Can someone help me understand the financials of this company.

In last 10 years topline grew about 15%CAGR, bottomline 23%CAGR, and the stock grew at 52%CAGR for the same period(maybe due to 8-10 times PE expansion)

Return on equity almost zero, How did it manage to sustain that growth without diluting equity?

Secondly how does cash reserve in 2011 jump from 9.70 Crore to 662.96Cr?

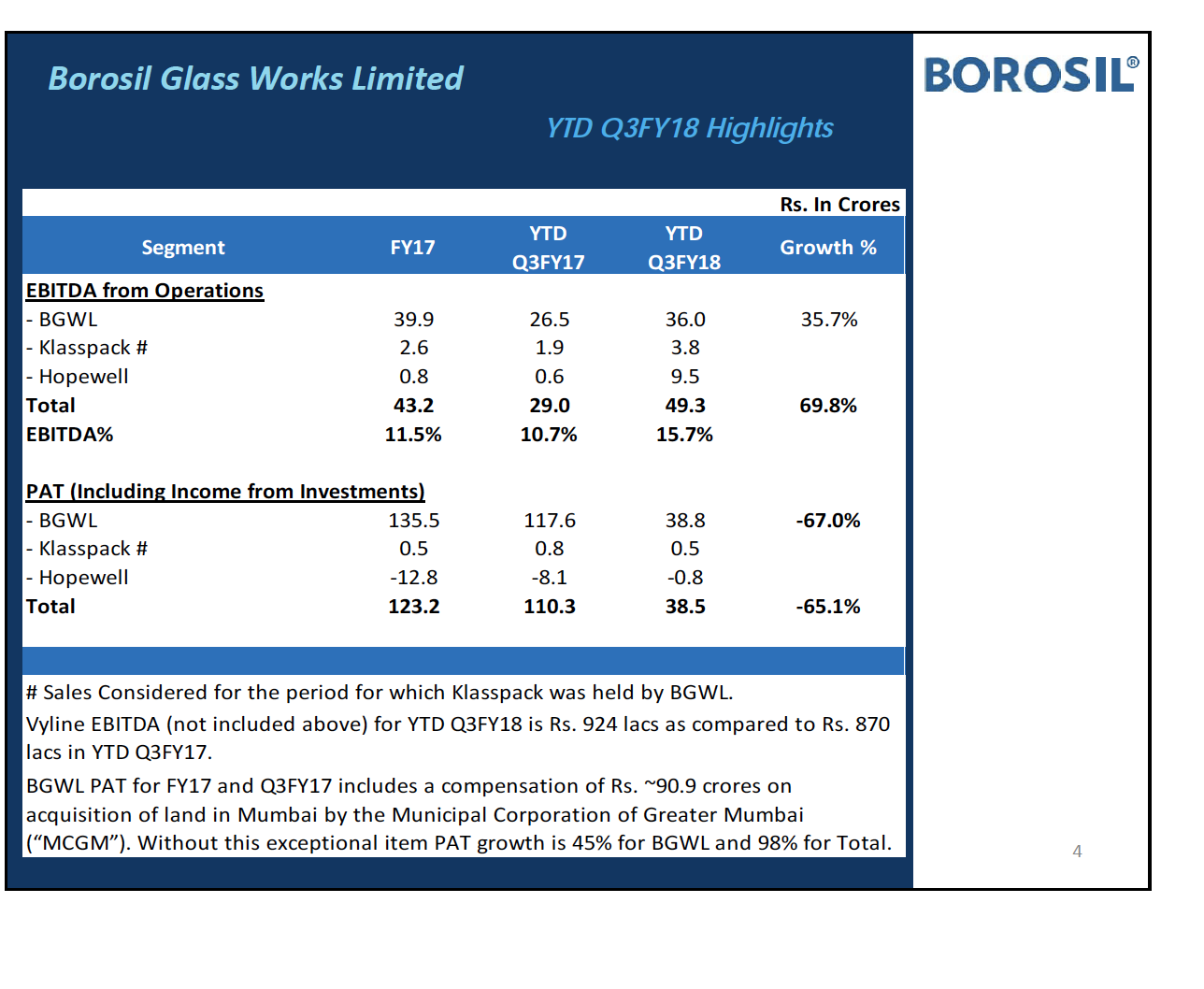

The company has other income from investments. The investments are from the amount they realised from sale of land in Mumbai. The profits from operations are almost non-existent.

which year did it happen ?

I think about 6 years back.

Well very difficult to read P/L statements of such companies. What I understand is parent business has not generated any cash with OPM fluctuating between -10% to 10% thereby averaging low single digit ROE but it’s investments have grown in leaps and bounds in last decade which helped the stock become a multibagger.

There has been a sudden upward spurt in the stock. Was trying to find the reason of the increased interest in the company. Other than finding an interview of the CEO I could not come across any findings related to any fundamental level changes. He talks about the benefit of GST for Borosil and how unorganized players would be affected. Also there seems to be no bulk deals, the last one was in March 2017.

Looking at solely the top line, the standalone sales have been good. The exceptional item of (9088) Crs and the tax exemption from the sale of the Andheri land can be accounted for in our analysis. Looking forward to reading their notes and schedules.

Borosil reminds me of my banking days. In our treasury we had a team called BSMG - Balance Sheet Management Group. Lot of BS management needs to be done for Borosil too. One can imagine what fear a person with the most ‘commoditzed’ degree (combination of engineering plus mba) feels when he or she sees such financial statements. The horror of not being able to balance his balance sheets flashes again!

Rgds

DV

Disclosure: Invested in Borosil Works and Gujarat Borosil

1 Like

@deevee since you are heavily invested in glass stocks, what do you think are the drivers for growth ahead. Just going by numbers , I still dont understand how borosil’s PAT grew by 63%CAGR in last 10 years whereas topline grew by mere 15%CAGR. However recent(3 years) data shows consolidated topline grew by 52% vs standalone’s 20%.

Do you have conviction that topline will grow at 20%+ for next 5 years ? If so can you help me understand the drivers.

Disclosure.Though I am Invested, but I must admit I don’t understand the business much yet. I am invested in plastics as well which looks kind of antagonistic

1 Like

Reason for price surge in Gujarat Borosil

Hi Ishan

Apologies for the delayed response. Was away from the forum for sometime.

I have actually readjusted and consolidated my portfolio and have exited the borosils almost completely. There is a very good analysis done on this blog. You must read it.

I think the business on consumer side will surely grow but i wanted to use my limited money for investments elsewhere. Also I couldnt follow this stock much.

Apologies my answers are not of much help.

All the best.

Thanks.

Regards

Deepak

That blog is about past.

I was going though couple of research reports of edelwiss topline to grow at 22%CAGR for FY17-FY19.

Also see a mention of OPM to improve from 10% to 15%

2 Likes

I came across Borosil Glassworks some time ago and while my initial impression was mixed (due to reasons I will cover later), but on more detailed research it seems like a good multi year story.

The company is essentially engaged in 2 businesses;

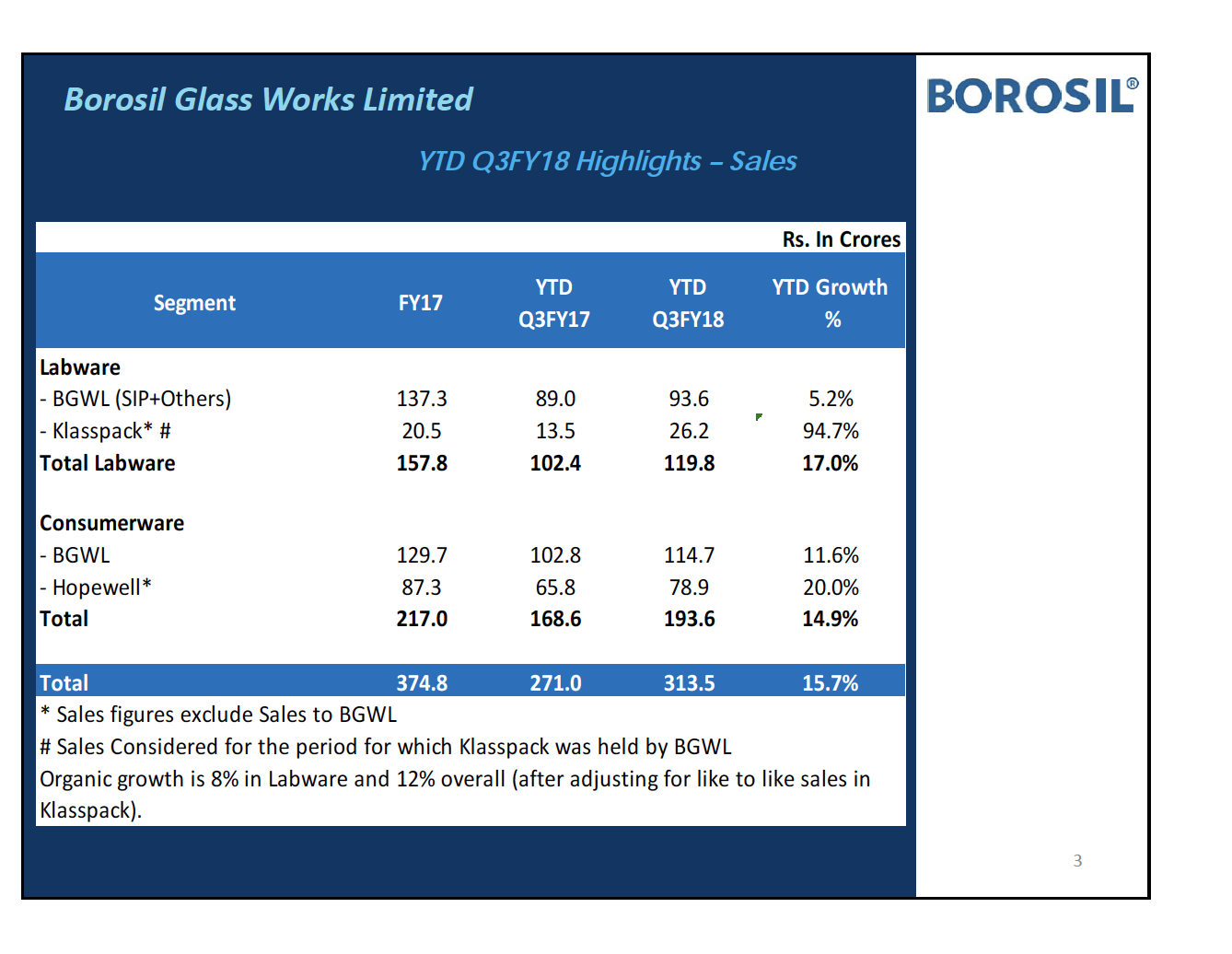

a) the consumer products business including microwavable glassware – for which is it quite well known and opalware (which it entered through an acquisition 2 years ago). This segment forms approx. 63% of turnover &

b) Labware division which basically comprises Laboratory equipment such as beakers, bottles, test tubes etc, used mainly in pharma & possibly other chemical industries. This comprises balance 37% of turnover as per 9m YTD 2018 numbers.

The company in the past has had legacy issues in the sense they did not seem investor focused; for one they are not listed on NSE. More pertinently if you look at the 2017 AR while the company is debt free and cash rich; the cash is deployed in lots of equity holdings (as in listed marketable securities) that are actively traded in. This for me was a no-no and I had not invested in the stock at the time, though I had liked the business aspects.

However on more digging into this apparently the management has changed with the promoters son Shreevar Kheruka having taken over. While he did so a few years ago in the last couple of years he seems to have taken a number of pro shareholder measures. The legacy trading investments are now gone (as per the last concall) and money is now invested in liquid securities. Also non core assets are being unlocked,the company sold a chunk of real estate in Mumbai in 2016-17 with extraordinary income of 90 cr. Another such land parcel in Mumbai is now put up for sale with a tentative value of approx. 68 cr. Holding structure is being simplified and company should have a very clean balance sheet from next year.

Business wise there are a number of factors that I found attractive:

a) Last 5 years revenue CAGR is a very healthy 29% & EBIDTA CAGR is 38%

b) While the company is well known in the glassware segment it has now entered through acquisition of a company called Hopewell into opalware (a sector dominated by La Opala among organized players); which is a related & value added segment with much higher profitability. Initial performance has been promising.

c) It is also getting to larger business segments such as storage containers/ tumblers which are much larger than its traditional glassware segment (details in attached investor presentation).

Since distribution channels are pretty similar the company should be able to leverage its brand and reach over time offering significant long term growth opportunities. Plus the company is giving more focus to modern trade & ecommerce which are currently small in size but have potential for expansion of base.

d) Competition in all these sectors is primarily unorganized and post GST organized players should be at an advantage.

e) Company will benefit from general growth in consumer discretionary products as well as the slow shift from plastic products to glass/opal both on account of aspirational factors as well as environmental issues (such as recent plastic ban in Maharashtra).

f) Company has recently expanded capacity in consumerware with a new furnace, as per management this will expand capacity by 50% so there shouldn’t be major capex in near term.

g) In Scientific products also the company is the market leader for many products. This segment I do not expect to match the consumer segment in growth but it has higher entry barriers (products need to be approved for QC in pharma) and

Other than the above business issues notable point is that the company has applied a few months ago for an NSE listing, and once that comes it will come under the radar of a number of institutional investors (currently MF holding is nil).

My guess is that this current absence of MF holding is partially due to internal MF guidelines or preferences for a NSE listing. In any case the listing when it happens will definitely improve liquidity and visibility as the company is in the much favoured consumer discretionary sector.

On the financial side the company is debt free & has some 190 cr in cash as per last concall not counting the proceeds expected from proceeds of land parcel. Management is guiding double digit revenue growth in all product lines and higher profit growth. This seems very possible, as seen from below screenshots.

Main negative I see is that for a smallcap it is not cheap (FY18 PE should be above 22 after annualizing 9 month earnings even after current decline) but these seem to be offset by a good consumer business with strong franchise, good visibility on growth and profitability as well and strong financial structure.

Other question mark is that the company holds 58% (post restructuring) in Gujarat Borosil a sister concern manufacturing solar panels. Solar panels again on fact of it is not a great industry with huge Chinese competition. However management seems quite confident on it, as per management speak they are making higher end glass which does not compete with Chinese imports and they should be able to hold their own even if anti dumping duty is removed. I would not be as sanguine on that but they have shown good profit levels continuously and management has given a lot of interviews about how their product is differentiated and better. Not a technical person to vet those but think this may not be a drag on holding company.

Some links

http://www.borosil.com/doc_files/BGWL%20Investor%20Presentation%20-%20Feb’18.pdf

http://www.btvi.in/videos/watch/26319/beyond-the-bottomline--borosil - a detailed interview of Shreevar Kheruka

6 Likes

What I liked about the current management is they are doing what they said they will do, whether liquidating dead assets like land and flats or putting money in productive assets etc. On con calls, they are pretty open and honest about their goals and targets.

Remember this is the same company which has done 25% share buyback 2 years back for which company spent Rs 174 Cr !! This is HUGE positive step for minority shareholders. I know many companies sitting of cash piles but very few has taken such a bold share holder friendly action.

Disclosure - Forms 10% of my portfolio and continues to add on every drop

2 Likes

Thank you for sharing the links. The interview inspired confidence and the CEO seems very level headed and result oriented.

Disc: Invested (with MTM Loss) and planning to add more at lower levels.

@Marathondreams @shenbal - agree, the son seems to be much more dynamic & level headed. I think a lot of Indian managements have realized they can make more money by focussing on shareholder returns and showing profits on books rather than through the old Indian promoter jhol/ jugaad style. See a good long term story here.

I have also invested last month am also looking at adding to add further on declines.

1 Like

Borosil got listed on NSE. This should help improving the liquidity

FY18 & Q4 Results:

Investor presentation:

1 Like

Great set of numbers. Standalone sales up by 16% whereas PBT up by 91%!! Consolidated sales were impacted by Hopewell furnace up-gradation.

Once company completes amalgamation of related parties like Hopewell Tableware Pvt Ltd, Fennel Investments and Vyline Glass works (pending at NCLT), it will simplify the corporate structure and remove related party transactions. Company is sitting on 260 Cr of cash (not good for ROE  ) but that gives them opportunity for acquisition of regional players.

) but that gives them opportunity for acquisition of regional players.

2 Likes

Borosil Concall

http://www.borosil.com/doc_files/Borosil%20conference%20call%20Transcript%20-May30-2018.pdf

Key points

- Management seems positive on pretty much everything, a bit too positive I thought! Commentary is like a Sooraj Barjatya film with no tragedy or villains

Anyway on the facts side, revenue growth & prospects looking good, EBITDA expected to move in 15-20% range over 2 years with above 15% in FY19. Last quarter this was 13%

Anyway on the facts side, revenue growth & prospects looking good, EBITDA expected to move in 15-20% range over 2 years with above 15% in FY19. Last quarter this was 13% - Maintenance shutdown done with, opalware unit fully functional

- Capacity expansion would need to be done in laboratory glass business in current year + capex for central warehouse discussed earlier would be taken up in current year.

- Looking at geographical expansion in opal business (currently strong only in North & East)

- One time real estate gains seem to have ended, there is some balance surplus land but that is encroached since many decades (near Mumbai airport), IMO this is never going to be monetized

- 250 cr cash in books, looks like it will stay there for some time. Not clear if the 65 cr land sale in FY18 is in this already, possibly it is not there.

- In general a good set of numbers for FY18, in line with what I hoped for. I see broader trends like GST, move away from plastic, increase in product categories to be very beneficial to BGL in medium term.

Anyway on the facts side, revenue growth & prospects looking good, EBITDA expected to move in 15-20% range over 2 years with above 15% in FY19. Last quarter this was 13%

Anyway on the facts side, revenue growth & prospects looking good, EBITDA expected to move in 15-20% range over 2 years with above 15% in FY19. Last quarter this was 13%Couple of points on flip side

- Not really convinced about the loss in the standalone consumerware business in Q4, management has said seasonal impact, but I find it weird since sales have grown despite supposed weak season. Can be inventory level adjustments especially with shutdown et al, will go with management view…

- I had written earlier that this is an example of a management that seems to have decided that you can make more money through market cap growth rather than by avoiding tax. Modus operandi seems to have been showing higher profits in Vyline which is the promoter owned manufacturing business through favourable transfer pricing. This will end as promoter owned business is getting merged with listed company in ongoing merger scheme (that will actually be a plus since those margins will also come in books) but a fact worth knowing.

4 Likes

I bought it very expensive because they took care of the negative point 2. I think they are spending a lot of money on brand building and pushing their products. I am willing to give them 1 year to improve their margins after the entire integration of businesses.

Disc- It almost forms the second largest stock in my PF