Interesting view point on CARE -

5 Likes

Good analysis but this assessment should include some hall of shame for Care rating as well. Google for Care rating’s role in CRB scam as they rated a fraud CR Bhansali ‘AAA’ even when they were going down. Subsequent regulatory action made NBFCs unviable for 10 yrs and 90% of of them just closed down in late 90s. This had tremendous impact on the economy at that time but somehow Care escaped the punishment. In US they would have closed long back. I have serious doubt that rating agencies can make it big here. They are poor copycats of the western model. Look at ILFS event which only proves that ratings are being distributed from AC rooms and not through a basic level of field work and fact finding. Either we will have more competition to compensate for incompetence of existing ones or more customers (MFs, Insurance etc) will have in-house assessment teams giving less importance to what rating agencies write. Situation will become similar to what happens to most of equity research reports anyway. In either case they are not up for supernormal profits like previous capex cycle.

This is my view and I am not invested till we have regulatory framework for rating agencies like fines for wrongful or poor rating.

3 Likes

i agree who needs these rating agencies … not sure why they exists.

1 Like

well, I get the sarcasm but 5Y PAT and revenue CAGR of 10% and with 6 competitors in the marketplace which is relatively small with no real differentiation. Additionally, any capex cycle can never be like 2004-08 again. The right question should be “who needs Care Ratings and why?”

2 Likes

The best way to check who needs CARE Rating is look at customers renewal rates … Is it consistently high … Is the market share going up or down , if so why …

@amitcontrarian has presented his case pretty soundly through the link provided , would like you provide counter data to the same .

One client going down among lacs or thousand of client is not an issue … It happens across industries and hence we see bad debts in all companies , and hence we have IBC etc … The discussion is interesting but would like to see facts talking , This will be useful for all of us

5 Likes

Moody and S&P rated most of the subprime debt ; I have not read any of them being penalized for it. The point I am trying to make is the rating agencies are required to rate debt and irrespective of the rating implication , they have renewals . Its a moral hazard . my view would be to dispassionate while judging a business and judge on the basis on the basis of ROCE rather than morality.

1 Like

no Sumit point is CARE quality is low … CRISIL and ICRA will continue to dominate the markets.

1 Like

If i’m not wrong, CRISIL gave IL&FS pretty good ratings recently too

The question is whether CARE is a good stock to buy now with attractive valuations

Sumit,

Appreciate your efforts in bringing out critical aspect about neglgence for credit rating industry in general and CARE in particular in context of CRB Capital. However, subsequent to your message I googled and found two link which have contradictory information. In the enclosed link, I find credit rating of “A” being issued by CARE for FD programe in 1996 as against AAA mentioned by you in post. Enclosing link for your reference:

In view of above, I would appreicate if you can provide authentic link which provide information about CRB being rated “AAA” by CARE Rating, if possible.

While not to underestimate concern, finally credit rating is an opinion and we shall not try to over read from one default. Consistent error of judgement is defintely cause of concern. For every credit rating company with histroy, there is bound to have default of rated paper. Hence, it would be important to see consistency in rating migration.

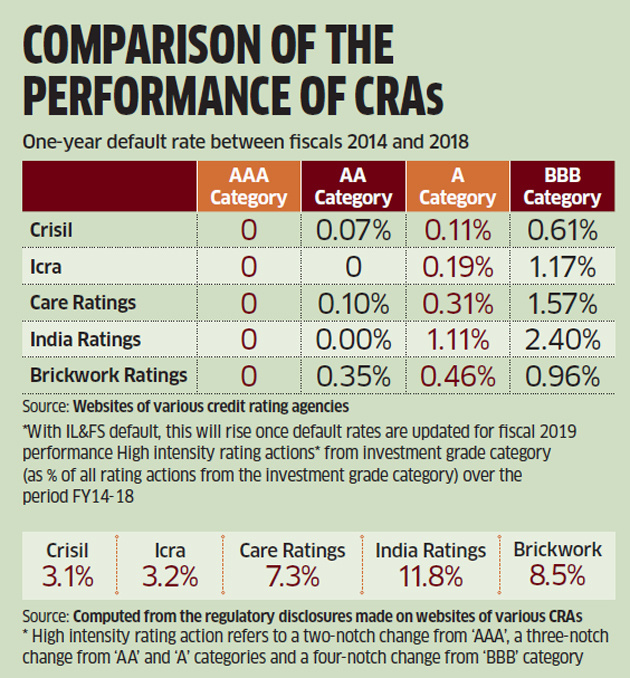

Hence, I find ET latest article on October 2018, (Link enclosed) more useful in that context.

From above data, while we find CRISL and ICRA being relatively better performer on default study, CARE is second followed with India Rating (Fith Rating India subsidiary). While one shall always strive for best and have best rating migration records, but at the same time, on relative scale, CARE appears to be medium (obviously not the best, but also not worst).

Once again, thanks for bringing out a very ciritical aspect about Credit rating business and highlighting CARE Rating weak points in past.

Discl: My view may be biased due to my holding in CARE and investor shall do its own due diligence before investing.

8 Likes

Great points … To add few more points

Quality of business is assessed by shareholders while Product/ service Quality is assessed by customers .

If any company has top end ( quality sensitive ) customers then presumably the product quality is considered good . Say for example Merc / BMW are buying auto ancillaries from a company we can presume that company has better quality controls

So in same context if HDFC bank and Bajaj Finance are using care rating assuming they understand Credit markets well then we can consider CARE Rating is providing good quality @ price acceptable to consumers …

7 Likes

I was reading through Economic Times today morning and came across a news that SEBI is mulling on separating the rating and non-rating businesses of credit rating agencies on the backdrop of IL&FS issue. Some important points that SEBI is going to discuss this week:

- A company has to have get rated from atleast 2 agencies.

- A company cannot get rated for 2 consecutive terms from the same agency (1 term = 3 years)

- Incentive for credit rating agencies (same for all) depending on how their rating turns out to be.

For CARE, almost 98% of it’s business is from rating so it really doesn’t have any major headwinds. Although the second point mentioned above if materialised will lead to long term clients being going into cyclicality. But also a positive point would be that exclusive clients from other agencies will be open to be grabbed by CARE. Let’s see what SEBI decides this week.

2 Likes

2 Likes

This is the link for above…ET article

1 Like

Does anyone have concall notes?

This doesn’t sounds like any bad news for them … Its nothing.

Well i didn’t say this is bad news. But these are some reform measures prescribed by SEBI which should translate into more work for CRAs. Now a natural question is, will this additional work translate into higher fees charged to clients or will just remain a compliance cost for CRAs? Something im pondering upon…

Overall, requirement of multiple ratings should increase the total industry revenue. Last full year revenue for CRISIL+ICRA+CARE is ~1000cr which should increase if multiple ratings become a requirement (although they already exist for CPs). Plus appointment of at least 2 CRAs & a fixed 3 year term opens a market share opportunity for these firms. Also opens up the industry to cartelization/consolidation imo.

Fixed tarriff could be tricky!

Lots happening in this relatively benign space!

1 Like

Some of the concerns regarding care…

2012 sales were 180 cr… Fast forward to 2018 sales is 333cr…in 6 yes times sales is yet to double… Sales cagr less than 12%…

Thing I am more concerned about is the profit growth… Which is going down…

Operating profit margins from 69% in 2012 has come down to 59% this yr… EPs growth is even dismal… 35 rs in 2012 to 50 rs this yr… So in six years it has not even increased by 50%…

On top of it headwinds by actions which are anticipated by sebi…

Are we looking at a business which is transforming from great to moderate…

Only solace is dividend yield… And we do not know what will happen to it if the OPM falls further…

Disc: invested in the recent fall… Wanted to add more… Now having second thoughts…

2 Likes