@tirumal & I visited their office last week. Sharing notes from the visit:

Market Size:

• 500,000-600,000 Tons global market

• EU & UK largest importer of beans followed by US

• Top suppliers are from Brazil, Columbia, Vietnam, Indonesia

• EU: 90,000 Tons. Suppliers predominantly from Asia & Columbia

• UK: 30,000-40,000 Tons

• US market: Approx 80,000 Tons of which 40% is addressable market currently catered to by Nestle, Kenco (part of JDE), Folgers (J.M. Smucker), Kraft Heinz Foods etc., rest is non-addressable

• Brazil & Mexico : Brazil only allows use of home grown green coffee & doesn’t allow imports.

• Japan : 35,000 Tons liquid coffee - Unique to Japan

• India & China: Predominantly tea drinkers. Coffee market likely to be approx 10,000 tons each

Competition & Production Capacity:

• Globally approx 600,000 tons of which 250,000 tons of Freeze Dried & rest Spray Dried

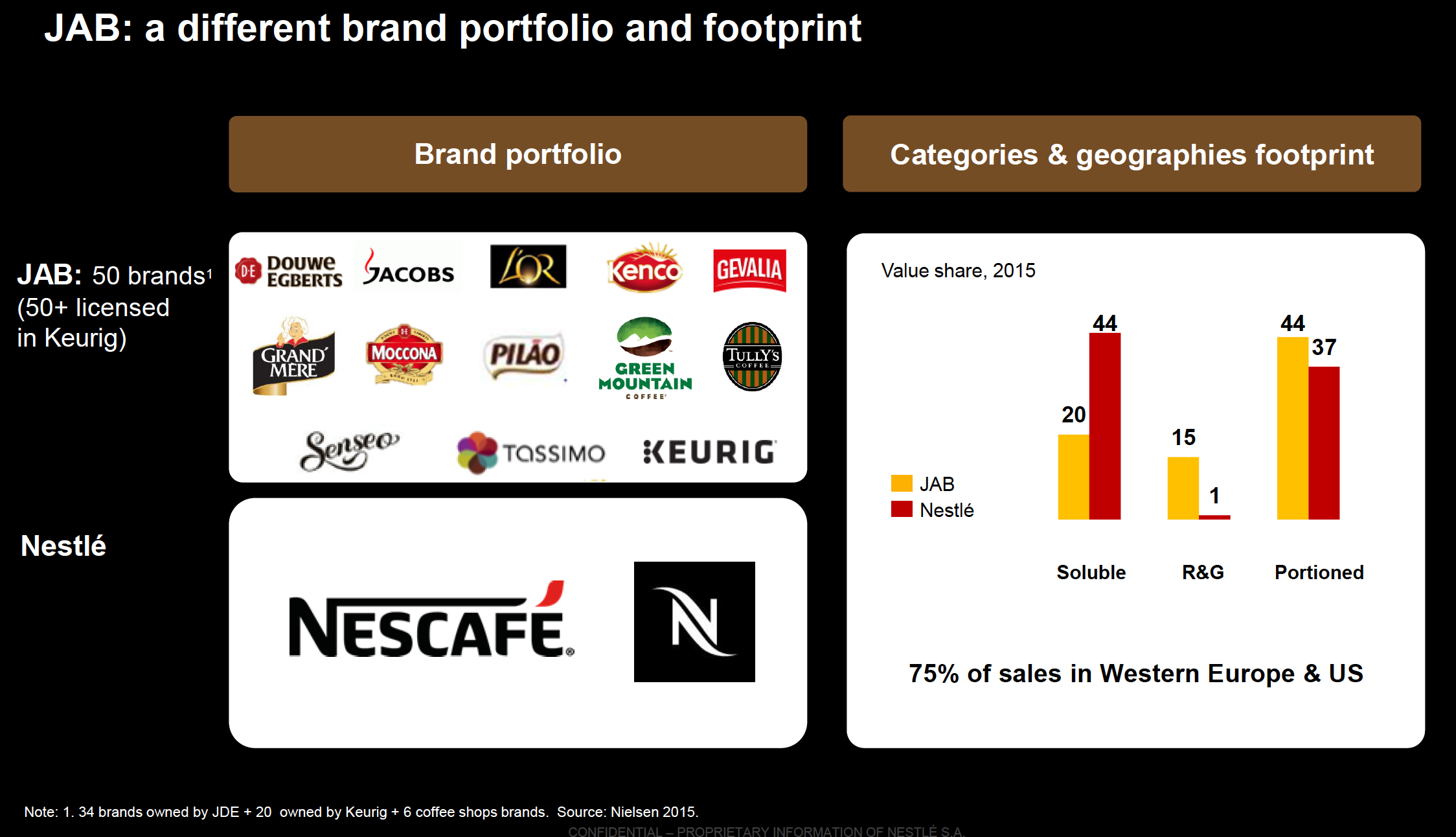

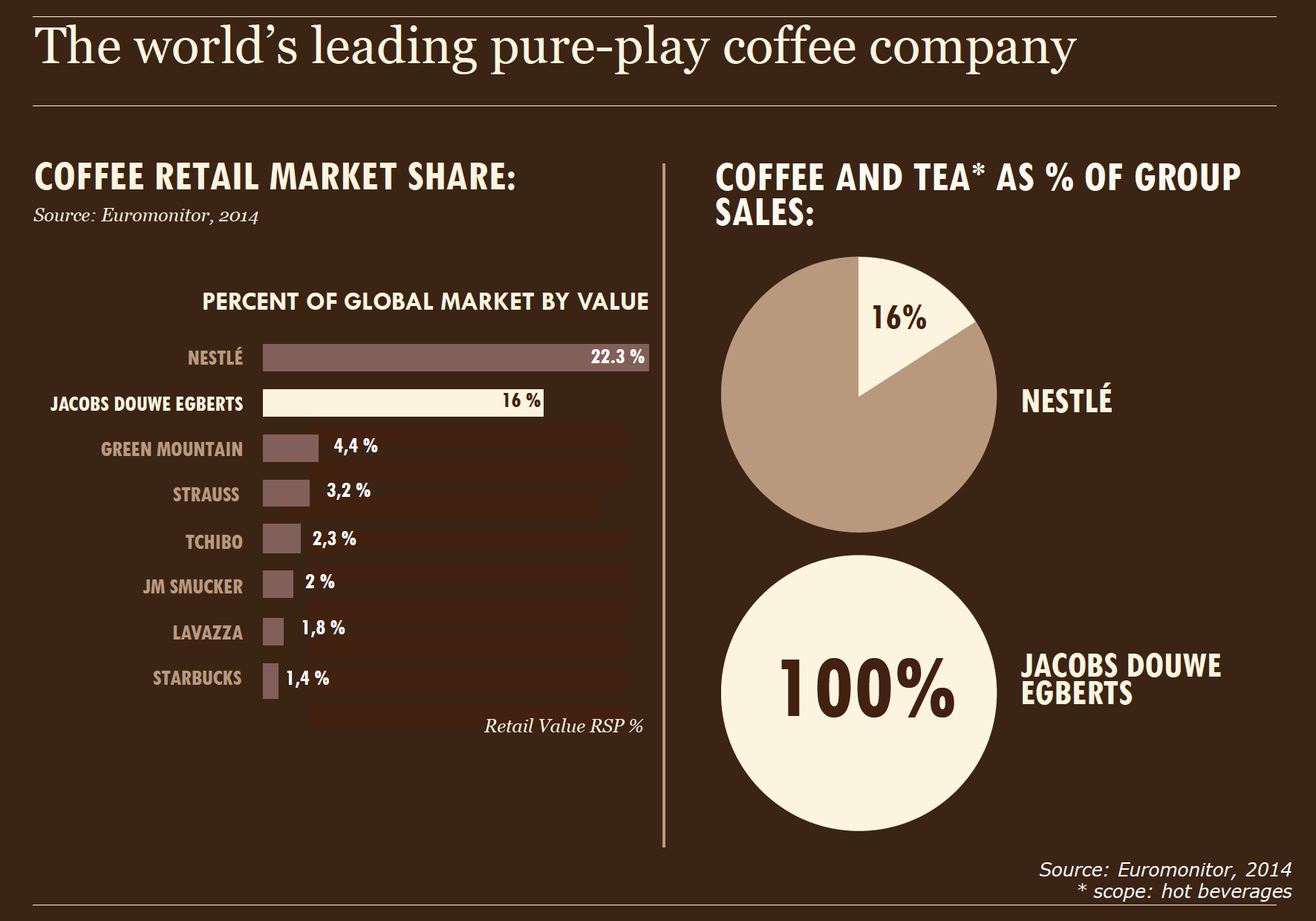

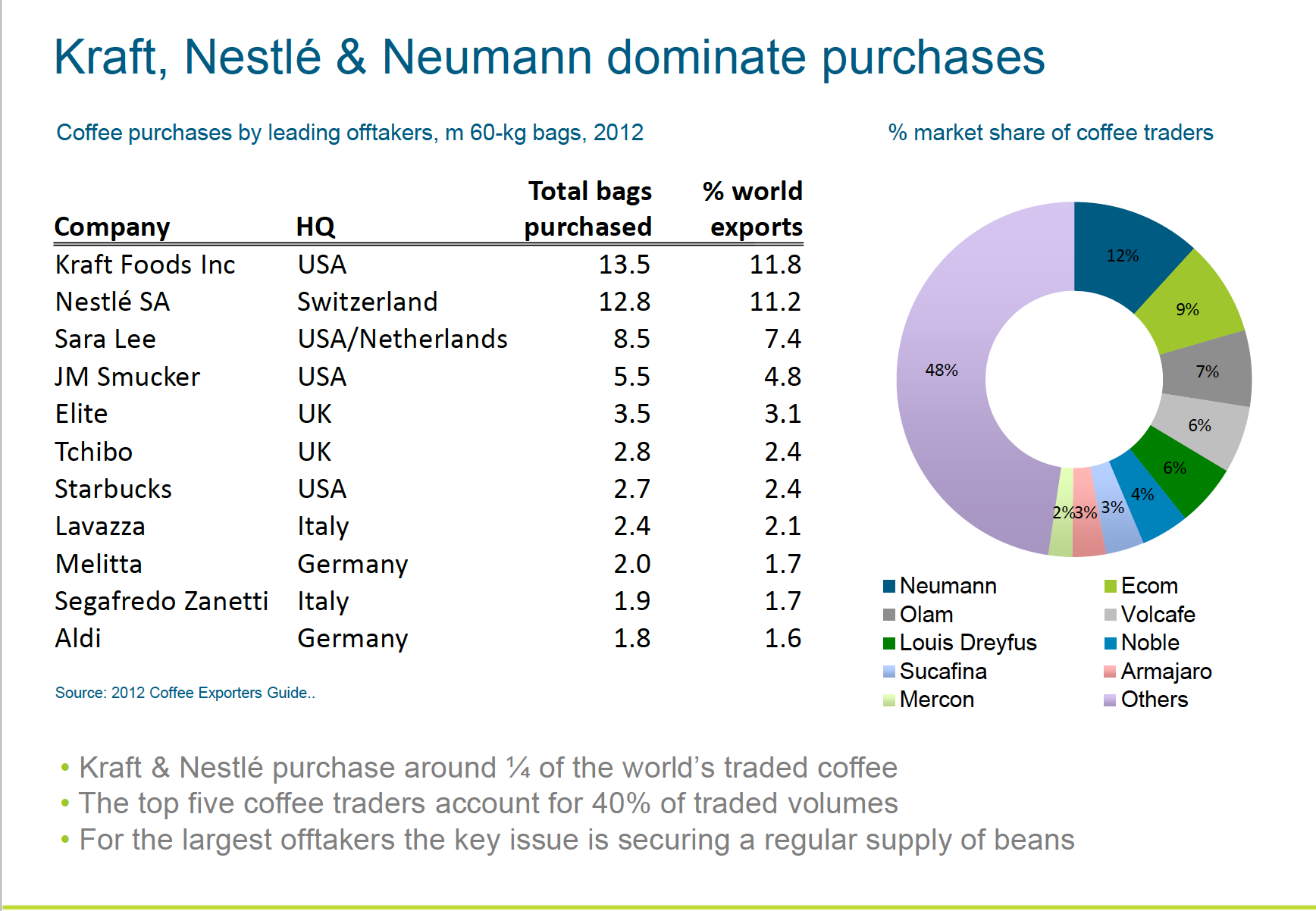

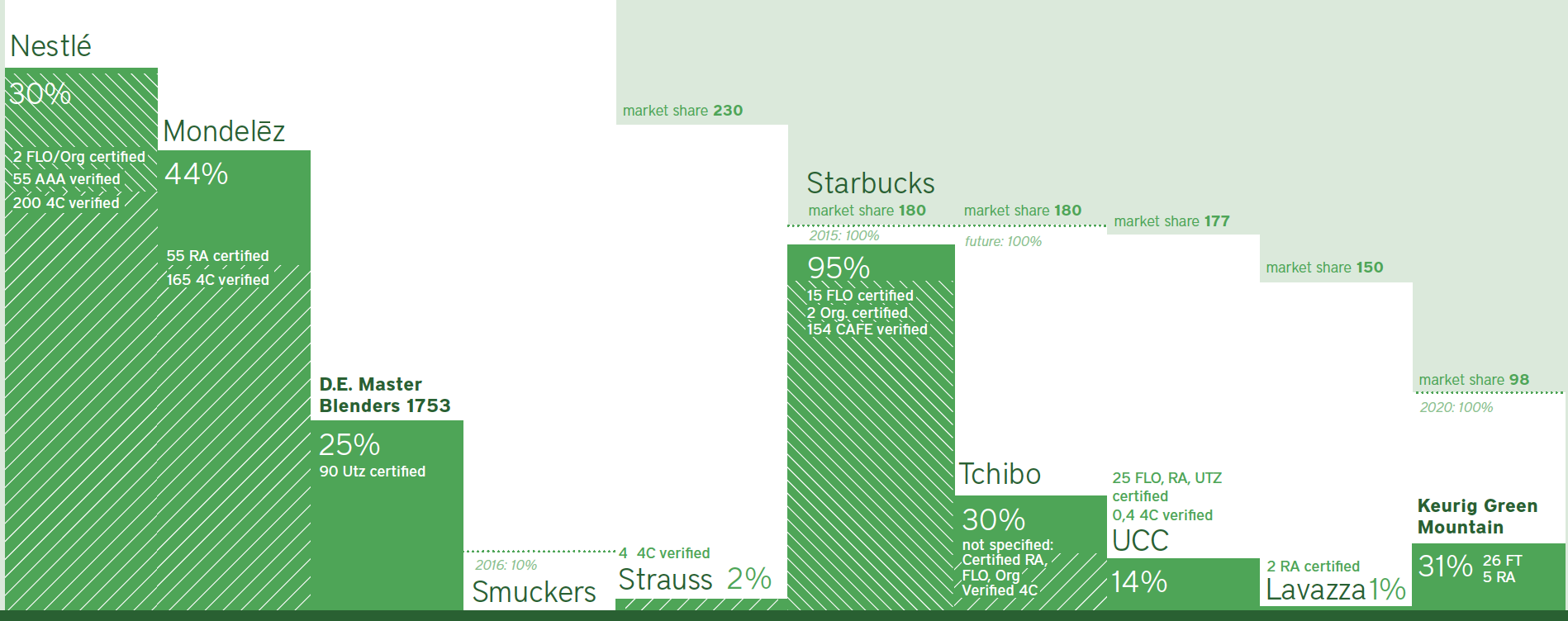

• Nestle is the global leader (150,000 – 250,000 tons of which 80,000 tons in FD capacity) followed by JDE [Jacobs Douwe & Egberts – with Mondelez merger ] (50,000-60,000 tons), Kraft Heinz Foods, Folgers (from J.M Smucker), DEK (Deutsche Extrakt Kaffee GmbH).

• Private label suppliers include ColCafe SAS (Columbia) (25,000 tons), Klasik (Vietnam) (20,000 tons), Olam (Vietnam) (15,000 tons), Tata Coffee (8,000 tons), Super Singapore (part of JDE, majorly 3-in-1 product)

Market growth & Coffee drinking habits:

• Global Instant coffee growth rate hovers around 2.5% over the past 4-5 yrs

• However, US & EU market de-growing by about 1% each year over past 4-5 yrs

• Moving towards micro ground coffee (soluble with roasted coffee beans).

• Ready to drink segment likely to include coffee consumption in tetra packs

CCL Market positioning:

• Production capacity 35,000-45,000 tons (of which 11,000 tons in Freeze Dried with new plant at Chittoor) - Target customers include Re-packers & Ingredient manufacturers

• Domestic (India) market visibility increasing and gaining traction across both Own Brand (Continental Coffee) & Private labels.

• Brand building exercise likely to be in focus over next 2-3 years. Team in place with Targets being drawn for next year.

• Working on innovative products to convert tea drinkers to coffee drinkers.

Strengths:

• Economies of scale & Variety of product offerings (close to 1,000 product varieties)

• Capability of leveraging long standing relationships with customers, employees across the globe.

• Product Quality: CCL follows stringent external & internal quality checks (internal test lab equipped with world class test equipments). Company has spent Rs. 100-150 Cr over the past 5yrs on R&D.

• Likely to be 3rd largest global player in FD market with 11,000 tons (once production starts at Chittoor plant).

Takeaways:

Scope for growth in revenues & profits:

• CCL (currently growing at approx 15%) is likely gaining market share from smaller players in the global market (global market growth at 2.5% y-o-y)

• Japan has 1 vending machine for every 14 people (with consumption at 35,000 tonnes liquid coffee) - Scope for growth for vending m/c’s in India.

• Scope for CCL to premiumise products to increase both top & bottom line.

• Promoters buying from open market in case of fall in stock price (seen last year & recently b/w mid-Jul to mid-Aug 2017). – Shows faith of mgmt in company’s future/growth prospects.

Key Risks:

• In case of delay in commissioning of new plant at Chitoor (5,000 tons): Such a scenario could topple bottom line as this facility is exclusively for producing higher margin Freeze Dried product. Capex requirements could also escalate.

• If existing bigger global players like JDE etc come out with expansion plans, market is likely to get disrupted as current global production capacities exceed demand

• Risks in Brand building & Execution: Brand Marketing spends likely to increase over the next 2-3 years. Majority of companies fail to promote brands with only very few brands succeeding in creating niche & sustain in the long run.

• HUL spends approx Rs.150 crores on brand building in India out its Rs.1,000 Cr revenues – For CCL, brand building spends may dent bottom-line in the medium term.

• US market penetration may not pan out as planned or get delayed

Discl: Holding. No transactions during the past 90 days.