Company finally disclosed that they have received the approval from USFDA for one the plants. Annual results are also due tomorrow. Hopefully shareholders will finally have some good time.

Companies who give ESOP are found to make best use of their resources. I feel it’s good that Indian companies are taking steps in that direction, very few Indian companies do. There are various researches why giving a small amout of EPOS gives lot more motivation to the employees that small amount of hike. Most of employees are not familiar with stock market and since they track only stock ie of their company they find it more motivating to see it go up and put in more effort. In short term it may dilute the equity marginally but in long run it will boost the companies output. For me it seems to be a sign of advanced and forward thinking management.

1 Like

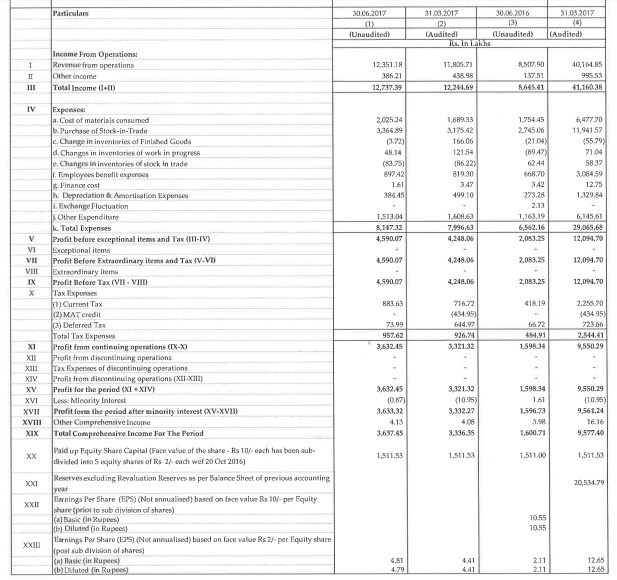

So - yea the results were great… looking forward for the same growth.

Could someone shed more lights on EIR recently received from USFDA.EIR is a report post the USFDA observation given in october.Does that mean its a US FDA or to say - they can sell in US market.If yes it was for which facility and what was approved to be sold in USA.What are their future plans.I could not find anything about all this on bse updates except the note from company about EIR.

Disc. Innvested at low levels.

I’ve been adding Caplin Point in tranches over the past 2 years at different levels, but with the company now trading at ~55x TTM, I’m wondering if it’s wise to partially exit and look at re-entering the stock at more reasonable valuations.

It’s hard to put a definite exit multiple for companies like Caplin that consistently have such high growth because if they continue to grow at the scorching pace that they have been growing at for the past few years (50%+ CAGR), their PE multiple could easily be 35x at the end of the year which is really when their growth begins to catapult (2018 onwards with the entry into the US).

I would like to stay invested in the company, but as they say, every company has a price and once it goes beyond a certain price point, it’s wise to exit and re-enter at more reasonable levels. On the other hand, it could turn out to be like Symphony, where the company is constantly “overpriced” with high multiples due to the steady stratospheric growth in the company, thereby not coming back down to cheaper levels and valuations.

Would like to invite the views of other members on how they deal with this conundrum of whether to exit or just hold through the price fluctuation and watch the company grow while the stock price could possibly not move for long periods because of the sky-high valuation it has currently.

Edit:

Apologies, I looked at the standalone numbers and not the consolidated numbers. It’s currently trading at 42x TTM.

1 Like

High PE can sustain for a decade if market has clear visibility of earnings and growth.

This is something which is beginning to worry me now, every time the company is posting steller results but the management is not as transparent as I would have liked.

Worth digging deep on the concerns raised by @atulastra

Hope this doesn’t turn out to be one of those too good to be true stories.

Disc: Holding from lower levels.

1 Like

First thing first, PE of the company is not 55x as the last year consolidated eps is 12.72. So, for the share price to trade at 55x the price needs to reach ~700 levels.

Corporate governance is an issue in India forget about this small company, do all of you recall Satyam or more recently all private sector banks under reporting NPA’s?

For me following are the key points to look forward to:

– EIR already in and 2 ANDA’s are filled, 7 more will be filled till Dec 17. I wish they get approval or rejection quickly for them. They are highly likely to get approvals as they have partnered with some big players, those big players won’t let their name get wasted so will keep a deep quality check on all counts. Based on the outcome the company can start supplying to USA in FY 2018.

– Company has set up 2 subsidiaries and I think all expenses they have already written off wrt setting of these subsidiaries. So, at best they are under reporting the profits.

– They are entering 3 new markets this year Colombia (already have approval from thr local authority), Chile and Paraguay and this does not include Brazil or European market, where they already have approved their production facility and now the company has submitted some products for approval. Brazil, they have submitted application for 4 approvals (from company website). European Union has approved their injectible plant.

– Every country they are present, they are applying for new formulations and approvals. 300 approvals this year to 2300 products another 350 are due in next 11 months.

– Only 2 things are real in results: Taxes and dividend both of them are increasing every year.

– Management guidance of 25-30% I am hearing this for past many years, they believe in under commitment and over delivery. Their sales are growing @30% and profit @64%, since 2011.

Markets have decently rewarded the stock price since 2011. ROE is one of the highest in the industry.

All in all a good long-term bet for risk seekers. I am expecting this to be 4-5x in next 4-5 years. No valuation is over or under it’s all about sentiments and ofcourse the results which are fab for the company.

Disc: Invested from very low levels; views are biased.

Addition: Company plans another plant at Puducherry from internal accruals again no loans.

5 Likes

I agree - Why is the management not transparent.I am not even in terms of naming your clients and all but atleast give a small breakup of your growth and i.e. my biggest concern.

@atulastra - Could you share citation or official release for above information regarding the above plans you shared.

And also how can you say that the expenses have been written off - I am asking this as they already debt free soo dosent matter otherwise too but if it just to stay clean this way - its a red alert but again I am just asking as I am not too sure about this.YOu even say only taxes and dividend are real - so my point is if sheet is cooked up would they be able to pay these. Just asking not too sure.

Nothing is my imagination, kindly check latest press release, company website and annual report.

About amount written off, they have shown some loss from associates, I assume that company has written off the amount. They are normally very conservative in their estimates.

Disc: Holding shares and biased views

1 Like

My personal thoughts is to have some skin in the game (never consider a full exit as market may choose not to correct). This company has the potential to deliver 30+% CAGR for the next 5-7 years. Their moat is their trading business routed via Pharmacies (as we are all aware) & without incurring debt , they have managed to line up CR I/ II & III to be called a Pharma company. I believe that USFDA could add substantially to the bottom line & what we are seeing now is market pricing in the next 2-3 years growth. Also being a low floating stock , the moves are exaggerated. Since there are more talented members who can comment on fundamentals & I have nothing new to present , my take from technicals is that this 3rd wave of some degree targeting 700 with first line of resistance at 550. If it is unable to break 550 , then it heads down to 480 & from there could resume the uptrend. My view is that we are going to break 550 & push ahead.I have no exposure & dont intend to take

3 Likes

What’t the sudden spike of nearly 150 rs in one weeks time is about? Really appreciate if someone can throw some light on latest development if any.

1 Like

Yes. The Caplin point labs stock price zoomed to around +28% in last 5 trading days. Is there any positive news that we should know?

Evaluating Current Stock Valuation:

Hi,

I seek some opinion on the pricing of this stock.

The results for latest quarter (FQ1 FY18). EPS 4.81 vs 2.11 for same quarter last year i.e. 2.27x. Assuming same ratio on annual basis EPS for FY18 will be ~28. Even if we take industry PE of 29 (in this case it should be much higher), price is ~ 812. Would it be fair to assume that the stock is still not over valued?

It would be great of someone can help me evaluate this.

Best regards,

Mayank

2 Likes

Awesome set of Q12018 numbers but I missed the press release from the company. Press release gives much more details.

Following are the points covering few hits and miss:

– Company fails to make in Forbes Asia 200 under billion list (personally I am surprised)

– Company has now 2400 registrations around the world and 300 pending approvals

– Brazil they have 7 registrations and 3 submitted I think last 2 qtrs they are making sales to Brazil but yet to get the confirmation.

– US 3 ANDA’s filed and 28 pending… this was a small number, 28 is certainly a surprise.

Eagerly awaiting Annual report for FY 2016-17.

Disc: Vested interest and biased views.

Hi Mayank, I am guessing your EPS estimate is a bit on the agressive side. Caplin has done an EPS of 4 for Q1-2018. A simple extrapolation would give us 16-18 as EPS. Currently it is trading at a PE of under 40. Companies growing at above 30 CAGR would generally quote at higher PE. At this point Caplin seems to be adequately valued according to me.

I would add Caplin if I get it around 30-32 PE on forward earnings.

Disc: invested.

Hi Atul,

I am not able to locate the Press Release post the Q1 results. Where can I find it?

Thanks

Dear Nithin,

Thanks for the note. I agree that the EPS estimate is slightly aggressive. Can you please help me understand your estimate of 16-18 EPS?

Q1FY18 results, reflect (consolidated) q-o-q change from $2.21 in Q1FY17 to $4.81 Q1FY18. Also, their TTM is ~15.5 implying a PE of 44. Is there something I am missing?

Disc: Invested.

Thanks and best regards,

Mayank

Lot of people are asking for press release. I don’t have any infact thats what i said “I missed the press release from the company”… All information taken from company website. Please browse through and add any information missed by me .

My takeaways from Annual report 2016-17:

- The company is partnering a unique software development provider to design an unprecedented business automation service for the benefit of pharmacists:

1.1 By providing a service completely free to more than 3000 pharmacists across the Latin American markets;

1.2 this service will achieve something far-reaching for Caplin Point.

1.2.1 an understanding of lifestyle disease trends, an understanding of which districts suffer an incidence of what disease,

1.2.2 a knowledge of evolving disease profiles and an insight into the prescription.

-

Caplin Point possess an organisational structure that is attractively placed to widen its global footprint. It started a new range of OTC and wellness products manufactured out of China, which were exported through its HK subsidiary. It’s new range of pharmacy-related products has also been launched through the HK subsidiary. Since China has Free Trade Agreements with several Latin American countries, trading options out of HK are more attractive compared to India for specific products. The HK subsidiary also serves as an attractive option for probable acquisitions as it represents a more favourable environment.

-

The company initially planned to file 4 ANDAs with partners, of which three have already been filed, strengthening preparedness to file 6 more ANDAs in the next 12 months. The company plans to add 30 more ANDAs in the next 30-36 months (under Caplin’s name).

-

The company is engaged in the long-term research of Liposomal formulations.

-

The company is planning to activate Phase 2 of CP-IV, empowering it to handle a large capacity of Lyophilized products and complex injectables (likely to be completed by end 2019)

-

The company made timely investments in this direction; it is in the process of building capacities to handle pre-filled syringes and cartridges, likely to go on stream within the next 12 months.

-

the company is required to meet an annual operating cost of INR60 cr till 2019 when the shipment for US starts.

-

Caplin performance ambition:

8.1 Financial ambition: Match revenues in 2016-17 with PAT in 2021- 22; earn a sizeable share of revenues from regulated markets.

8.2 Intellectual ambition: Transform employees into shareholders, undertake cutting-edge R&D to address the unmet needs of regulated and unregulated markets; file more proprietary and collaborative ANDAs.

8.3 Geographic ambition: Consolidate presence in large and fast-growing markets like the US, Brazil, Colombia and Chile among others.

8.4 Therapeutic ambition: Focus on niche injectables in the US by extending to the manufacture of specialty suspensions and PFS products.

8.5 Logistical ambition: Evolve identity from being a distributor led player to one which is directly engaged with retailers across Latin America.

- Priorities for the Latin American and Caribbean markets:

9.1 Larger shelf share and wider coverage of pharmacists

9.2 Stronger focus on direct pharmacist engagements (better margins)

9.3 Next market expansion likely to come from digital interventions

9.4 Increase in share of organizational revenues from pharmacists from 20% to 30%

9.5 Extension from pharma to complementary wellness products Deeper inroads into the tender market

Disc: All information from Annual report 2016-17; None of the above is my interpretation; Vested interest and biased views.

8 Likes

I just extrapolated the current qtr consolidated EPS to 4 qtr which would work to 16+ I am hoping they do more than that.

Cycle Pharmaceuticals says U.S. Food and Drug Administration approves Abbreviated New Drug Application for Ketorolac Tromethamine Injection 30mg/mL.

Cycle says Ketorolac developed with Caplin Point Laboratories

Ketorolac indicated for short-term, or up to 5 days in adults, management of moderately severe acute pain requiring analgesia at opioid level

Ketorolac being made at Caplin Point’s FDA-approved site

Cycle names Virtus Pharmaceuticals, LLC as Ketorolac importer, distributor in U.S.

3 Likes