Hi Advait,

Yes I still own Biocon, it is among the biggest positions in my portfolio.

I think the consolidation with the downward bias you are referring to is based on the technical and charts?

As far as the business is concerned, I am very bullish and the opportunities going forward are huge, it is also good to see that they’re investing heavily deeper down in the pipeline, so its not just Trastu Pegfil and Glargine that they’re betting the company’s future on. The current period is where they reap the rewards of investments made over the past 5-6 years.

4 Likes

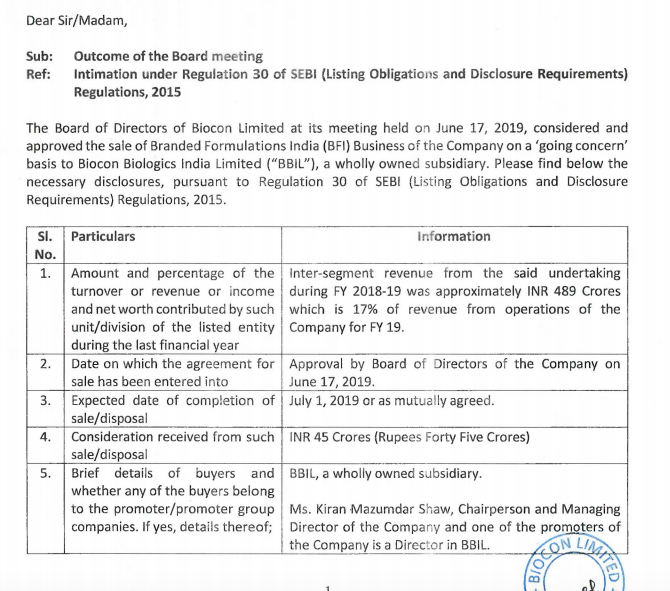

Hi Folks, could someone please help decode what this means ?

Part of business sold to another subsidiary, how would that help the company ? Will it have any impact on Biocon’s consolidated revenues ?

Biocon-Announcement.pdf (738.1 KB)

Yes, I would like to know the rationale for such a transaction as well!

I have no idea…

No impact on consolidated numbers for now. BBIL is a wholly owned subsidiary.

Management has hinted at potentially spinning off BBIL in the near future to fund the 2nd phase of Biosimilar development (Post 2023 launches).

I think spinning off BBIL will be value accretive as the resulting entity would have a superior return profile.

3 Likes

Its more like the Sun pharma spinning of high specialty business as separate stock Solara. So considerable growth / revenue will come from the new spin off company. Where as the old company will do the regular operational business ( less profitable business). What i see with Sun pharma - stock went down hill, however the spin off candidate solara double over a period of 1 year. Expert can correct me if i am wrong the understanding on Pharma space.

What Biocon promoter told publically is

They want to spin-off Biologics business separately … As they want to unlock more value for share holders and Biologics is such a business that it will require continues R&D investment on each and every molecules (may be Sandoz spend 50%)

They have appointed Christiane Hamacher as CEO of Biocon biologics India Ltd … may be first step for this

So it’s personal call on promoter integrity between Sun and Biocon

We all know very well that SUN pharma fall was due to 172 page Whistle blower complaints

Thanks

Ashit

Ogivri getting launched last week of June

1 Like

Just a side point, the 7 billion size is for world wide sales and the new launch is just in Canada so they are not targeting the entire 7 billion sale

The other markets already have the generics and hence that revenue is not incremental

British Columbia a province in canada is switching patients from originator to Biosimilar. If they recommend the same for Ogivri, there is a significant opportunity being the first to launch Trastuzumab.

Eagerly awaiting the launch in US which is the biggest market. World over regulators are encouraging use of Biosimilar to control Health care costs. Biocon is in a sweet spot to capture this trend in the global pharma industry.

3 Likes

The situation in Canada is very similar to Europe - high uptake of biosimilars. In the USA the situation is different for bizarre reasons and the uptake of biosimilars (and complex generics) have been much lower than expected.

I had assumed net profit of 30 crores from Canada (refer to my post a few pages above) but it will be higher because of the higher and compulsory use of biosimilars…

1 Like

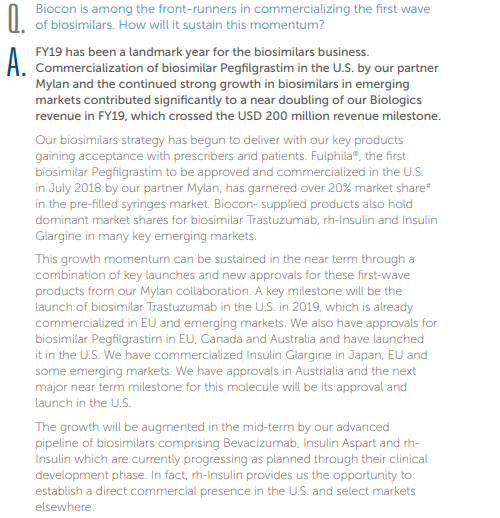

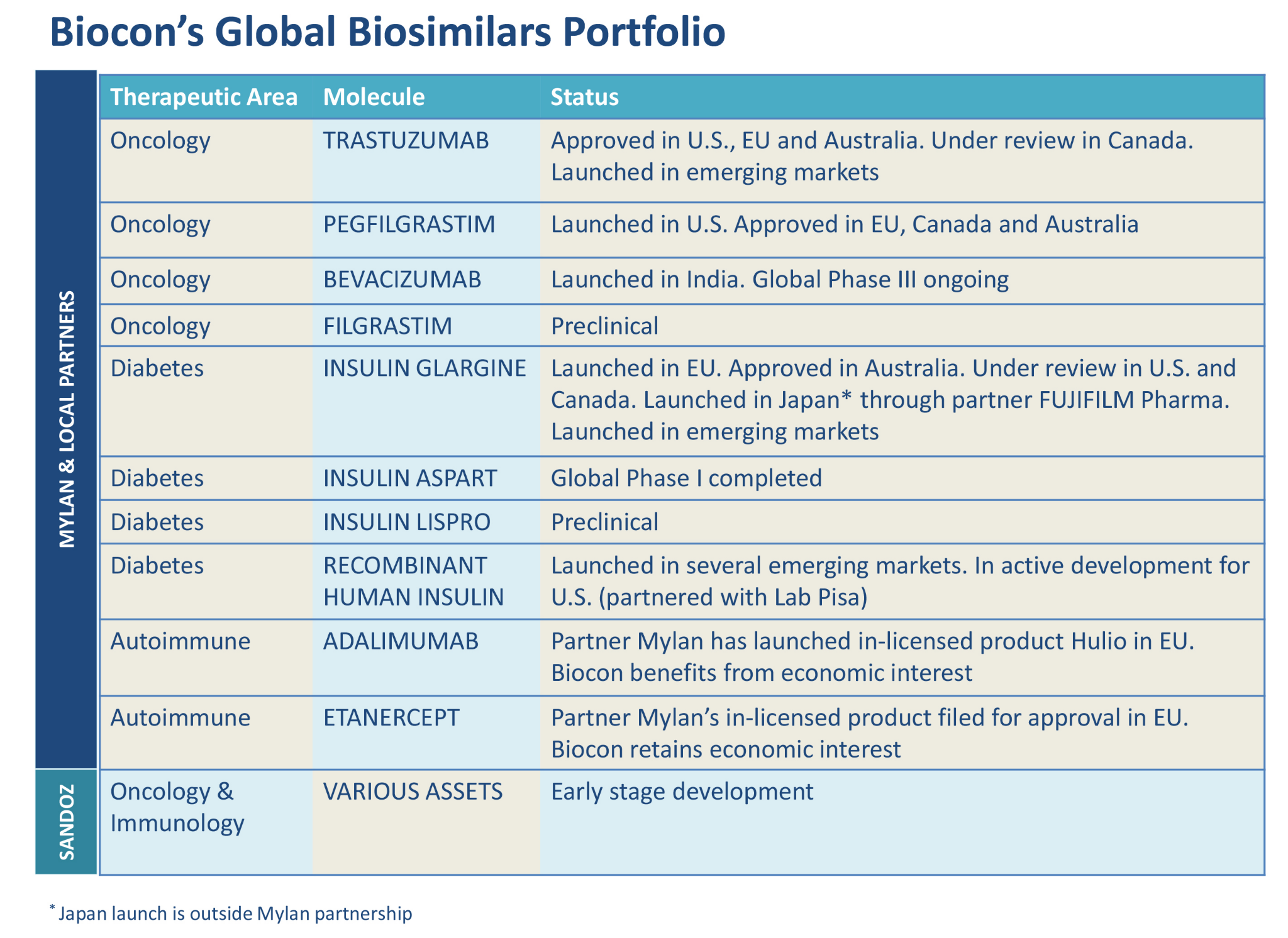

Biocon continues with Emerging market/EU launches before the US launches through partners and commercialization.

Extract from the Annual report:

This growth momentum can be sustained in the near term through a

combination of key launches and new approvals for these fi rst-wave

products from our Mylan collaboration. A key milestone will be the

launch of biosimilar Trastuzumab in the U.S. in 2019, which is already

commercialized in EU and emerging markets. We also have approvals for

biosimilar Pegfi lgrastim in EU, Canada and Australia and have launched

it in the U.S. We have commercialized Insulin Glargine in Japan, EU and

some emerging markets. We have approvals in Austrialia and the next

major near term milestone for this molecule will be its approval and

launch in the U.S.

The growth will be augmented in the mid-term by our advanced

pipeline of biosimilars comprising Bevacizumab, Insulin Aspart and rhInsulin which are currently progressing as planned through their clinical

development phase. In fact, rh-Insulin provides us the opportunity to

establish a direct commercial presence in the U.S. and select markets

elsewhere.

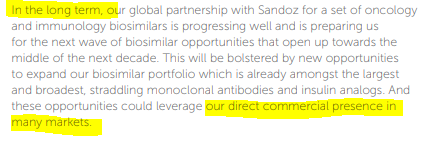

In the long term, our global partnership with Sandoz for a set of oncology

and immunology biosimilars is progressing well and is preparing us

for the next wave of biosimilar opportunities that open up towards the

middle of the next decade. This will be bolstered by new opportunities

to expand our biosimilar portfolio which is already amongst the largest

and broadest, straddling monoclonal antibodies and insulin analogs. And

these opportunities could leverage our direct commercial presence in

many markets.

1 Like

`[Biocon-gets-USFDA-observations](https://www.dsij.in/DSIJArticleDetail/ArtMID/10163/ArticleID/8270/Biocon-gets-USFDA-observations)`

Biocon has been issued 12 observations by the USFDA for its assembly facilities in Malaysia. Despite the news, the stock price of the company increased by 1.5 per cent.

I was expecting to add with today’s fall, but not sure why it went up.

If you have 5 to 6 years horizon , then I may say opportunity is really very large

Most of there biosimilars are in oncology and autoimmune, and chronic disease now if you see sales of top molecules in the world you will realise the opportunity

Now it’s difficult to predict how much share they gain over period of time , so difficult to predict cash flow and difficult to value

From latest AR

"In FY19, we incorporated Bicara Therapeutics based in Boston, U.S., as a wholly owned subsidiary of Biocon to focus on developing a pipeline of bifunctional antibodies that exploit the recent advances in immuno-oncology. We believe bi-specifi c antibodies are the next big opportunity as they offer an advanced therapy option against cancer.

want to know more about Bispecific antibody the you can read this

https://www.google.com/amp/s/heraldspace.com/2019/07/10/bispecific-antibody-therapeutics-market-to-register-steady-growth-during-2017-2025/amp/

If youread this thread will roughly get answer to your question

Thanks

Ashit

Disclosure Invested in it and by profession in medical field

9 Likes

Any reason why they are developing the pipeline on Bifunctional antibodies in US instead of India?

This field of medicine/pharmaceutics is very advanced and there is no expertise in India in this field. USA and China (specifically for CAR-T cell therapies) are the leaders in this therapy. So they are doing the right thing by advancing this in the USA. Also, this is different from Biologics! Very confusing even for medical people…

3 Likes

Looking at current business profile, biocon may split into two business verticals - biosimilars and pharma.

The opportunity, size and prospects outweigh the other by a huge margin.

Their tie up with Mylan for marketing is a big plus. They may be doing over 4000 Cr in biosimilars alone in next three to four years. If all goes well this may lead to windfall gains for biocon and its shareholders.

The agreement with Mylan is on profit sharing basis, on marketing margins which is over and above the nominal margin they have on manufacturing. Good chance of crossing 1000 Cr in 19-20.

In pharma their focus will be on filing ANDAs for next four five years so long way to go on that front. So if it splits in near to mid term, better to reinvest the realization in biosimilar if possible.

Discl: bought some. And look to add as and when possible. My opinion may be biased, do your own research.