My below post is not specific to CARE, but overall Indian rating industry in general. Sorry, I decided to post it here as I believe it will help everyone understand the ongoing industry dynamics since CARE is very much part of it. And also sorry for the long post.

I have always had questions on inability of Indian rating businesses to grow at decent rate which has kept me away from investing in them. End of the day, if there is no growth in equity, it will be treated like bond. Bharat Shah has nicely said that “When growth goes away, Equities reduce to a Bond. It will be Treated like a Bond for a while. If the Picture Deteriorates Further, then it will be Treated Worse than a Bond.”

In a growing country like India where you have decent number of great compounding growth businesses, I don’t understand why would one want to buy a business at 40+ PE where earnings are growing at meager 6-7%. This has been the case with all rating businesses in India in last 5-6 years. All of them were available at north of 35-40PE most of the time with earnings not growing more than 7-8%.

It is a great moated business which generates excellent ROE, throws tremendous cash flows and dividends. Just 3 players capturing 95% of the market. I believe most of us will agree that it is a great business.

If US rating agencies survived 2008 debacle, what’s happening in India is nothing compared to it. So one can have reasonable confidence in its longevity.

I believe Warren has been holding Moody’s in his Berkshire portfolio for last 30+ years. And now Berkshire would be getting 20%+ return on their initial investment as annual dividends.

My understanding is that business of rating agencies should grow at some function of growth in your debt market and underlying economy. At a high level - Moody’s revenue have grown from $349mn to $4.2bn in last 21 years at CAGR of 13% which is much faster than underlying economy growth rate of the US. This growth rate has been achieved despite of dot-com crash and 2008 financial crisis.

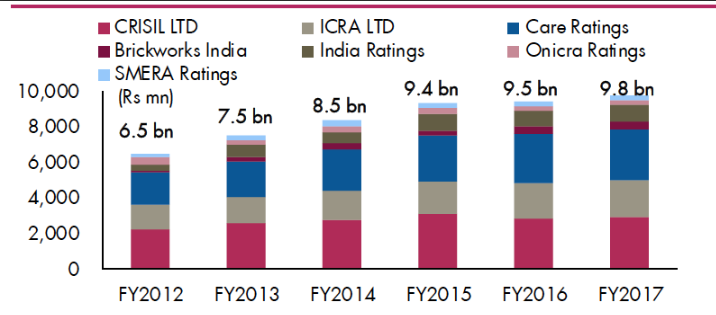

Per @AmitContrarian’s below screenshot it looks like top-line for all players have grown at CAGR of 8.56% from 2012 to 2017.

CARE’s revenue has grown at CAGR of 8.11% between FY11 to FY19. CARE’s growth is inline with the industry growth rate. But underlying nominal economy has grown at much faster rate. It is short period but still things have been flat.

With this backdrop few questions that I have are:

-

Is this slow growth rate in Indian rating businesses because debt markets in India are not well structured yet?

-

What is that structural hindrance that is causing slower growth rate for all players compared to economy growth rate? (especially in last 5-6 years)

I apologize if these items have already been covered in their Annual Reports. I admit that I have not looked beyond CARE’s AR and have not done a deep dive to find out answer for above questions. Any help with understanding above questions will be much appreciated.

Thanks,

Amit R.