Shobha realtors (primary market is Bangalore) has decent QoQ growth in sales volume. Hopefully the RERA impact of Q1 is one-time impact and general housing sales volume and hence the lending towards it is better in Q2.

Also as Canfin Homes major market is Bangalore (37% or so), hopefully this bodes well for Canfin Q2.

Another related article where they mention interest in entering affordable housing area. If a big, upper-middle class builder is entering affordable housing area, that would be a good boost for the supply side of such projects, which has been a major dampener for the affordable housing story so far.

In report they decreased the earnings for FY18E… the reason stating that increased competetion among HFC’s…but as part of the doing business competetion present everywhere.

Gruh finance has posted good results, especially better disbursement and loan book growth compared to Q1. It may not be a one-to-one comparison with Canfin but the results are quite indicative of a better Q2 (compared to Q1).

Latest news about Canara bank’s plan on divestment of non-core assets. Doesn’t mention anything specifically about canfin homes, but can we expect another divestment to happen within a year?

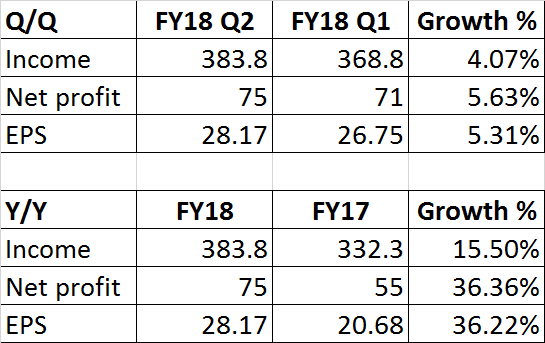

A decent and slightly better quarter (compared to Q1).

Higher disbursements indicate improving environment (although hampered by higher switchover by existing customers). But this is a trend with many HFCs, noticed it in Gruh as well.

NPA levels almost remained the same (marginal increase). This shows that the sudden spike in NPA in Q1 was a one-time event. Need to watch this for few more quarters though.

Need to see how they grow a quality loan book moving forward. Book target of 17000 crores by year end looks quite difficult. But overall, pretty much in line with peers (read Gruh)

Disc : Invested. Above notes are my understanding from partial conf call I attended, you may wait for transcript of complete call for more accurate details.

Zoro99, I attended the call as well but missed the initial commentary on the NPA. Did Mr. Hota mention anything about the recovery efforts and how much had been the additional slippages in Q2 compared to Q1?

@newone , I too joined about 5 minutes late and missed some part of his commentary. However later there were no questions around NPA. Since there was no increase this quarter hence it was assumed to be fine and not worth mentioning.

Some points which i could capture from the conf call as below :-

Cost to Income Ratio 14.6 compared to 14.96 in Q1. - There is scope for improvement.

Operating Environment -

Salaried Class : 70%

Non- Salaried : 30%

See huge opportunity in non-salaried class(SME etc)

Affordable housing is the key growth driver. LIG and MIG-1 should be the driving force.

Majority of their customers are first time buyers.

Supply side issues are there but demand is huge

Rights Issue -

Waiting for opportune time to initiate rights issue.

Positive Impact of RERA will be hugely positive. Q3 and Q4 would show more growth.

FY19 and FY20 would be the best years for any housing finance company.

17000cr for full year - outlook , is that feasible?

Post Q3 they would be in a position to be able to see if 17000cr can be achieved. Appears to be a bit difficult to achieve but thats their guidance.

Competition -

Repayment schedule not an issue.

Can fin portfolio preferred portfolio for poaching.

Competition there from banking space. Banks got better cost advantage due to CASA. But can fin operate in a segment where banks do not target.

Pst GST Impact - GST still in nascent stage. Will be advantageous in long run.

Margins - both salaried and non salaried class has similar margins.

Incremental portfolio share of non salaried gradually increasing. Salaried class seem to be waiting for RERA clarifications and regulations. Going forward in second half year they believe the growth should be driven by Salaried class.

35000cr loan book vision by FY20 - how to achieve -

This is a vision set in FY14. Many things have changed . They currently are looking year or year guidance. This year guidance of 17000cr is still applicable.

Big players coming to affordable space. If supply side issue is addressed, demand is huge.

Post demonitization is the reason for increase in NPA. Asset quality is their forte. They think their NPA is still best in industry.They will not compromise on asset quality to achieve they growth targets.

Is it now 4 consecutive quarters of no (to tiny) growth in loan sanctions and disbursements for Canfin? The management has been sounding positive about the following quarter each time, but hasn’t delivered on its promises. All while competitors like DHFL and IBHFL have started showing really robust growth in sanctions and disbursements after the transient impact of demonetisation. What gives?

Looking forward to the conference call transcript to see management’s explanation.