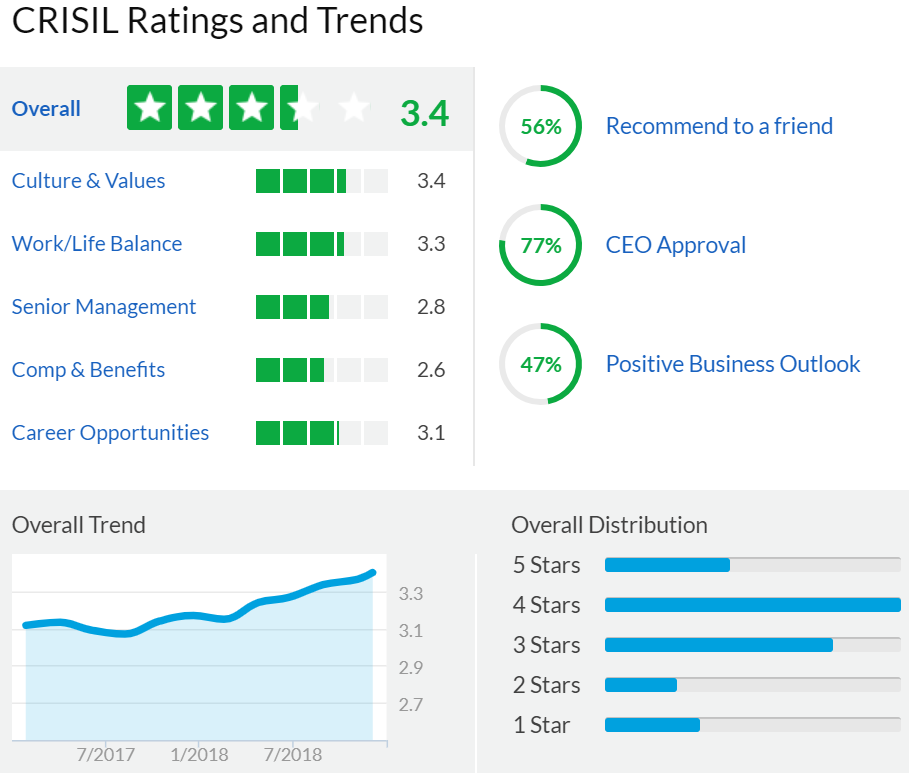

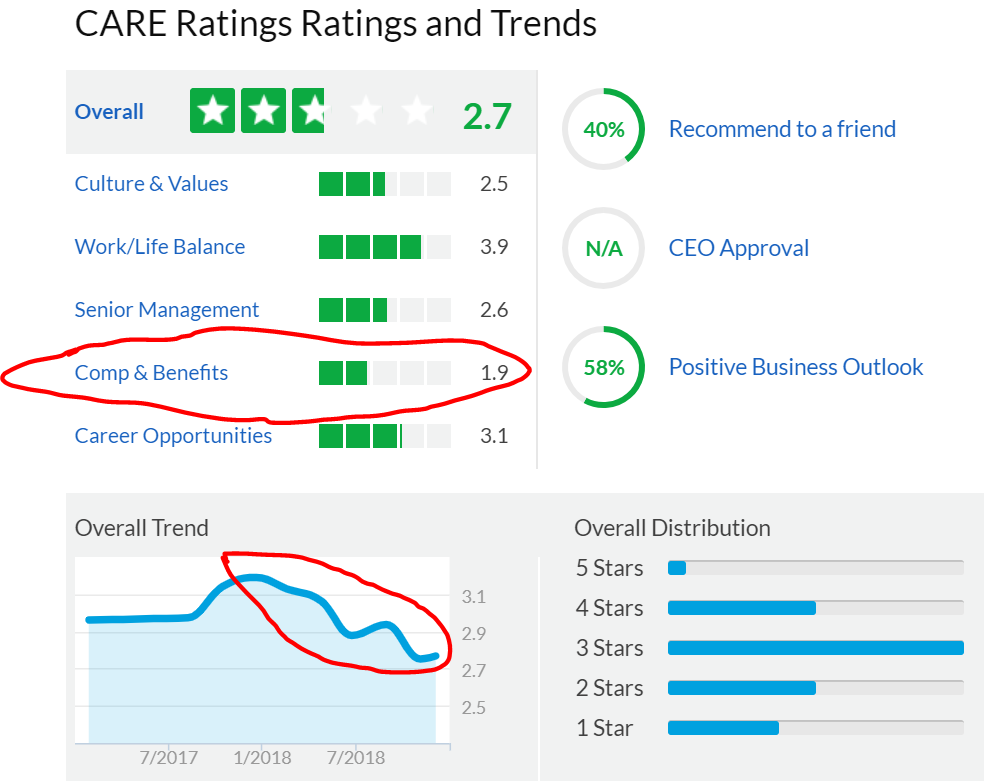

Clearly Care employees are not satisfied with their compensation. Also look at the Glassdoor rating trend. Something seems to have changed since early 2018.

2 Likes

Thanks for sharing good to know information.

But I was thinking as an investor, I won’t be invested in CARE if it treats it’s employees better than it treats it’s investors and customers.

For CARE’s customers, getting rated is purely a cost necessary to be incurred to raise funds. The goal is to raise funds, not to indulge in the quality of analysis done by the CRA. For the bankers hiring a CRA to assess similarly, ratings is a cost.

And as an exercise in financial analysis, ratings is a process based activity, not something which requires a very high level of intellect (compared to say developing a driverless car).

I as an investor would be happy if CARE can hire someone at 6-7 lpa to do the grunt work compared with CRISIL which might pay 8-9 lpa for the same kind of work and thereby either cost more to the customer or accept lower margins.

Just my thoughts… and I don’t want to demean the work done by credit analysts out there…I would be very happy to do that kind of work!

2 Likes

This isn’t exactly logical . Revenue per employee has no element of employee cost in it. CARE might simply be more efficient relative to CRISIL or it might be ‘exploiting’ its employees by forcing a lot of work on a few employees. The glassdoor data you present us with seems to point to the latter. However, I think that most analysts follow a standard procedure while rating companies,so if CARE pays them a lower salary, I don’t think it’s a huge problem.

2 Likes

excellent and logical response by @AKGupta and @IsaacAsimov.

The rating work is entirely process driven and the greater the operational efficiency and margins better we go as an investor.

1 Like

While comparing Salaries have we also factored in the City where these employees are based at ?

I think while Crisil it’s Mumbai whereas for CARE it’s Ahemedabad …so 20-25 percent difference in salary between them ( 9 lpa vs 6 lpa ) is ok and gets nutralized the moment we factor in the cost of living for both these cities.

Pls correct me if my understanding is correct on this.

Disc …Holding and forma 10 percent of my PF

2 Likes

Without second thought, CRISIL is the best play as far as investment in this sector is considered …

And this is reflected in the valuation too … CRISIL enjoy higher valuation as compared to peers.

CARE has better risk reward as of now .

As far as salary etc is considered , I don’t think this has any bearing on investment thesis and more to do with internal organization policies and HR procedures.

1 Like

Does management quality impacts valuation and decision to purchase ?

CARE has no promoter and in India, shareholding activism is unknown … Institutions will be more than happy to sell rather than confront the management in event of any missteps…

CRISIL has a global MNC promoter which was more than willing to purchase extra shares at 1850/- odd levels 6 months back…And may be will also be willing to purchase in future.

Moreover, CRISIL purchased 9% stake in CARE, but if regulators dont allow more purchases and perhaps takeover, that will also find its way into markets.

In my opinion, the valuation gap is going to persist as there is 100% Vs 25% to fight for…

2 Likes

Promoter ???.. I am sorry this is not a valid and logical point.

Please know that unlike its listed competitors, CRISIL and ICRA which have alliances with international rating agencies like S&P and Moody’s, CARE is a professionally managed company with majority shareholding held by leading domestic banks and financial institutions like IDBI Bank, Canara Bank and SBI to name a few.

Coming to second point why don’t we see that most of the investors dig into small caps and microcaps to find value though there are plethora of well discovered and proven names.

So while CRISIL etc may be more visible in terms of brand and valuation and market knows that and discounted that in calculation but we bet into future and risk reward is more favorable in CARE.

Rakesh Jhunjhunwala holds CRISIL.

PPFAS fund hold ICRA.

Mohnish Pabrai holds CARE.

Different perspectives on the same sector… Best luck to everyone.

2 Likes

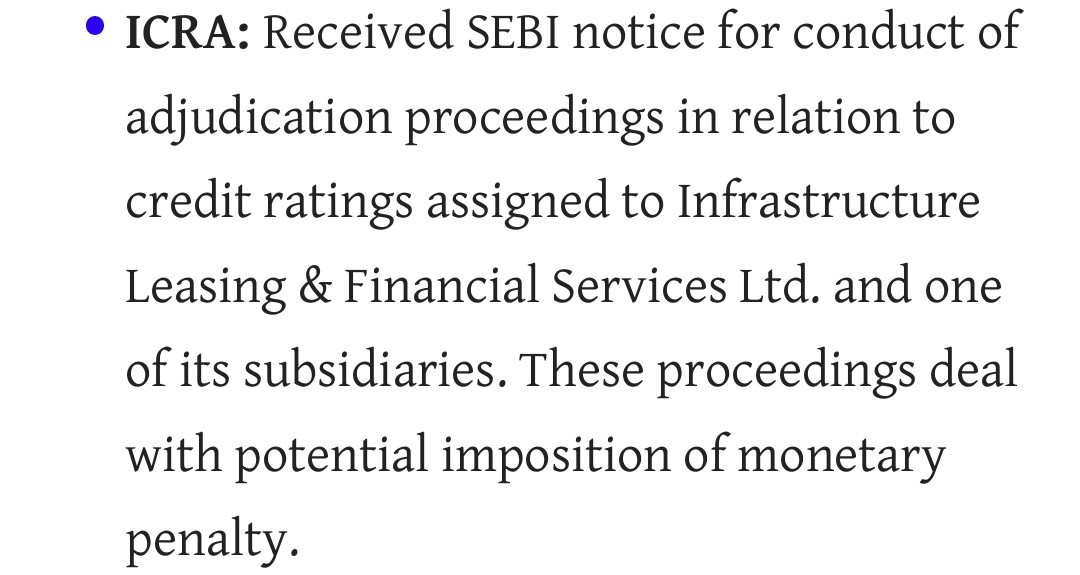

IL&FS Scam: SEBI Starts Adjudication against Credit Rating Agencies.Please go through the article .May effect ICRA, CARE and India Ratings

Kindly take a note. Mohnish Pabrai recently Sold 2.43% of his stake.

3 Likes

In my opinion, with the coming in of a new RBI Governor who is more sympathetic to the cause of the banks, credit growth will off take well from here. Investment cycle is showing signs of revival as well.

The 11 PSBs under PCA might just be freed from the shackles of PCA framework & since CARE derives most of its business from PSBs BLR segment, it should benefit.

Long term I’m counting on deepening of the bond markets in India to benefit CRAs. I was reading an interview of one of the KKR chiefs & he said India has to enable corporates to raise long term debt capital directly from the public to develop its financial system. That will bode well for its Ease of Doing Business ranking…I hope the govt also pays attention!

Here’s the link: https://www.cnbctv18.com/market/stocks/india-needs-a-deep-large-bond-market-says-kkrs-henry-r-kravis-1676651.htm

2 Likes

Adjudication proceedings have been started against CRAs for their role in ILFS. These typically involve monetary penalty…

1 Like

f4559a8d-83f9-4857-87d7-5c1ddd54b699.pdf (74.4 KB)

1 Like

about this i don’t think we should treat CARE as guilty, In credit related businesses you are bound to make mistake.

Also, if in 2009 US credit rating agencies can get away by paying modest fines , i don’t see this IL&FS episode will kill them.

If stock falls -20% tomorrow i’ll be the buyer ( i don’t think it will react ).

3 Likes

Was trying to understand which can be the best bet in CRA space among CARE, CRISIL and ICRA considering recent turmoil…

If i understand correctly, the ratings are usually regulator prescribed and required for easing taking on debt…

Any company will look to these three factors while shopping for ratings…

- Cost

- Ease of obtaining a favorable rating

- Quality / Marketability of rating (A rating from one CRA carries better weightage compared to other and thereby ensuring lower cost of borrowing)

So just looking for the where the CARE excels compared to rest two CRA in terms of these three points ?

In my opinion, pricing and perhaps ease may be favorable points…Third looks doubtful.

If it is just going to compete on pricing and perhaps, ease, can we say it is undervalued compared to rest two or has a lasting moat despite limited competition and high entry barriers?

Posting big investor’s entry/exit is ok but too much emphasis & discussion of their actions is unwanted and it dilutes the quality of discussion. Hope we avoid such non-value posts.

7 Likes

As per your study which CRA excels in third point ?? Operating margins are highest for CARE

If i were to draw a parallel to this discussion with other similar incidents then it would be the Wells Fargo Incident.And here is what Buffet had to say about it and how he acted on it.

As I discussed earlier, I wanted to share some analysis related to CARE’s ESOP scheme and its overall importance in the total employee related expenses.

So here it goes…

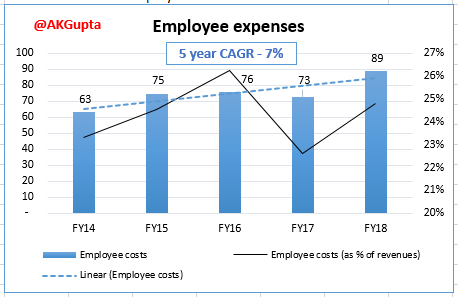

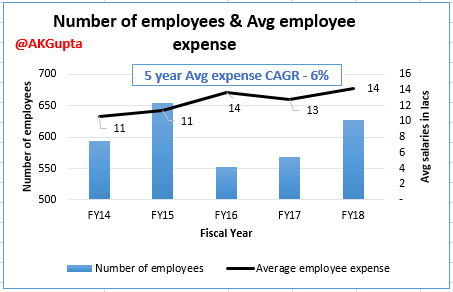

Looking at the total Employees related expenses for CARE over the last 5 years, the following picture emerges:

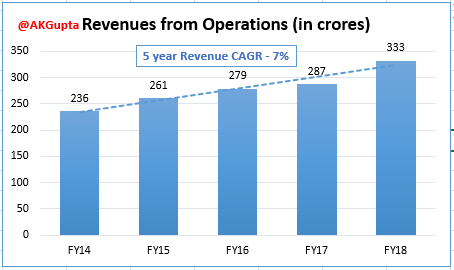

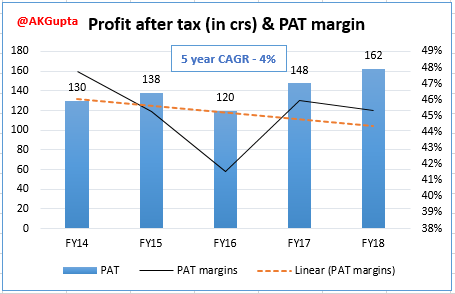

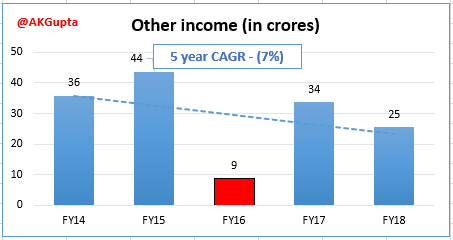

As we can see this expense is growing at a 7% CAGR which is pretty high (in fact this is equal to the Operating Revenue CAGR of 7% witnessed over the same time period). But this is not impacting my PAT CAGR (which is at 4%) which is the story of “Other income” declining substantially over the last 5 years (CAGR of -7%).

But focussing on the employees expense again…

Notice in the below chart how even though the number of employees have not been growing, the average expense for the employees is steadily increasing between FY14 & FY18:

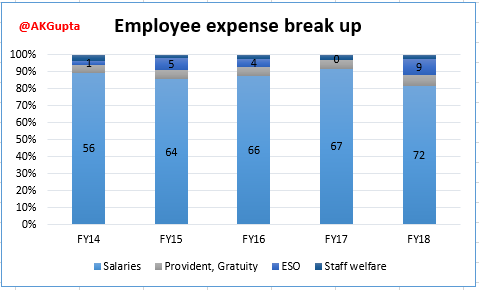

The break up of Total employees expense is presented below:

While the basic Salaries & Allowances are the major component driving employee expense growth, ESOPs are a contributor as well.

I noticed in the AR FY18, CARE has granted additional 538K options at an exercise price of Rs 1139/share. Thus the total outstanding liability for stock options on CARE’s books is 524K. Break up is as below:

How this works, in brief, is when the options are granted, a liability is created on the Balance Sheet for the difference between exercise price and fair value (calculated using Black Schols formula) of the options and correspondingly an expense is created. As the vesting period is 2 years, CARE amortises this liability over 2 years (as stated in Notes to Financial Statements).

This amortised expense net of options lapsed during the year (we are netting off lapsed options because they are reversed from the Balance Sheet liability for ESOs), is what we see in the P&L (roughly 9 crores for FY18).

Note that the actual exercise of the options won’t have an impact on the P&L but only on equity outstanding.

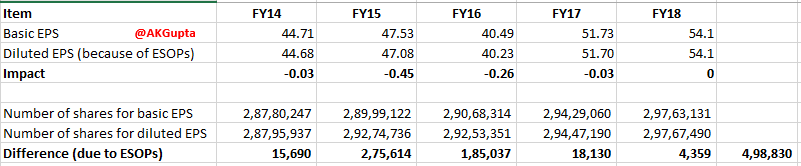

Thus ESOPs impact us shareholders in 2 ways - firstly it reduces P&L by the difference between exercise price and fair value of these options, and secondly it increases the equity base (number of shares outstanding) and thus reduces EPS. (Note that this liability

can also be settled using cash payments to employees but CARE opts for equity settlement). Note the trend of basic and diluted consolidated EPS as shared below:

In my opinion, the quantum of ESOPs is not a major worry if it properly incentivises the mgmt to perform to boost earnings and aligns mgmt interest with shareholder interests.

Disclosure: Invested in CARE. All above numbers are taken from ARs.

10 Likes

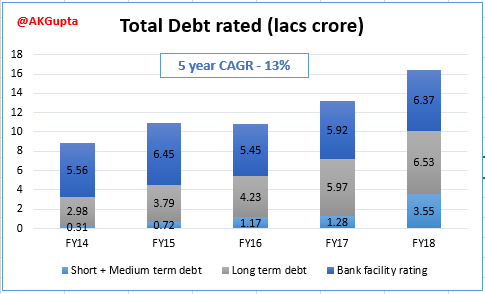

Some more thoughts that I wanted to share on CARE’s P&L:

CARE is focusing on winning as much business as it can, growing volumes of debt rated at twice the CAGR of operating revenues. This could also mean CARE is winning market share by underpricing its services vs competitors:

The above chart also shows how CARE is trying to reduce its reliance on Bank loan ratings by rating more short term (CPs) and long term (bonds) debt. Combined with efforts to diversify internationally, this bodes well for investors.

Do note in the next chart that:

- PAT is growing at a meagre 4% CAGR for last five years, and

- Margins are also declining steadily

This is because of paltry other income (maybe CARE should just hand over the Balance Sheet cash, roughly 500 crores, to investors & focus on core business!!!):

This paltry growth is however, in an environment of subdued credit growth in the economy where half the public sector banks have been handcuffed by RBI & other half are trying to recover bas assets in NCLT. Plus, several big companies are not borrowing before elections related uncertainty is over. If credit offtake/investment activity improves, it should bring back growth to CARE as well.

I was watching Kenneth Andrade’s interview on BQ in which he said capacity utilisation has reached to a level where fresh capex should get triggered. Nobody can time it exactly though!

13 Likes