Wrote a short note on twitter in September last year regarding Byke.

4 Likes

As for as the Staff Expense is concerned there are lot of contractual staff which is marked in other expenses . If we add up the Employee expense with Contract staff number this comes to around 20 % which is similar to that of Royal Orchid. As for as Tax expense can you please let me know from where you are getting this info. As per the cash flow statement the number looks similar to P/L numbers. Thanks for your details.

Hi Hrusikesh,

Small cap investing is like investing in options & start ups but with superior reward to risk ratio . Only one needs to be diversified .

During bull market one will hear lot of stories that will tell you how the business model is superior and how management is intelligent and in bear market you will equally hear how flawed the business model is and how corrupt / fraud the management is … Some of it may be true and some of it be may be noise .

In past I have experienced this in many stocks like Nilkamal , Graphite India . Venkys , Sona Steering , Cosmo films , etc … I have mentioned my experience in my post LUCKY TRADE (July 2018 ) in BULL in BEAR Market - #14 by kb_snn

Now coming to Byke … I have too invested in this stock @ Rs 150 odd but as startup kind of investment … I am ok if the value goes to zero … What was my logic when I invested in this stock

-

Focus – Like take example of thought of being Pure vegetarian even in Goa and Himachal - It takes guts to take any strategic position and sticking to it for years & across location… My experience in investing in business - often management with guts to stick to a strategic position across time lines often wins

-

Ability of think different - However stupid or intelligent Room chartering business may sound - in common trade terms it is called whole selling - It is what tata coffee does with coffee , ITC does it with soyabean , coffee and wheat and or KRBL does with Rice . There are time when it works wonderfully like when your own Cost of capital is cheaper . Most companies boost their ROCE of anchor business with these trades plus it gives them more bargaining power for anchor business . While OYO may also do the same thing , the approach by BYKE is like traditional wholeselling - that makes it more interesting … I would like to see if such a solution can really work on large scale .

-

Focus on events vs individual travellers : This is positioning that makes them focus on Food vs Room and focus on Local / regional crowd vs outside tourist … Hence you see them less sensitive to trip advisors kind of tourists ( though recently you see them responding to travellers issues at least on website ) … This business model is very popular in budget hotels ( not the ones that are listed ) – Here cost of Bulk room rates and food rates are critical … Also you need maintain few rooms very well for key guests and rest rooms will be in OK OK condition.

-

Cost Focus : In the opportunistic business model chosen by BYKE you need to cost focussed . It has no loyalty to location unlike TAJ etc wherein they fought hard to win back Delhi property . Byke will leave location if customers flow is lower or some other issue happens … Hence it invest very little in leased property making exit easy and landowner often has less bargaining power … and hence lease rentals can be lower … Plus they run firm on lean management and staff . Now one may debate this model is not scalable or cannot be branded - That is reason this startup idea is different and needs to be tested … If it works we may have hotel business model that makes money … Rest models like TAJ and rest will never give you good returns on capital .

Finally what if business numbers are Fudged … Well that is risk we need to take in small business and hence one needs to diversify …

Best wishes – Keep spirit & hope high in equity investing … It is required in market as things can be even uglier or better from here

7 Likes

I don’t understand why promoter being brother is a problem? Choice international is well managed company by a set of CAs and I was quiet impressed by their financials in last few years.

More over choice broking services is already declared as promoter of byke hospitality since more than 5-8 years and the information is already public.

First of all I would like to thank @phreakv6 to bring new perspective and to show a direction in which we can dig further. Also your website is very good will suggest every one to go check out the facts by your self. I agree with you on almost all the points because I too had the same feeling and ambiguity last year when I saw these transactions, but i did a mistake at that point by ignoring them. In the agm too I observed one peculiar thing that they only give 1 hr for it and they finish it within time limit as if they were just conducting for formality. The biggest problem in their AGM is that, ppl there ask lame/useless/stupid(sorry if rude) questions and praise the management. Like for instance let me give one example-

“Oh sir your photo on the front page of the Ar is very good. You are out of the world person, you hotels are working great. You never get tired to give us the best results we want. All thing you do are great no doubt about them but we dint find your smiling photo of you on this year’s Ar”

Literally this is the language they speak in and this speech of many investors(So called investors but not real investors) goes and goes on for 40-45min. After that the poor investors(real investors/analysts) get the chance to ask their questions and clear their doubts(hardly 10-15min). After that they dont answer any questions because there is another AGM in the same hall- Guess who’s- its Choice Internationals. First I was very upset because of this type of approach then I came to know the real game behind this. I came to know from my close reliable sources that the promoters of many co’s(not just this) pay these people to sit in the AGM and just give the co majority voice in any decision that Co is great and waste the remaining time. Poor investors/analyst who goes there thinking he will ask many questions with promoters is left with no time to ask and clear doubts and AGM ends, he feels that this co is good as many investors were barging about it, but he fails to understand this real game. Same thing happened with me. I am pretty sure that who ever has attended their agm must have experienced the same/similar situation.

These were some points I noted and I have many more written in my dairy but this post will be lengthy if I write them all.

@paresh.sarjani1 Sir on what basis you are telling that choice international is well managed? If you ask me byke is far better than Choice on financial condition. That NBFC is having trade receivables of more-than 75%, Receivable days of more than 280 days(I mean which NBFC has 280+ receivable days?). Many red-flags.

A big redflag for me and a confirmation for me was when recently they have pledged shares, that too in a very abnormal way like Poddar family that runs Choice is a promoter in Byke and the Patodia family is a promoter in Choice. Poddar family has pledged Byke shares and Anil Patodia has pledged Choice shares. Like common whom are you people fooling? Byke is asset lite atleast it doesnot require pledging of its shares in such market conditions but yes Choice is really in hunger of money as all its money is stuck in trade receivables(this means it is not realizing any NPA’S and just inflating their balancesheet/P&L), this is the primary reason why Choice is trading at 0.85 of BV

I ignored some key areas so I had to pay the price.

Note- This is my personal view and observations so take it lightly

9 Likes

This is very informative. Thank you @phreakv6!

Great work @phreakv6

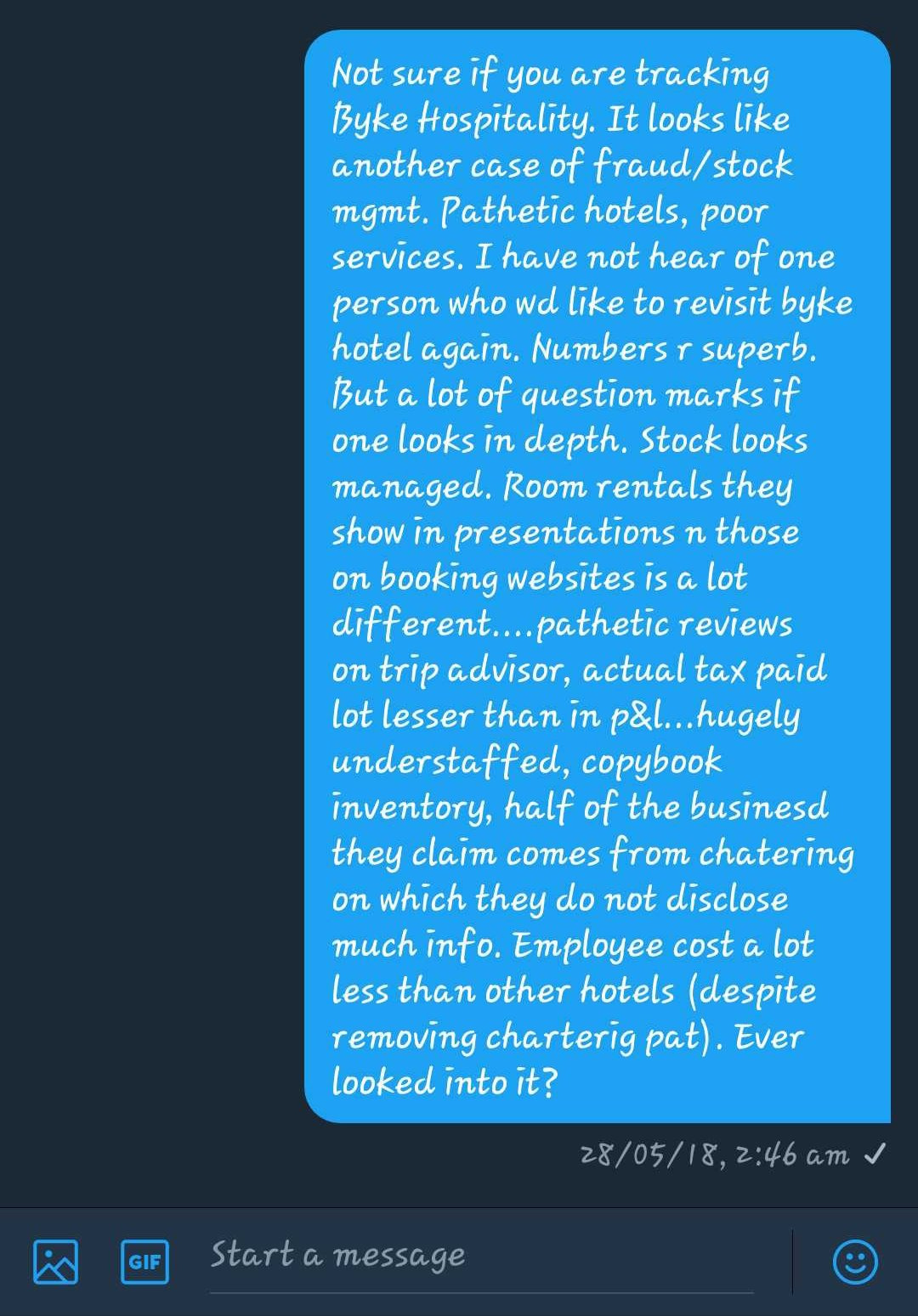

There does not look any incidence of pumping the price here as we witnessed in Vakrangee ! The price was around 160-180 for a 3 year period. Only shift in hands by different trading companies was going on.

Apart from holding different combinations from the same pool of companies , lots of directors of one company are present on the other too.

Darshanik Valuserve director Jitendra Berde is associated with Novus Tradestar where the other directors are Mohd Latif and Rakesh Kanojiya.

Mohd Latif is also a Director in Chartered Capital , Florence& Carron.

Rakesh Kanojiya is also a director in Paath Financial and Choice E-Commerce.

One of the Choice E-commerce director Kamal Poddar is also a partner in Choice Strategic Advisors Llp where the other director is Vikash Kumar Agrawal.

This Vikas Kumar Agrawal is a Director in Byke Hospitality.

It is a very complex web and is done in a such way that it no where connects the links with the main promoter Mr. Anil. Only that , these entities used to trade in the company shares.

I guess it all started where these entities offloaded their stakes while some time later Mr. Anil started acquiring 4.83 Lakh Shares (1.2%) of the company in between Dec 2017 to March 2018. It is obvious that such promoter buying is most of the times seen as a good signal for the company. I think , this is where the distribution should have started and prices kept on falling.

Though lot of red flags were highlighted in the thread before the collapse. The poor quality of services, rating suspension by ICRA and few other points by one of the experienced member @dd1474 in his post Byke as well as by other members.

Overall a good learning !

2 Likes

Please check the dividend as a % of Net Profit. They gave a dividend of around 2 Cr when the profit was around 2 Cr (around 84% Payout according to screener) and they maintained that Rs.1 dividend irrespective of share capital (dilution doubled the base since FY15) so the dividend amount was 4 Cr when they claimed a Net Profit of 36 Cr (11% Payout) which is a far cry from the FY11 levels. The numbers are unbelievable only in the last 5 years and it is during this time that things get dodgy.

Not apples vs apples comparison but despite the falling knife scenario, there is delivery of shares unlike DHFL where there has been less delivery for months. I am not sure if these are investors or traders, but there is still interest at this price, I don’t know what it means.

From Screener.

Byke

DHFL

Comments?

A big chunk of cash flow is spent on capex (refresh of current properties + refurbish of leased properties), so there isnt much left to distribute as dividends, it has been in the tune of 7-9Cr in the last 5 years. Not raising dividends dont look unusual though.

Thank you for enlightening us all on the stock management behind the scenes. I have exited it, but am curious to see how the movie unfolds from here.

Promoter has bought 2 lakh shares of vakrange from the open market. It’s disclosed in bse stock exchange.

I guess this sums up that Byke indeed is a lost battle for investment. If the stock is down > 80% from the top and the promoter yet chooses to buy shares of another company from open market (despite the other company arguably being a case of fraud), then is something wrong with the promoter. No two ways about it.

The Promoter of Vakrange has bought 7 lakh shares from the market of Vakrange company. This has nothing to do with Byke.

Oh my bad. I didn’t check the filing and thought it was the Byke Promoter who bought the shares. Because that certainly would have been the nail in the coffin.

The results are out and I believe they have doctored the numbers perfectly to show a nominal profits by showing all income as expense due to loss in chartering business. How can chartering business incur such losses? I think these guys will keep showing losses from now.

53804228-90c4-4322-b13a-b30d0fb3aa99.pdf (1.2 MB)

And no mention about the reason for such drop in profits in press release.

a9836f36-7f86-4598-96ef-fc5f61962ca0.pdf (500.3 KB)

4 Likes

You are right . This stock will go Vakrangee , PCJ way . Down the drain .

One needs to write off the investment as learning loss …

I am going keep this stock to tell me how stupid I had been … It was a great learning experience

I was expecting good part of 29 crores loss - Trade receivables as shown in Sept to done this quarter . They seem to written off 10 crores .

It will interesting to see what they present in March results . Will eagerly wait to see change in their Trade receivables

3 Likes