great results by capital first as usual

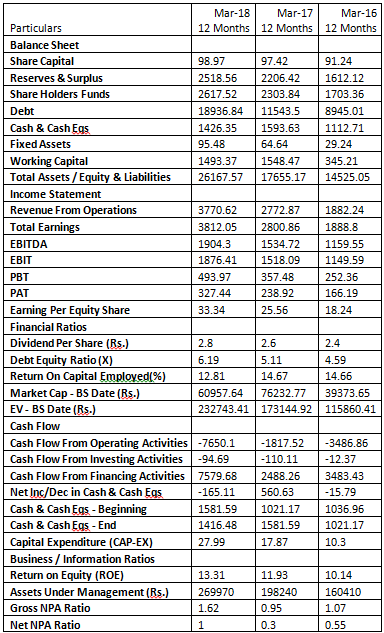

total income increased to 1055 cr vs 769.11 cr ( 37% yoy growth)

PBT increased to 159 cr vs 96 cr ( 65 % yoy growth )

PAT increased to 101 cr vs 65 cr ( 55 % yoy growth )

Asset quality slightly improved

The Gross and Net NPA of the Company as per existing RBI guidelines are 1.57% and 1.00% respectively as of 30 June 2018 as compared to Gross and Net NPA of 1.72% and 1.04% respectively as of 30 June 2017.

6 Likes

Y is the companys P/E so low as compared to industry…also is the 139 IDFC bank shares for 10 shares in capital first capping the upside?

That’s exactly right, now one is buying IDFC bank and not Capital first as merger is impending.

The real challenge lies in integration. There are cultural issues. How Vaidyananthan is able to take along an otherwise slow organisation along with his CF ,that remains to be seen. If that happens , real benefits would be visible in 3/4 years.

1 Like

Ind AS accounting standard slightly increases the book value per share (288/-)

Investor presentation https://www.bseindia.com/xml-data/corpfiling/AttachHis/1b618cc6-285e-429a-b3f7-7b341b1971f3.pdf

Investor meets this month: https://www.bseindia.com/xml-data/corpfiling/AttachLive/5a8d5d27-7164-4cc8-867f-eaa7d27c32e1.pdf

Kindly share your thoughts on the below. Apologies if any of my questions are irrelevant/repetitive.

-

Since the swap ratio is 139:10, what happens if I have only 1 share of CapitalFirst? Mathematically, I should get 13.9 shares, but how do they account for fractional holding of 0.9 ?

-

Price has corrected by almost 50% from highs. Can some with technical analysis skills look at the chart of either CapFirst or IDFC Bank and share if there is scope for further correction ? Or the cleanup is done and things can only get better from here (hopefully) ?

-

Given that most NBFC’s are getting thrashed due to questions on incremental capital availability/cost of capital, CapitalFirst’s merger with IDFC Bank gives it access to low cost CASA deposits. In that sense, it may be better off than many pure-play NBFC’s - in a small way atleast. Is this a valid argument?

-

When is the merger expected to be consummated? Can someone throw light on the expected EPS, Book Value for IDFC Bank post-merger ? Along with calculation logic if possible.

2 Likes

Capital First:

Company has transformed after management buyout led by Mr. Vaidyanathan with backing from PE firm Warburg Pincus. Mr. Vaidyanathan able to transform its loan booked from wholesale lending to retail lending. With the average AUM growth of more than 30% pa, he manages to increase the stake of retail portfolio from 28% in FY11 to 94% in FY18 with the NPLs under control. This story is again expected to repeat after the merger of IDFC bank and CapF which is again expected to be led by Mr. Vaidyanathan.

CAFL’s strength lies in scaling up retail financing businesses including mortgage, home loans, SME loans, auto loans and consumer durable loans. Bank platform will add to its strength.

Capital First AUM Breakup:

Of the Rs 300bn AUM, about Rs 110bn(36%) is secured MSME / LAP, about Rs 50bn(16%) is unsecured MSME, consumer durables book is about Rs 40bn(13%), 2 wheeler book is about Rs 30bn(10%), home loans is about Rs 20bn(7%) and the rest is used car book and others.

Consumer durables business Rs 40bn (13% of AUM) – Range from Rs 30,000 to Rs 3,00,000 without asking for financials. This is also extended to mobile phones and high end watches.

This segment is largely acquired by 2 players, Bajaj finance (70% market share) and Capital first (25% market share). Remaining (5% market share) is HBD Financial and L&T financial.

Customer count is ~2mn of which ~40% are repeat customers and Capf has served ~25mn customers till now in this segment. This makes their database much richer and its analytical outcomes are expected to improve its performance in future.

This segment generally takes around 3-4 years to breakeven which was just turned positive and managed to clock ~13% ROE. Management guided for 25% ROE in this segment suggesting treamendous improvement in this segment.

For consumer durable market as a whole, about 15-20% buy through loan/EMI card, 35-40% through credit card and the rest is through cash. This shows a lot of penetration upside remains.

2 Wheeler business- Rs 30bn (10% of AUM): This is the high ROE business with ROE of ~18-20%. ~60% business is fetch through digital platform while remaining is through Honda most of which are from non-geared bike customers.

Home loan – Rs 20bn (7% of AUM): 60% of this is to self-employed customers which is witnessing a trend shift in to salaried customers. This is currently in investment phase and has capacity to clock 15% ROE.

Overall business strategy : For relatively new business of used car, home loan and micro enterprise lending, CFL has incurred PAT loss of about Rs 120-130mn. Excluding this, overall ROE would have been ~19% which is nearly equivalent to its biggest competitor.

Rationale for merger deal with IDFC Bank:

- It is understood that banks and NBFCs had complimentary clientele. Banks focused on corporate, SME, and retail clients being regular salaried, larger ricket size , lower opex ratio and located in metro/tier 1 centres. NBFCs tended to cater more to those who were under-served by banks. However, in search of long-term growth on a risk-adjusted basis, banks are increasingly attracted to the traditional NBFC client base and NBFCs are sensing this increased competition. NBFCs realize that it may be a matter of time that banks build the required reach and then the latter’s cost of funds advantage may kick in. Hence, the desire to sit inside a bank via the merger and access low-cost funding. This is the primary broad rationale from CFL’s perspective.

- It is to be noted that IDFC Bank is currently not retailised even on the liability side as CASA ratio is just 8.2%. However, IDFC Bank, post-merger, will be able to access CFL’s retail client base of 5mn customers and build the required CASA franchise rapidly, if post-merger implementation proceeds desirably.

- CFL has a cumulative retail client base of 5mn, which IDFC Bank will tap to sell, potentially, the entire gamut of retail loan products. As discussed above, IDFC Bank will also tap this client base to push liability products, particularly CASA. There could be good traction for current accounts given that CFL is significantly MSME-focused.

- CFL has been a robust adopter of technology and analytics and IDFC Bank will gain these capabilities after the merger. This is something IDFC Bank has explicitly stated in its BSE release on the planned merger. CFL has effectively used analytics for sourcing and credit appraisal of consumer durable loans, two-wheeler loans and personal loans and this has helped control credit costs compared with its own past.

- With the merger, both the entities will leverage their network considering the strong reach in North and west of capital first while maximum branches of IDFC bank being in Centre (MP) and south (Karnataka).

Share holding pattern of merged entity:

· Assuming 100% of CFL is being merged and IDFC Limited or affiliates already do not own any stake in CFL, IDFC’s stake in the combined entity will fall to 37.6%. IDFC currently owns 52.8% in IDFC Bank.

· When IDFC Limited had applied for a universal bank license and obtained one from the RBI, the latter had stipulated that IDFC cannot bring down its stake in IDFC Bank below 40% for the next five years. This could be the challenge faced in IDFC bank and CapF merger deal.

· Warburg Pincus affiliates, which currently own 35.6% in CFL, will see its ownership in the combined entity dropping to 10.2%.

Other Challenges:

- Capital first will have the challenge in converting its retail loan customers in to retail liability side for the merged entity to minimize its cost of funding.

- Growth will be a challenge as IDFC bank is reducing its infra loan book.

- Opex control will also have impact on ROE as it will be aggressive on branch expansion.

- Improving the asset quality of combined entity after inheriting its loan portfolio from IDFC bank will be a huge challenge for Mr. Vaidyanathan.

Key Numbers:

Source: Cogencis.

5 Likes

Risk aversion ups funding costs for 2nd-rung commercial papers

**

Capital First recently sold three-month maturity commercial papers at 9.55% compared with 8-8.25% it paid about a month ago, dealers said.

**

In the market for NBFCs, pedigree counts. Even a cursory glance at the widening spreads in financing costs for the para banks shows that entities with a diverse revenue mix and backed by nationally known promoters are able to raise funds way more cheaply.

Spreads have widened to about 100 basis points on an average from 20 bps a month ago, dealers said., HDFC Ltd, Aditya Bilra Fin, and Tata Capital, for instance, have a more diversified customer base and revenue stream, and they seem to have an edge over peers such as Capital First or Manappuram in raising cash now.

IDFC Bank declared loss in Q2FY19 thanks to 518 cr specific provision.

CAPF results were flat QoQ.

The combined P/BV is 0.9

How do you look at this now.

regards

Disc. Tracking. Not invested.

For Q3, IDFC bank management indicated that certain gnpa and nnpa would resolve bringing down gnpa,nnpa further…

operational performance has been disappointing…I was looking at yes Bank n IndusInd bank’s operational expenses which total to arnd 1500 cr. per quarter (includes salary,rent etc.) Which comes to arnd 1.25 cr. per branch per quarter…IDFC bank has just 206 branches and operational expense of ~500 cr. in q2…I guess the new management will have to look the operating expenses… the merger is 1-2 months away. Looking forward to seeing their plans/execution for creating the liability franchise while keeping the costs under check.

Disclosure: invested and adding, Last addition at 480/-.

3 Likes

Hi All, provision in Q2 has gone up from 153Cr (Q1) to 209Cr…and I dont see GNPA and NPA % in the latest presentation file.

Portfolio % at Stage 3 is 1.92%, is it equivalent to GNPA? If yes, Q1 GNPA was 1.57%.any reason it went up?

Check page no. 13 -

On 2896 cr. stressed assets (includes gnpa, other stressed loans n stressed equity) ,provisions are 80% at arnd 2310 cr. In Q3 , certain stressed assets are expected to be resolved (expected to become standard assets) as per the management n without any provisioning,the PCR is expected to go up from 80% to 90%.

Hi Vicky, you have provided IDFC link, i was talking about CF. Do you know CF numbers?

Thx

Sorry, yes gnpa is the 90 dpd figure only (at 1.92%). Nnpa , I couldn’t find either. Since they have provided higher provisions, nnpa should again be in 1-1.1% range is my guess. I don’t know the reasons for increase.

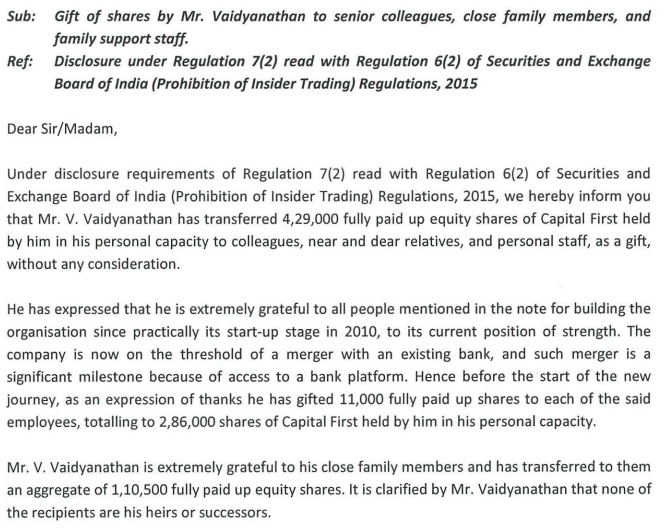

Mr. V. Vaidyanathan has proposed to board to share almost 10% of his personal holding in CF with senior colleagues, close family members, and family support staff. Shows the self-less character of the leader who is truly passionate about building an eternal organization by moving to banking platform and not after any monetary gains. He has not only shared his wealth with existing colleagues but also with former colleagues. This will just increase the loyalty and respect from the people that work closely with him. And as we know that loyalty goes long way in maintaining culture for an eternal organization. A special leader on the verge of doing super special things.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/790a2f27-6900-4dd2-9469-34a3066fb713.pdf

Disc: invested and accumulating in SIP mode. Views may be biased.

7 Likes

There are truly v few leaders in India of his kind. Vaidyanatha also donated few shares few months to an NGO for a better cause. Ajay Piramal also rewarded his employees & shareholders when he sold his Pharma division to Abott.

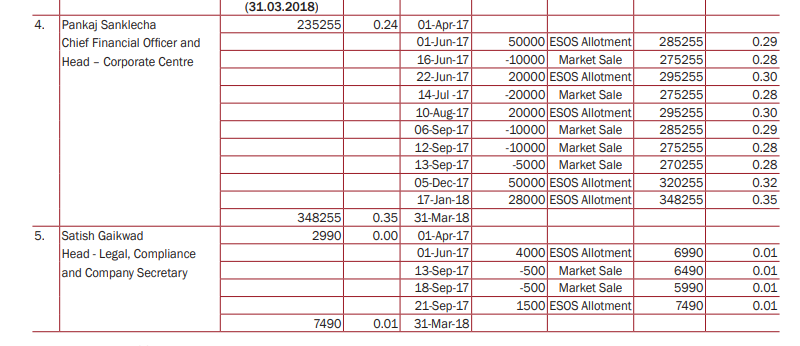

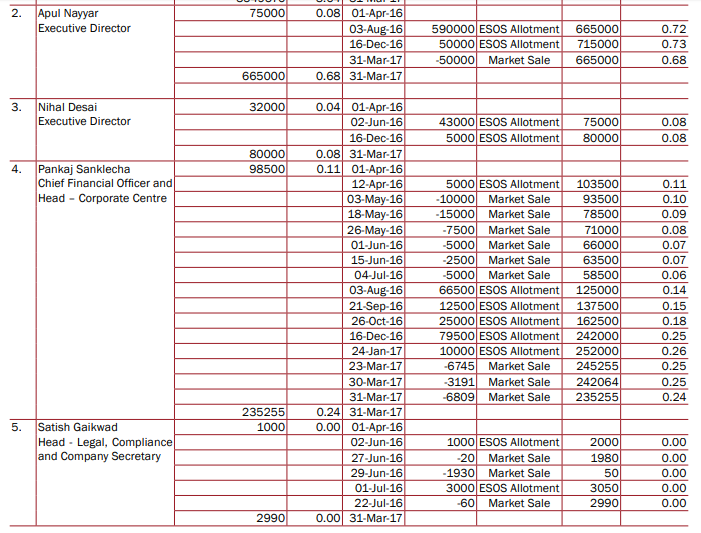

However, I hope top mgmt should recognize the value of their shares. Company (Vaidyanathan) grants top mgmt ESOP so that they can be treated as owners of the company instead of employees and top mgmt sell their ESOPs in open market. The result is, even though PAT has grown at staggering 39% CAGR, EPS has grown at 29% CAGR due to increase in number of shares.

Money motivates most people. If you give too much of it, most people will lack motivation to work anymore. So too much and too frequent equity dilution is a negative. Also it is always at the expense of minority shareholders as it will dilute the EPS. So it is better to stay away from entities that frequently dilute the equity

1 Like

Regarding pat n EPS cagr : They had done a Qip in March 2015 which was the main dilution(7.69 million new shares at 390/- a share).

1 Like