

The management spent Rs.76 Crore in 2018 on fixed assets. A big sum in its accounts. Where did this money go?

The money went towards an office space purchased in Lower Parel, Mumbai

Dear Sir,

Thanks for sharing your invaluable thoughts. Everything is in order for CDSL except for the fact that it does not have control over its sales as well as profits. Its sales are proxy to increase in financialisation and Profits on charges mandated by SEBI. In such a scenario its it would be a slow but steady compounder.

I feel it is a pseudo cyclical stock. When the stock market fever is common, enthusiasm is high, cdsl will earn. When it’s not, which could be a span of five years at a stretch, the earnings growth would be absent, in which case the stock may collapse to interesting levels of PE.

I don’t mind owning a slow but steady compounder. Fast growing companies scare me to be honest because you never know which quarter will be bad and then there is a steep correction.

Despite having limited control over profits it has gone from 43 crores to 100+ crores PAT in 3-4 years. It is a proven and durable business model and one which I wonder how it could be disrupted.

To the point about cyclicality, every business in the market is cyclical. When there’s a downturn nothing is left out. So in my opinion, it’s unwise to expect our businesses will hold their ground when others are suffering. No business runs like that.

I have people in my office who were never exposed to equities or Mutual funds who now want to open a demat account. Financialisation of the Indian economy is a secular trend for years to come.

That said, I agree the price is not “cheap” right now but that just depends on a person’s time horizon. Good businesses are rarely ever cheap and the wait for the right price might just be forever. My preferred approach is buying if the business is good and doubling down when the price is attractive. That said, there’s no alternative to patiently waiting for the complete story to unfold.