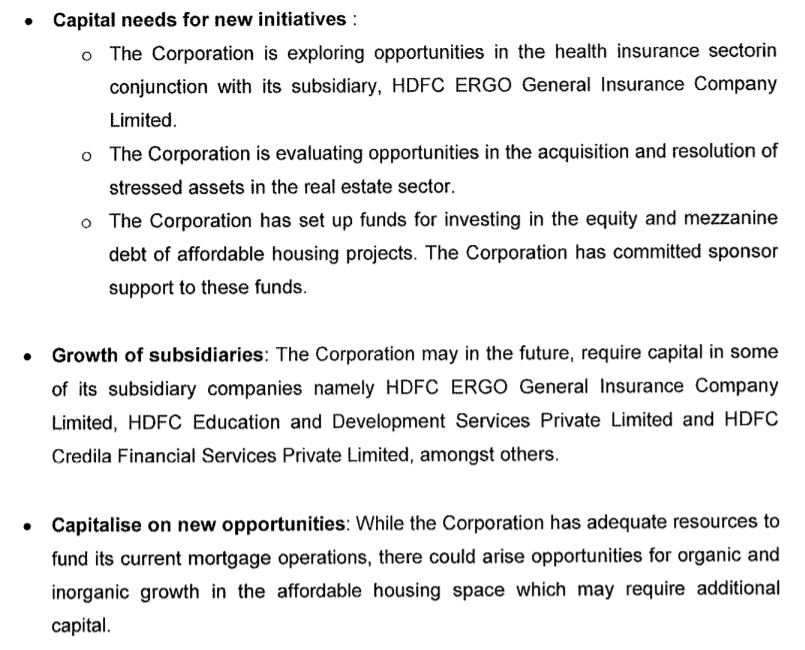

I thought it was only about raising funds for investing in HDFC Bank fund raising activities to maintain its own stake. But the outcome of board meeting mentions few additional objectives for raising funds upto 13000 Crores (of which, 8500 crores for subscribing to HDFC bank QIP / Preferential allotment).

Of the additional 3 objectives, the last one looks interesting - "While the corporation has adequate resources to fund its current mortgage operations, there could arise opportunities for organic and inorganic growth in the affordable housing space which may require additional capital"

Reason why it looks interesting:

Canara bank is working towards selling its stake in Canfin Homes, which is in affordable housing area. It has a clean book and good growth and profit margins, which may present itself as an attractive option for HDFC (should it look for inorganic growth). Also Canfin Homes was initially sponsored by Canara bank in association with few more entities, which includes HDFC itself - in 1987 of course)

Would be really good if HDFC buys the stake from Canara bank…!!!

Comments from Mr.Keki Mistry:

"The company will also look at inorganic growth into the housing finance space. “Housing Business is the most affordable in the last 20-30 years. So this is the best time for the affordable housing segment and we see strong growth,” he said.

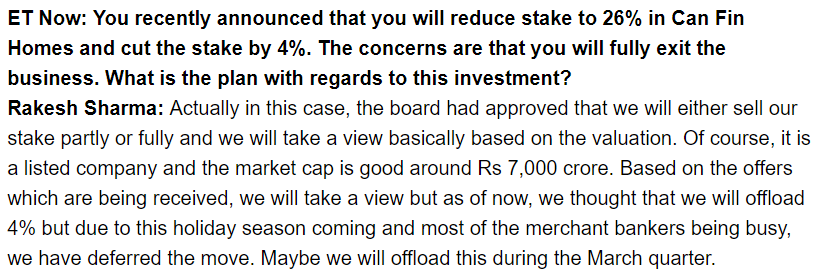

There is report by equirus saying that Canfin homes is ideal candidate for HDFC ltd to takeover. Anyhow canara bank which holds 30% in canfin homes wants to exit and raise money. Equirus mentions canfin homes similar in many ways to gruh finance hence the spike.

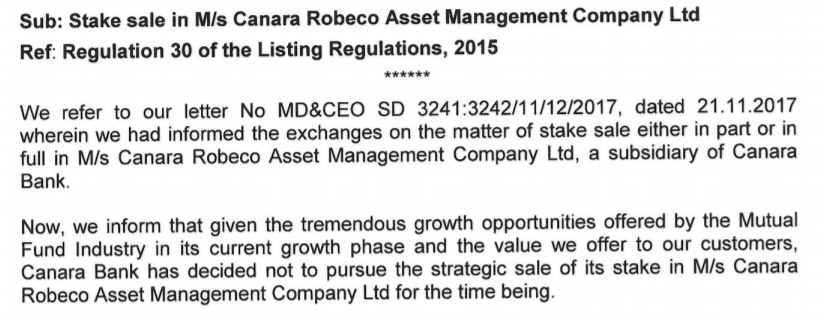

Within a month of announcing the intent to sell stake in Canara Robeco arm, now Canara bank says they will not sell their stake as they see lot of opportunities in the MF industry (Was is not there a month ago??). This along with the news of selling just 4 % stake in Canfin Homes.

Perhaps they are getting good money from the government and are forced by the government to sell the non-core asssets. But sounds too much of a flip-flop in decision making.

This is a cut out from aRvind infra q2 concall highlighting how in real estate post RERA in short term market may behave differently due to different regulatory speed. However, my point is not on real estate companies but to canfin homes which generates 35 percent Loan from Bangalore areas . This could be another reason for slow disbursement n may pick up going forward apart from non home low growth where they do not want to dilute quality. So, next 1-2 quarters will be make or break if loan growth slowness was temporary blip or a longer problem. Disc : Took a small position recently

Can Fin Homes has the average ticket size of 18 lakhs. Since it is average, let us assume the apartments financed by Can Fin in Bengaluru is approximately 30 lakhs (wild guess), how many developers have apartments in that price range?

So why should we think that RERA has any impact on Can Fin Homes, rather why can’t be most of the home loans it services be of self-build nature which is pretty common in India?

Point accepted. However, I am not sure % of loans sanctioned to individual houses vs apartment . If you have data, it would be great Point 2 when they say Bangalore, they lend in exteriors of Bangalore. So, key point let us find if apartments are significant receiver of loans in Karnataka, if yes, then all these apartment builders will need to comply with RERA like Arvind infra and hence would go through similar delays. So, key is to find loans sanctioned in karnataka by apartment vs individual houses. I am not yet totally convinced that it not apartment because they do not lend in core bangalore and exterior areas may have 25-30 lakh property. Avg loan size being 18 lakhs means you will still have 20-30% segment getting around 18-25 lakh loan assuming a normal distribution. So, still going outskirts (as they say extensions of city) with 20% lending in 18-25 lakh still can mean lending for apartments. the break up may remove all confusions

I heard in some interview that about 60% of loans are for own construction and 40% for purchase of apartments. I cant’t recollect where. May be, google would help.

Also, the loan size will typically be a fraction of total property cost / price. Assuming 60% average loan size as total of property value (wild guess), 18 lakhs implies 30 lakhs property and 30 lakhs would imply 50 lakh property value.

If we add your and @pranav_pratap point, then, at least a partial impact of slow RERA implementation can’t b ruled out. However, with limited data and information, we can only make educated guesses . Let’s see how future results turn out

HDFC’s Deepak Parekh is betting big on affordable housing…

“Our endeavour is to participate in the huge opportunity of affordable housing, which is a sunrise segment right now and for many years to come given the housing shortage in the country. The government’s push towards ‘Housing for All by 2022’ will not only act as a growth driver for the real estate industry in India, but will also be a catalyst for GDP growth,” Parekh said.

I hope they don’t sell it to PE funds as PE funds will be looking to exit in few years. This is a good and promising business, so hopefully some big core HFC player like HDFC itself buys the stake, with a long term perspective.