Basic rationale for investing in this company is the global supply disruption due to pollution crack down in China. It’s a little unnerving when investment rationale is an external factor and not something that the company itself can control. Although China issue is structural in nature so it can persist long enough to make the current scenario the new normal. In that context, the Indian specialty chemicals industry has good prospects and Bodal is one of the good players in the industry (I will post my peer analysis in few days).

However, its not a question of if but rather when the Chinese supply will come back in the market and at what price. That’s a big unknown at this point. There are estimates of 12-24 months from now which looks reasonable. Even if the Chinese manufacturers are not price competitive as and when they start producing again, they are likely to undercut their Indian competitors on prices to win back their customers. That will be a real testing time for the industry. At some point, market will start discounting that eventuality.

Disc: Building a position.

Perfectly sums up my thoughts on this company…

Disc: Invested

Very well summed up Yogesh bro!

I am studying akshar n shree pushkar though invested in bodal from lower levels. Would be great to share our notes .

CARE upgrades short term and long term debt rating

ICICI report on Bodal Chemicals

http://content.icicidirect.com/mailimages/IDirect_BodalChemicals_MgmtNote.pdf

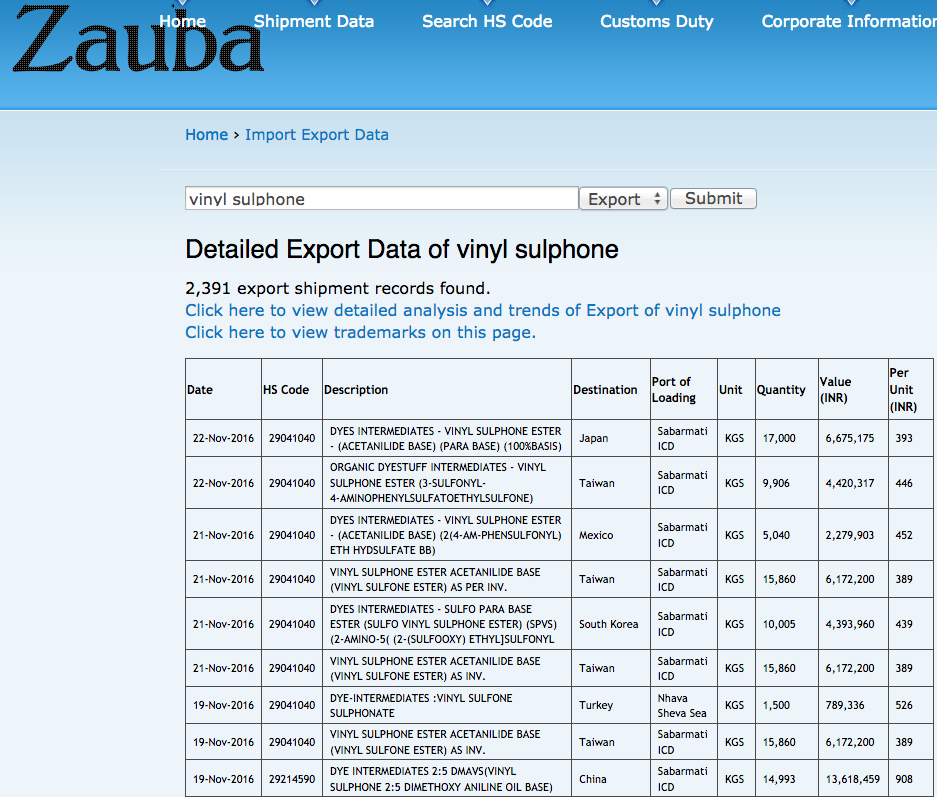

I am struggling to find price of Vinyl Sulphone/dye intermediate for the month of January - 2017.

Latest data I could find is for the month of November - 2016.

Any suggestion on how to keep an eye on price of dye intermediates will be most welcome.

Thanks

Not sure of the prices of dye intermediaries and vinyl sulphone. But i

found an interesting fact in the BSE new 52 week high list…About 30% of

the companies in the list are from commodity chemcials and speciality

chemicals industry. But they are smaller tier3 kind of companies with

revenues of say about Rs 50 Cr or less. I suspect that the chemcials sector

rotation has gone to the bottom most companies now where even they look

fairly valued equal to that of tier 1 companies. The rotation has to come

back to tier 1 companies now again as they look cheap now…Have an eye on

the big ones such as Bodal, Bhageria, Aksharchem, Dai-Ichi etc…

Disc: Have a 10% investment in the sector as a whole. My views cud be

biased…

FY17 Q3 Results announced.

Good set of numbers

Does anybody have the transcript/notes of the yesterday’s call?

Hi Guys, came across the below news

Dye/Chemical Sector update-The biggest Chinese company Hubei Chuyuan has started production again leading to product Price corrections.

How do you think this will impact the industry and Bodal chemicals?

Hi

This chinese company has started production from Jan 17 itself. In that

sense it is not something shocking or new threat. The Vinyl sulphone prices

have come down by 30% and some other chemical prices have also come down.

But Bodal and Akshar are very confident of profit growth in coming

years…They say that the current prices are still more than 20% higher than

prices of early 2016…They say that margins will moderate but overall

profit growth should be good due to volume growth. They say that the

chinese will never be able to do as much volumes they did 1 to 2 yrs back

due to environment restrictions…

@varunm2112 Can you please link you source of information regarding Hubei Chuyuan?

See Shree Pushkar concall transcript

There are references to Chinese operations on page 7/8, 14, 15. Bodal Concall also mentioned something similar in their concal. Prices being low are apparently not so much of a concern, as long as they are stable. Fluctuations or steep rises/falls can create temporary impact, till the companies get time to adjust to the new prices.

Chinese cos are now much more regulated on the environmental front. Hence they maynot be as competitive on prices and on volumes as earlier. Customers would prefer sustainable suppliers, and Indian cos will benefit.

Regarding Bodal, the new initiatives of the management are progressing well. They are walking the talk. These steps will improve the business profile and give it the necessary diversification (albeit within spciality chem space).I have very high regards for this management (as elaborated earlier).

Discl - hold from lower levels. no change in holdings from earlier levels.

DSP Blackrock MF and Religare are meeting the Bodal management tomorrow the

6th for analysis. This is a good sign…

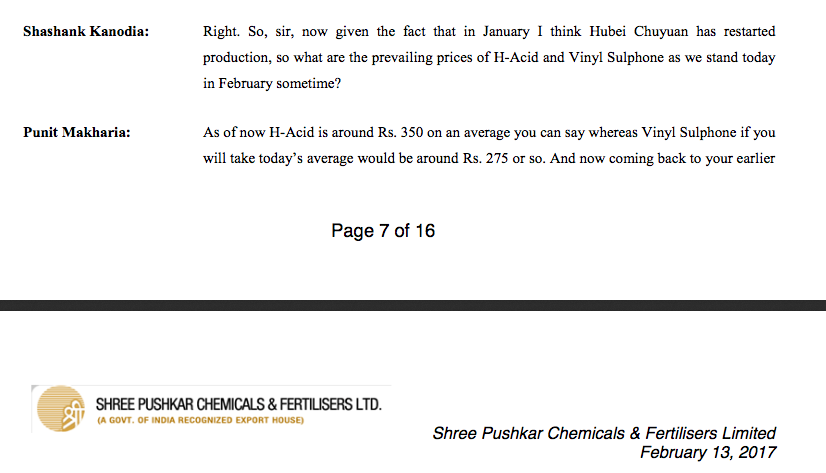

Thanks @sammy11 for mentioning the source. I think 275 is good price for Vinyl Sulphone. It was in 150-160 range in Jan-16.

Companies will post better result in q4 yoy.

I read one article in NewYork times, Chinese govt has put in significant effort in reducing pollution emanating out of Coal Powered Power plant and also steel plant. Point is focus on reducing Pollution related industries.

Has anybody access to the following meeting notes or brokers’ notes 'Bodal chemicals organised an instituational investor meeting with Religare Insitutional team and DSP Black Rock on 6 March

2017 ’

Kindly share.Important to hear in backdrop of Chinese production etc

Bodal chemicals adds 250 Tons/ per month capacity for dye intermediaries through an acquisition. The management commentary in the press release about chinese supply problems are also bullish. The acquisition is funded fully by internal accruals.

This is a fully compliant H acid plant with zero discharge and capacity of 250 TPM. Acquisition cost is 4.1 cr inr PLUS 35 cr of debt. (Debt figure arrived at through the following fact presented in the same release)…

Unsecured loan of 45 cr has been provided to this company for clearing all of its debt and building a Vinyl Sulphone plant (350 tpm) at a cost of 10 cr.

So, for 70% equity, acquisition cost is 4.1 + 35 ~39.1 cr. So, total valuation for this acquired company should be close to 55 cr? Revenue of this company is 75 cr (Feb 2017).

Anyone knows the cost to setup a greenfield/brownfield plant for H acid? I would like to compare why mgmt has made this acquisition. Probably they saw value here vis a vis augmenting capacity of their existing plants… by how much?