Looks like the unit metrics around ARR, occupancy, etc have stagnated. Going forward, it would probably be directly dependent on how they scale with additional hotels/ chartered rooms.

If you see the Q1FY18 presentation there is significant improvement in both occupancy(QoQ 59 vs 63) and ARR(QoQ 3689 vs 3799) for Owned and Leased segment. One more point they are not utilizing full 733 rooms as 40 rooms of Delotel Mumbai is not operational yet. This non operating status for Delotel is becoming a concern as it is a on the investor presentation since OCt16 and the status remained same not operational, management should comment on it. Again the ARR may have affected due this non operational 40 room property or else ARR would be 4015 approximately( ARR for 693=733*3799/693). Please correct if i m wrong in my calculation. In AR for FY17 they have increase there Tax Provision to for FY 17 and FY16 are resepectively Provision For Taxation 100,892,191 20,589,010. Which almost 5 times. That may be due to high Differed Tax liability to tune of 9 crore. I like this company because of its high Return Ratios and if there asset light business model continues than these will be high only.

Is anybody going to attend the AGM of Byke Hospitality on 18th September in Mumbai? I will be going there.

If there is any question needs to be asked to the management, please let me know, I will pose it to the management if I get a chance.

1 Like

Hi hrusikesh,

I have three questions…

-

If someone else wd like to replicate the chartering business, how difficult wd that be? What’s the moat that byke has? Agent network? What else? As agent network wd wrk for someone else if given better commission. Afterall, it is mere trading?

-

Any news on the franchisee model? What wd be the profit margins and roe from this vertical? Woyld this be any different than what oyo is doing?

-

Revenue and pat growth for next 1-2-3 years?They were planning to ramp up leased hotel count to 20 in next few years. What wd be the capex requirements, would there be any dilution, etc.

Simple questions…and some of these might get covered by others…just try to get insight on how they are planning to put byke on next leg of growth.

Thx.

I have these question:

-

What is the status for the Delotel, Borivali if it is not operational yet then what is the cause for it?

-

Will the expansion play is the future of the company or they are thinking of some innovative ideas for maximizing or increasing there revenue/profit from the assets?

thank you.

Thanks Mridul and Ravish for giving me the questions. This was my first time at Byke’s AGM. The AGM was well attended, everybody seemed happy because they thought Byke has done a great job in a difficult year(Demonitisation and GST). Anil Patodia did most of the talking/answering and he seemed very upbeat. The only other person who spoke was Ayush Patodia(I think Anil’s son), this young chap talked nicely and seemed pretty intelligent.

Anil answered the questions but some of his answers were too vague. Here is what I remember:

The most asked question was about GST: Anil said GST is a big blessing for Byke, as earlier it used to get affected by cash transactions done by neighbouring unbranded hotels, especially for banquets. Also, in the room leasing segment, the GST rate is less than earlier rates. Current GST rates for Byke are either 12% or 18%. But room chartering business got affected by GST. I couldn’t understand what he meant but here is what I remember he said: “When Byke charters rooms and sells it to agents then there is GST on that transaction, then when the agent sells it to the sub-agent then there is GST on that transaction and when the sub-agent sells it to the end user then there is GST on that transaction. If the GST is on a gross revenue basis then there is no input credit available but if it is on a net revenue basis then there is input credit available. That is the reason why the company moved to net revenue basis for room chartering.” Sorry, Anil may have explained this properly but my recollection is poor because of my lack of understanding.

He said business is good since GST implementation and the current occupancy rate is 65% (I think he meant the leasing segment).

About Delotel, Borivili, he said the property is ready but OC(I think he meant occupancy certificate) is not there yet. They are expecting it soon. And because this property is lying vacant, the ARR and occupancy rates are low. (Here is my doubt: if the property is not being utilised then why is it part of the ARR calculation? is it because they may be paying the lease rental on it?)

They expect the Borivili property to generate significant amount of banquet revenue.

A lot of people asked about their goal of having 25 properties by 2020. Is it realistic? Anil was emphatic in saying that they will meet that goal ahead of time. He said at this point they are talking to 20-25 property owners to bring them under Byke brand either through leasing model or through franchise model. Now they are planning to take bigger/larger hotels.

For the franchise model, on the question of how is Byke different from companies like OYO, he said those companies are losing money and Byke won’t get into any losing proposition. I think he was a bit vague about their strategy. He said there are a lot of single hotel owners who don’t want to or don’t know how to brand their properties. They are keen on the Byke franchise model.

On the question about the online hotel booking platform, he said they will resume work on it soon after the GST related disruption settles down.

He didn’t specify the capex amounts but said there is no plan of any equity dilution or taking any debt. In fact, he said at this point company has zero longterm debt.

To my question about why the chartering business can’t be replicated by a competitor, he said there are some other people who are doing it but none is as profitable as Byke. He said others charter rooms throughout the year whereas Byke charters rooms only for the peak season. Also Byke pays the hotel owners in advance, mostly 90 days ahead of time and sometimes a year in advance. When I said that somebody can give better margin to the agents and take the business away, he said the agent network is based on trust(didn’t sound convincing).

One shareholder/analyst suggested that Byke should explore the option of banquet chartering. Anil liked the idea and said that it has great potential. He said banquet is a lucrative segment and Byke is doing well in this segment. He said the Thane property’s banquet hall has received booking for even 2019.

I travelled all the way from Bhubaneswar to Mumbai just for this AGM and I am glad that I did.

25 Likes

Well done Hrusikesh i appreciate for your effort and thankful to you for asking my query. But my query remained unanswered by the management they are maintaining the status quo and have been saying it for long time. They should have mentioned the cause of the delay. I am very happy to know that ARR is being calculated with the Delotel rooms this gives me confidence that company is improving its ARR and occupancy rate at very good pace. I am very confident about their Delotel property. I have got chance to pass by their Thane property and it looked booked for as many as 4 times. Ayush is a very sharp boy and you can also notice in this video also https://www.youtube.com/watch?v=wQUH4MnDanY . Their property selection is really blessing and this gives us the insight about the category of the management we have.

For a investment to be successful one needs to have Good and Able management, Low Debt, Good return ratio, Low valuation and innovative future growth strategy. I think most the characteristic are present here lets see how they perform from here fingers crossed.Best of luck to all here.

Disclosure: Invested

1 Like

One can also compare it with Royal Orchid Hotels Ltd both of them operates on same asset lite theme. But The Byke has been profitable and Royal is a laggard on profit front but it is improving slowly slowly. One more point is our company is owned by FPIs/FIIs and Royal is having some known Indian valuepickr. Lets see how both stories played out?

1 Like

I surfed TripAdvisor website to check reviews for all byke hotels. Must say this wasn’t impressive! Average rating was between 3-3.5. Lots of reviews were 1/2 star claiming poor service, poor staff, zero hospitality, power issues, unclean bedsheets, stinking toilets, average food, short on staff, rooms in bad shape, etc. On the contrary lots of reviews were good 4/5 star.

I think mgmt’s core focus with lease model is f&b as with this segment tripadvisor reviews do not hurt much. But, as a hotel chain looking to expand and cash on byke brand (through feanchisee model), all this didn’t look convincing.

This company has good bs n model, but customers aren’t satisfied. I know this is budget hotel chain, but still should have the hospitality basics sorted out. Stinking bed sheets n unclean toilets is a strict no no for anyone making bookings after checking the reviews.

Has anyone checked with tge mgmt in this regard? This is a very important question and i am sure must have surfaced sometime in the past.

1 Like

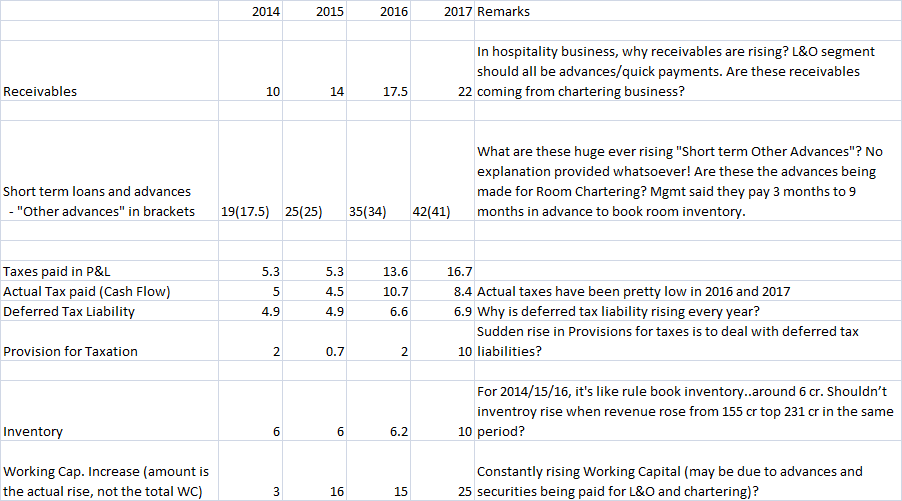

Just trying to delve into Balance Sheet and Cash Flows of Byke for last 3-4 years. Few salient points which needs further pondering -

Any take?

1 Like

@Mridul Good work. Just one suggestion, absolute numbers many times will be meaning less until and unless looked from a comparative angle. For example, receiavble growth from 100 to 130 might look bad but if revenue growth is 50 percent converting into cash profitability , on a 50 percent revenue growth , a 30 percent increase in receivables is a reduction in receivables as a percentage of sales. So, do look at right metrics to draw right inferences .cheers

1 Like

Nice points bro to ponder upon i was unable to dig deep in the balance sheet and finance of this company till you pointed very good points. I did some work and will try to give answer to your some of the points and will try answer them all after more study. I will give your tabled concerns to number from 1 to 8 and will try to answer them so here we go:

-

Receivables can be understood by this comment given in ARs of company

-

Short Terms Loans and Advances " Other advances are the main culprit her"

I did some calculation Revenue growth Vs Growth in Other Advances and it seemed fit for me take it as a explanation that as the room chartering business is growing Other advances are also growing in same fashion please see and comment

3., 4., 5. and 6. I could not get the explanation being a non finance guy this is my weakness.

-

I have read somewhere and i could not recall it where so just mentioning here what i heard or read about increase in inventory increase as there are Food And Beverage + Conference and Marriage and all type of functions management is carrying this inventory for above purposes. This explanation is fair enough to satisfy this change.

-

Working capital will increase as receivable and inventory increases.

_

There are three main components associated with working capital management: accounts receivable, accounts payable and inventory.

_

I just tried to make my understanding clear by giving above explanation and i may not be right. If i am making mistakes than please correct me.

Disc: Holding this share.

Hi,

I have a few queries with respect to the disclosures in the FY17 Annual Report:

-

Can anyone please explain the item Short-Term Loans and Advances > Balance With Government Authorities > Other Advances - Rs 410,920,725 (Pg 69)? To whom are these advances extended and for what purpose? This item is pretty significant (22% of total assets).

-

I have noticed that over the last 3 years (FY14-17), staff expenses have increased at 42% CAGR vs. sales growth of 20% CAGR. Specifically, in FY17, staff expenses have gone up 45% YoY vs. sales growth of 17% YoY. Why is employee expense growing at a significantly higher rate than sales? Even, if we exclude the 63% increase in KMP remuneration, the 22% increase in salaries of other employees is steep at 22% (compared to industry standards) and the company’s actuarial salary growth assumption of 6%.

-

What could be the nature of advances taken and repaid from/to related party Ms. Shree Shakambhari Exims (Rs 109,365,992 - Pg 74)? This entity shares name with the office address.

-

Why have Provisions for Taxation increased nearly 5x in FY17 to Rs 100,892,191? This is significantly higher than previous years’ trend.

-

I doubt that the company has free cash flows for leasing/deposits to sustain organic growth without raising debt. Does anyone have a differing view or can help me understand how it would be feasible.

Although I agree that employee expenses have increased 22%, these need to be looked from two angles -

- If you compare their employee expenses with rest of the industry, it is way lower (20%+ Vs. 4%)

This seems to be major reason for their profitability and if we can find out how they are able to manage such low employee expenses, it would be good.

- The second aspect to this is - newer hotels would tend to have higher % of employee expenses as it is a fixed cost and room occupancy would rise slowly. As overall room occupancy had dropped down in last two years, I feel this might be the case. You can try to get details room occupancy at per hotel level to get more clarity.

Best Regards,

Rupesh

I believe below is positive for Byke too…as decent profit comes from food business

ii. Restaurants in hotel premises having room tariff of less than Rs 7500 per unit per day will attract GST of 5% without ITC.

iii. Restaurants in hotel premises having room tariff of Rs 7500 and above per unit per day (even for a single room) will attract GST of 18% with full ITC.

The Council, during its implementation of GST, decided that the 28% GST would be imposed on hotel rooms with a tariff of Rs 7,500 and above against the previous proposal of Rs 5,000 and above. 18% GST would be levied on rooms with tariffs between Rs 2,500 and Rs 7,500.

The GST on hotel restaurants in five-star and other luxury hotels has been reduced to 18% from 28%, bringing it at par with other air-conditioned restaurants. Food & beverages segment in an hotels revenue form 30-40 per cent revenue for hotels.

In today’s GST council meet held in Guwahati, the GOM ( group of ministers) have suggested that eating out at hotels that have room tariff of more than Rs 7,500 should attract a uniform 18% rate instead of any separate category for a 5-star hotel, which currently falls under the 28% bracket. This will have positive impact on revenue from food and beverages segment of the hotel falling under this category. This will also benefit customers in terms of pricing.

The companies benefiting out of this suggestion would be Taj Hotels, Royal Orchid, Hotel Leela, Indian Hotels and many other hotels which fall under this category.

But byke does not offer 5stars hotels(Do they?)

their target is middleclass, so I dont think that byke falls under this bracket

Please let me know when Q2 Results will be announced

1 Like

this is a pretty sharp fall in topline. Has there been any explanation given?

“The Company has changed its accounting method of revenue from gross basis to net basis for room chartering segment from April 1, 2017, hence current year number is not comparable to last year”