okay just saw that’s the R&D expense in capital equipment …

high receivables are because of their business model, they are manufacturer, exporter and seller, their is no middle man in it that’s why high OPM also.

As far as i know management is good

1 Like

Company optically looks good, but still trades at cheap valuation. Despite, low leverage, good profit history, growing sales, low management remuneration, strong management control, healthy margins, solid return ratios and more, mutual funds are reluctant to invest in the script.

Reason: The company operates largely in unregulated segments. To my understanding, such fragile business models always runs a risk of regulatory intervention down the line, resulting in investment distancing by institutional investors.

To tide over this risk, business managements always need to be transparent and prudent in operations.

Although, in extreme bull runs, as quality takes back seat and momentum takes over, such stocks could show intermediate spells of large price movements but with sustainability under question.

Other key examples in this perspective are second-quality real estate and NBFC players including micro-finance, GFCs, HFCs etc.

8 Likes

thanks @Likeadiamond for your great insights and without undermining any of your points, wondering if operating in Latin America and African markets is a tactical play by the firm keeping itself immune from FDA approvals unlike some of the other Pharma majors. The stock has been a multibagger, and has gone down with other small caps since late 2017

Hi,

Thanks for your query.

Genreally, such endeavours are strategic in nature as businesses try to explore untapped markets and reap benefits as much possible until maturity. Before entering any market, managements do complete due dilligence including feasibility studies, competitor analysis, understanding market size etc.

During intial phases of operations, companies remain successful in achieving higher growth rates, however, what looks advantageous upfront turns disadvantage later as such high growth trajectory doesn’t last for long, pushing businesses to scout for new geographies.

Stock prices are a blend of rational and emotional layering over fundamentals. Past stock performance was mostly on account of low base effect and higher profit and sales growth. On a higher base, such growth rates are difficult to sustain, leading to correction in PE multiples.

Mr. Market give a higher multiple to a marathoner than a sprinter.

All the best in your investment journey.

6 Likes

Hi - thank you so much, these are incredible insights and there is so much to learn from your post. Much appreciated you taking out the time and helping explain in such fine detail. And your point around scouting for new geographies is clearly visible in the latest balance sheet. Thanks so much again, and wish you all the best as well in all that you do.

1 Like

Question: I would have lost money if I invested any time during the last three years despite great numbers, as a noob what would I be missing, why has the shares fallen so much?

My findings: PE dropped from 55 in July17 to 11 now, despite great numbers

3 year sales growth 30%

3 year profit growth 56%

3 year roce is 57%

change in promoters holding is -0.03%

company is debt free & 0% pledging

Last 3 years margins are also bound in 31-36 % range.

What am I missing here?

My Background: Last month I woke up, until then I was like a sleeper cell agent, JK ![]() . I have been waiting for this market crash since the last 2 years. Last month I invested heavily in several sectors, but still I haven’t found my drug, that shall take me to new highs(pun intended!)

. I have been waiting for this market crash since the last 2 years. Last month I invested heavily in several sectors, but still I haven’t found my drug, that shall take me to new highs(pun intended!)

I came across Caplin & got interesting insights via screener.

I have started reading this whole thread it shall take me time to go through all.

Trying to find the best pharma that fits my portfolio. Suggestions would be appreciated!

3 Likes

After 2 hours I read everything after 2016, hmmm!

Few issues with Caplin

- High AR days.

- Entry to China

- Long bet into the much regulated US markets

Comments:

- Management did say there hasn’t been any defaults yet & that contributions increased on account of entry to new markets which are more profitable albeit longer credit cycle.

- One thing that everyone missed & as you can recall this was one of the main reason for Asian Paints success (Optimizing their supply chain).

At two placed above in the thread this things has been mentioned, read details.

The company is partnering a unique software development provider to design an unprecedented business automation service for the benefit of pharmacists.

By providing a service completely free to more than 3000 pharmacists across the Latin American markets

This service will achieve something far-reaching for Caplin Point.

An understanding of lifestyle disease trends, an understanding of which districts suffer an incidence of what disease.

A knowledge of evolving disease profiles and an insight into the prescription.

Questions:

- Now I highly doubt their claim of more profitability since the OPM has decreased from 36-> 32(source screener TTM OPM).

- What is OPM in Chinese market?

- US investment has not paid up yet, right?

- Whats the update on that business process automation?

Disclosure: Not invested

1 Like

@sham72942

Didn’t want to crowd Hitesh ji’s thread, so replying here.

The allegations made in 2013 were “allegations” & not much financial inadequacies. It was a well performing company even in that time. Request you to go through those posts since you’ve read only after 2016, as you mentioned.

I agree that financials have improved much since 2013. And, that aroused my interest but so far stayed away from it.

One thing that intrigues me is that Marcellus has invested in Caplin point in the smallcap portfolio. I know Mr Mukherjea stresses on the hygiene of B/S in every interview and he takes management track record seriously. On the other hand, I’ve discussed about this company with several experienced investors outside VP and most of them warned me to stay away from this company for one mischief or the other (mostly financial shenanigans). My risk appetite doesn’t allow me to invest in this counter coz I’m somebody who considers management standards and financial reporting sacrosanct. Would be interested to know from experienced boarders on why one should avoid this stock given the valuations and the recent growth trajectory. What is it that the markets/experienced hands know that we don’t know? That would clear the air for New comers like me.

PS: No current holdings

5 Likes

I see @atulastra has been a shareholder for the last 15-20 years, could you please give few minutes to the query of new comers like me, especially at the process automation part

financial shenanigans like what? please elaborate?

2 Likes

Caplin Point Unit Gets US FDA Nod For Phenylephrine Hydrochloride Injection

Phenylephrine Hydrochloride injection is indicated for the treatment of clinically important hypotension resulting primarily from vasodilation in the setting of anesthesia.

2 Likes

Does anyone know more on what implications this would have for the company, how would it impact the topline, bottomline - market seems to be cheering this development in a big way…

Caplin Point is one of the companies in Marcellus Little Champions portfolio. That got me excited in teh stock

Invested as this ticks the boxes for me on P/E, ROCE, Sales Growth, Profit Growth, Promoter Honesty and Moat (in South America business). Bought 300 shares at 330, went up to 421 and now back to 380!

One bummer today is that the latest quarter results show a 28% decline. Will check transcript in detail if this is one off or systemic

6 Likes

To add to @rkirana’s points with some headwinds the company faces:

- Looking backward, a lot of their revenues/sales came from LatAm where they were the sole providers and hence were able to maintain high margins and ROEs. Going forward, since they are doing CapEx to provide sales in US, the part of the pie which comes from US will rise, ROICs might go down, regulatory oversight will increase.

- Going through the quarterly and annual results declared today, the trade receivables have jumped from 34cr last FY to 230 cr this FY, meaning the Operating cash flows have reduced from 84cr to 45cr.

Disc: Roughly 10% of equity direct stocks PF (second largest holding), plan to add more in coming days if and when it falls close to 300 rupees.

3 Likes

Thanks. 300 is almost 20-25% down from here. If that is the case, one could as well sell now and buy lower!

2 Likes

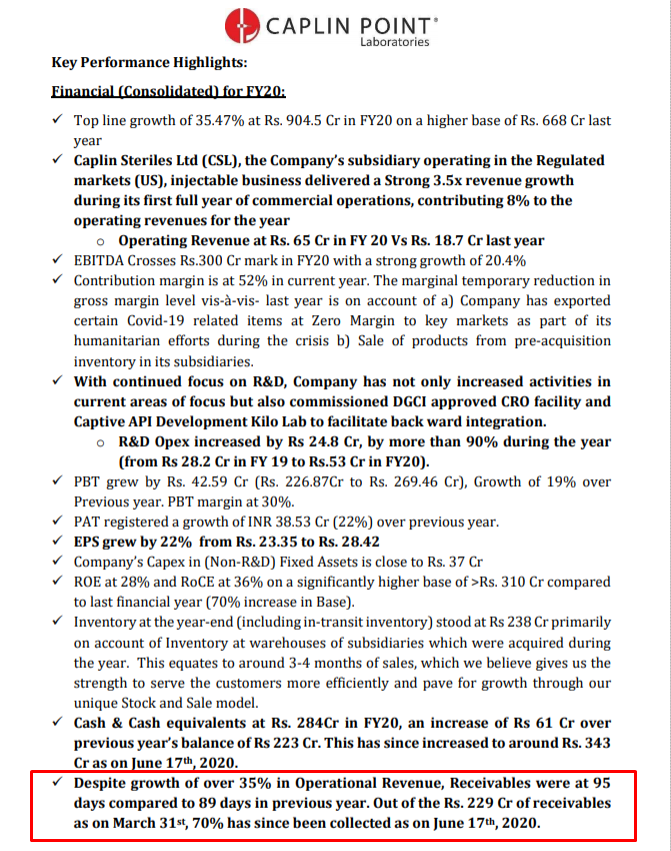

Yes there is a jump in companie’s receivables which looks bad on prima facie, but company has mentioned below in the highlights that out of 229 cr receivables 160cr receivables(70% approx )have been collected, till date ie june 17th, which looks quite good to me. Results look positive

4 Likes

On the con-call that’s underway right now, the chairman also said that they’ve been able to generate a cashflow of ~75 Cr just in the last 7 days with their cash and cash equivalents increasing by that number.

Thanks for adding, I’m on the concall as well. I would suggest/request for us to wait for a transcript to be published. From what i could hear it was not 7 but 70 days (I could be wrong though since the volume is quite low).