Notes from my research -

INDUSTRY

Indian tourism industry is slated grow at 8% rate for next many years. Indian hospitality industry - 18,400 Cr (FY13). India ranked 11th best tourist destination in Asia & 14th best overall.

BUSINESS MODEL

The company was started as Suave Hotels Limited in the year 2002 & the name was changed to The Byke Hospitality in 2010-11.

The company has following two businesses -

Hotels - Owned & Leased (O&L) - EBIDTA margin ~22%

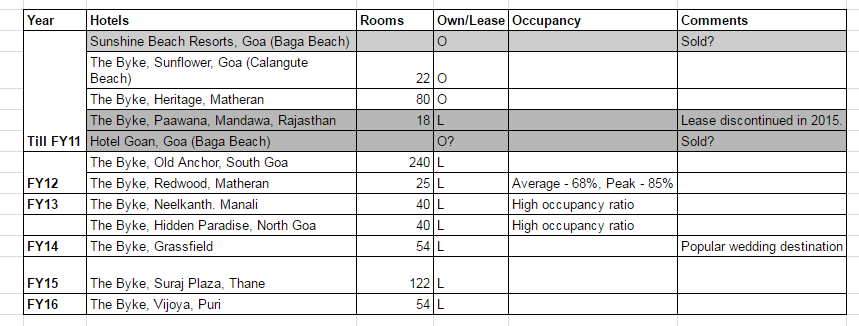

The company owns 2 hotels (details in table) & provides hospitality services in them. The company has not bought any new hotels since FY11 but holds freehold land of ~6.5Cr.

The company has leased 7 hotels till FY16, the leases are non-cancellable (?) & for the period of 10 to 15 years. The lease rates can be revised from year to year basis.

The company claims that these hotels are targeted towards middle & upper classes with the aim to create brand Byke & provide quality service offerings. The company also provides foods, beverages, conferences, weddings etc. services at these location & the revenue via this mode is higher than actual room rents.

(TODO - Premium hotels?? Stay @Byke hotel - scuttlebutt)

The company provides vegetarian only food at its hotel locations. This seems to be targeted towards capturing Rajshthani, Gujrathi, Jain, Marathi etc. family vacations. Also this will help to get higher preference while selecting these hotels as wedding destinations. In O&L segment, actual room rent provides less revenue than F&B etc. service offerings.

Room Chartering (RC) - EBITDA margin ~14%

The chartering business involves aggregation of hotel rooms through prior booking of inventory. This is done on a ‘take or pay’ basis, 3-4 months before the tourist season. The aggregated rooms are sold onward to travel agents, largely in mini metros and tier-2 cities across the country. This is a B2B business.

The RC business wast started in FY12 & as of date contributes ~50% of the revenue.

The main assumption on which this business is based on seems to be - company has sales power to attract bookings/orders. The company has network of over 300 travel agents to help in this sale.

(Trading type business? Sustainable? Growth Plateau?)

NUMBERS

Room Capcity

Freehold Land

FY10

- Sept 2009 - Acquired 38,700 sq. meters of land in Sawantwadi

FY14

- Navi Mumbai - Business Class Hotel - 3.75 Acres

- Aronda, Sindhudurg, Maharashtra - Spa Rejuvenation Centre & Resort - 10 acres

- Ashtamudhi Lake, Kollam, Kerala - Beach Resort - 2 acres

Assets

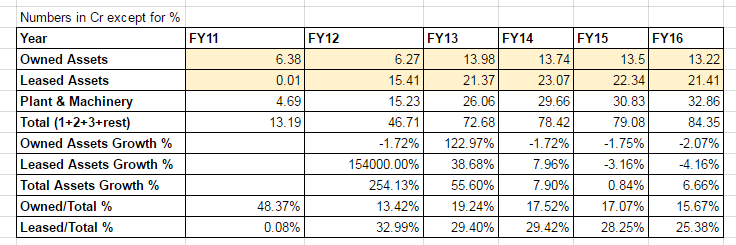

As can be seen, leased assets have grown faster than fixed assets & fixed assets did not grow at all after FY13.

Revenue Breakup

As can be seen above, 61Cr revenue is from F&B in FY16 put of total O&L revenue of ~115Cr. So O&L room rentals by itself is just ~25% of total revenue. One has to look at F&B performance, RC performance in conjunction with O&L rentals to make future projections.

MANAGEMENT

The promoters changed hands in FY11 with Anil Patodia, Vinita Patodia, Kamal Poddar taking over the company. This is what led to remarkable growth in the company.

The management initially issues shares to self on preferential basis through FY11 (75 lacs at the price of 34) & FY12 (10 lacs at the price of 44). The number of shares have been unchanged since FY12.

The management has generally walked the talk on the expansion plans set out after offsetting for general economic conditions & aggressive euphoria during good times. The discontinuation of lease of The Byke, Paawana in Rajsthan & selling of hotels (Sunshine Beach Resort, Hotel Goan) in Goa also shows managements willingness to let go of assets not suiting its business model.

Management Team

Mr. Anil Patodia, Chairman & MD

Mr. Satyanarayana Sharma, WTD

Mr. Pramod Patodia, ED

STRONG POINTS

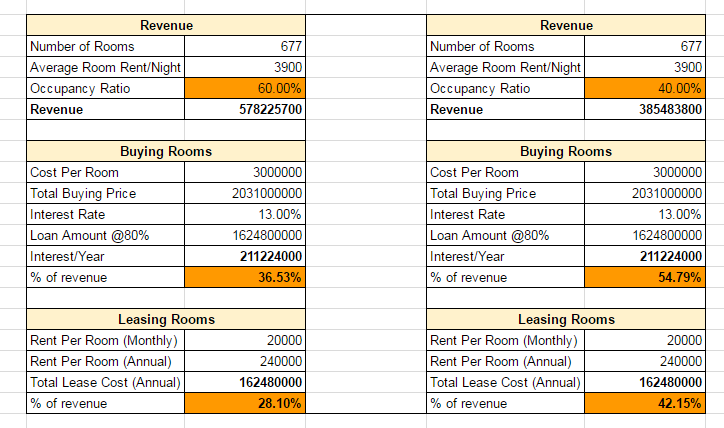

Leasing Vs. Buying - Truly Asset Light?

Due to high interest rates, leasing makes better economical sense than buying properties & paying interest. This helps to retain capital & expand. (See example table below)

The table incorporates a lot of simplistic assumptions & my conclusions can be completely wrong. On the left hand side, I take average occupancy ratio of Byke & on the right hand side I take industry average occupancy ratio. These numbers can be played with with different parameters. I can share excel sheet if someone is interested.

Following are lease & accomodation expenses of Byke

If lease expense of 9Cr is assumed as per above table, then it can be seen that average monthly rent per room that Byke has to pay is lower at 12000 & leasing becomes even more profitable in high interest rate scenario.

It is clear that, interest rate, occupancy ratio & lease prices remain important parameters for financial performance of company.

Securing long term leases at reasonable prices remains key in this model. In leasing model, the cost of lease would continue to recur for 40-50 years whereas in the buying model, after loan is repaid - the asset would continue to give free returns. So in essence, asset light = less burden at start.

Also termination of lease is much simpler in case some property falls out of favor compared to selling of asset. Examples of termination are - The Byke, Paawana, Mandawa, Rajasthan. The lease was terminated in FY15.

High Occupancy Ratio - 70% Vs. 40% Industry Average

It seems to me that focus on middle classes with value hotels is winning formula in India. Also letting out hotels for weddings, corporate events also seem to increase the occupancy ratio.

Balance Sheet

For a company in hotel business, the balance sheet of Byke hospitality is just beautiful. Although I must concede that I have not studied some other hotel business in great depth. The debt to equity ratio never went above 0.25 in last 5 years. Operating cash flows seem decent enough.

Management

The recent turnaround story of Byke started after new management took over. They have growth oriented vision with requisite caution. If they execute on their plan of increasing hotels in reasonable time frame, the business will do well even from here. The management’s attempt to build a brand & 30% repeat customers is also a good effort in right direction.

RISKS

Competition, No Pricing Power, Low Entry barriers

Since hotel industry has virtually no entry barriers (other than capital), there is absolutely no pricing power. If someone figures out that hotel has demand in certain area, one can open a new hotel & provide all similar services. (e.g. Look at number of hotels in Shirdi, Maharashtra). Keeping balance sheet debt free & creating a good, credible brand can protect this to some extent.

The pricing power is further undercut by discounts offered by online players like OYO etc. with their rounds of VC funding.

Room Chartering Business

This business has grown wonderfully well for Byke over the years. With Byke’s ability to get 90%+ occupancy rates, this business has added to growth without taking much toll on Balance Sheet (other than WC days, advances etc.). But there is zero competitive advantage here & someone can easily do what Byke does. Also there might be cases where hotel owners refuse to book inventory with Byke & would rather keep it for themselves. Or they can deal directly with agents cutting Byke from the chain.

Regulation & Taxation

Government’s view on taxation (service tax/luxury tax etc.) & regulation can also affect hotel business. Things like land acquisition/conversion, legal proceedings can hinder the growth.

A NOTE ON ONLINE ROOM AGGREGATORS (OYO, TREEBO, MAKEMYTRIP, STAYZILLA ETC.)

As per new articles & some research, only 25% bookings are done online, 59% are done through offline channels.

OYO

After reading several articles online, it seems that OYO rooms is paying upfront to hotel owners to buy inventory for a duration (like a month). Then they go ahead with their kit & do all the sanitation. They claim that OYO are offering room to end customer with lower cost & it has been deduced that they are making a loss. There are several questions that have been raised by several articles on their balance sheet, accounting methods & viability. One article went as far as calling it a ponzi scheme.

The important thing is many people called hotel directly & asked them to match OYO price & hotels gladly did due to guaranteed payment by OYO. I think the same thing can happen to Byke. Need to figure out how Byke handles it (dedicated agents? But then can’t these hotels deal directly with agents?).

Stayzilla

The company focuses exclusively on home stays & alternate accommodation & have moved away from hotels.

Raised $13 million from Matrix Partners and Nexus Venture Partners.

Treebo

Raised 112 crore from Bertelsmann India Investments.

MISCELLANEOUS

AR FY 11

- Total demand for branded hotel rooms - 2L, supply - 1.2L rooms

- Sales grew by 121% & PAT grew by 139%

- The Byke brand created

- Expansion plan outlines in AR -

- Target to purchase/lease properties in following regions

- Goa

- Maharashtra (Mahabaleshwar, Lavasa, Alibaug, Lonavala)

- Gujarat (Vadodara & Daman)

- Rajasthan (14% foreign tourists, Jaipur & Jodhpur)

- Online travel portal

- proposal to set up Byke rejuvenation center, Aronda, Konkan region

- Promoter holding at 45%

AR FY12

- Foreign tourists - Dec 2011 - 7.15L compared to Dec 2010 - 6.8L

- NPM went down to 4.9% from 6.8%

- The Byke - Spa & Rejuvenation Center started at The Byke - Old Anchor, Goa

AR FY13

- In process to join hands with State tourism departments of India by taking over their operational management of their state owned hotels. (As per AR FY16, this plan seems to have fizzled out).

- OPM Margins expanded from 10% to 17% this FY (why??)

- The company has become niche in “Pure Veg” segment

- Company Considers booking for third-party hotels & earning commission

- Aggressive expansion plan with 9 upcoming properties at - Shimla, Jodhpur, Aronda (Goa), Kollam (Kerala), Navi Mumbai, Mussoorie, Ooty, Hampi, Mahabaleshwar

- Satyanarayan Sharma sold his stake of 5.77% in this FY

AR FY14

- In the next 3 years we are committed to embark on an expansion program to offer 1,500 rooms under our brand, spread across around 25 properties and reach 50,000 rooms through room chartering. (Currently 10,000 rooms available via room chartering) (copied from AR)

- The company has expanded in Goa & Rajasthan as per plan set out in FY11. Rest still under watch.

- The 8 hotels (Goa - 3, Matheran - 2, Jaipur - 1, Mandawa - 1, Manali - 1) has 539 rooms in total & created 80 Cr revenue in FY14.

- Company sold 345,000 room nights in room chartering business - adding revenue of 75Cr.

- Aim to increase to 25 hotels by FY17 & to 50 by 2020.

- Company has 27 sales offices & 350 travel agents. Third party tie up at 8000 locations.

- In this FY, neither leased assets nor owned assets grew a lot. It seems growth primarily came from room chartering business.

AR FY15

- The Byke, Pawana, Rajasthan lease was discontinued in FY15

- RC nights - purchased → 398,000 (FY11 - 105, 950), sold → 373,250 (FY11 - 34,500)

AR FY16

- Plan to add 8 more properties over next 2 year, adding 450-500 rooms.

- RC nights - purchased → 519,967 (94% occupancy)

Disc - I hold tracking quantity & find it too difficult to value this business. This is not a buy/sell recommendation. I am not a SEBI registered analyst. Please do your own due diligence before investing.