Bhansali Engineering Polymers - AR Summary 2021

https://drive.google.com/file/d/1u1LgQA2SgTzix7x3p4mFhwGcGgcSDKrt/view?usp=sharing

Bhansali Engineering Polymers - AR Summary 2021

https://drive.google.com/file/d/1u1LgQA2SgTzix7x3p4mFhwGcGgcSDKrt/view?usp=sharing

@basumallick the company has mentioned they developed 100 grades, out of which 43 approved and 15 commercialized. Again, they say one abs grade commercialized for Bajaj. Could you please clarify the difference between these two statements. I am confused between color grade and abs grade.

If anyone has attended the annual meeting, could you please share the minutes of it.

Thanks in advance!

Hello ,

I am new to tracking this company. Just wanted to know any reasons for a such a huge improvement in OPM % of the company from 6% to 35% YoY.

Is it just because of foreign exchange fluctuations?

Are these improved margins sustainable or was it a one off thing? Can we form a long term opinion by tracking any available data?

(Sorry if this is too basic)

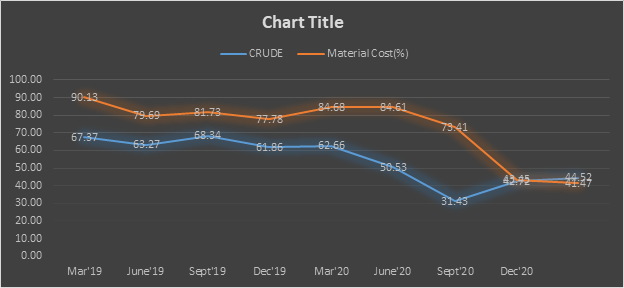

I was intrigued by the huge increase in OPM in the last few quarters. I wanted to know whether there is any correlation with crude prices. So I tried plotting material cost as a percentage of sales to Brent crude prices. I have used the average crude prices of the previous quarter to reduce the effect of inventory outstanding.

Eventhough the management has claimed that crude prices doesn’t affect their OPM, it looks like crude prices directly affect the cost of raw materials. There is a deviation seen only in 2020. It is seen that the company carried a high cost inventory of 208 crores as on March’20. Due to covid crisis crude prices fell sharply, but raw material costs remained high due to the old inventory and company was able to make a sale of only 99 cores in Q1’21, so the high cost inventory spilled into Q2 dragging down OPM in Q2 as well. After the inventory was exhausted OPM jumped up significantly in proportionate to crude prices. But crude price has started moving up in Q4’21 and is at around $76 currently. The Q1 OPM may still be good due to the inventory of 113 crores as of Q4’21, But the company’s margins may come under severe pressure from Q2’22. The company however did well to improve its topline significantly.

We will get a clear idea of how much cost the company is able to pass on from Q2’21 only

Disc: No investments

Good one @Jose .

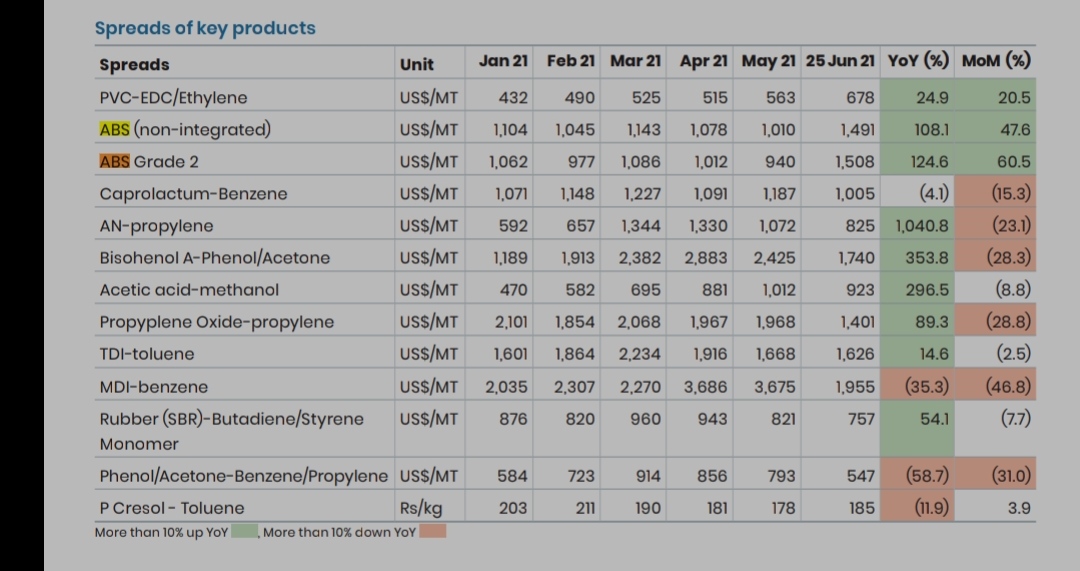

On the other hand the prices of ABS have also run up a lot. As per Tijori ABS prices are up 100% in the last year even after the recent consolidation. With the increased electronics manufacturing in India along with India growing as an export hub for Autos, the demand could be really high keeping the prices in check for next 1 year until supplies increase.

Other thing I remember is, fluctuation in exchange rates affect more than crude oil prices as per the promoter.

Disc: Invested and biased.

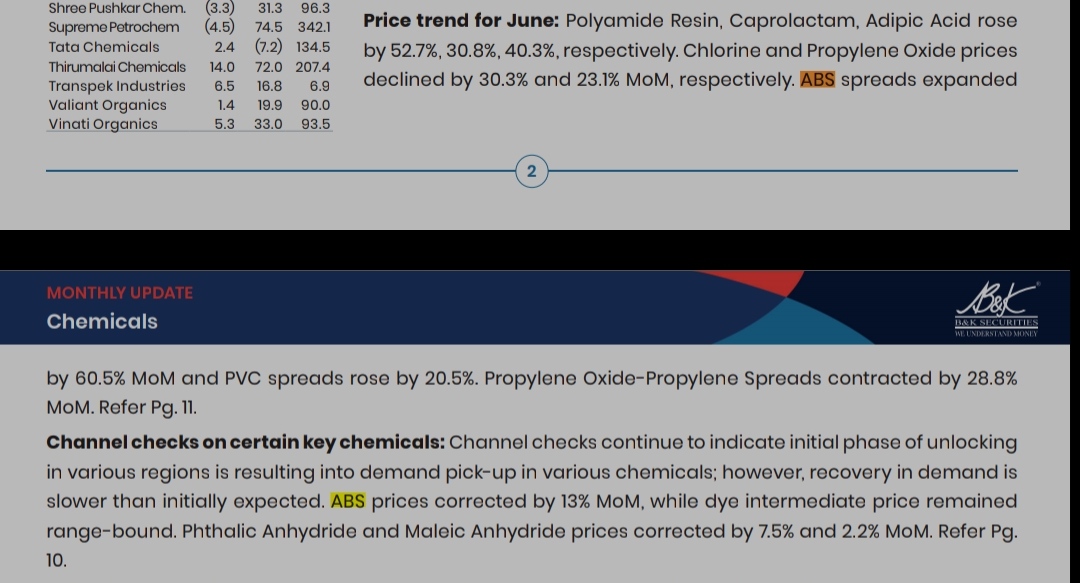

As I shared previously ABS prices remain firm at $2500/MT as per the latest sunidhi report.

This was one of the reason why I wanted to check it up, to make an entry, but from what I understood margins have a very good correlation with crude prices.

As you have said prices as well as demand for ABS has gone up which is evident from the topline growth, the company was able to clock better sales in the financial year even after a washout in Q1’21. But you have to note the fact that crude prices have almost doubled in the past 6 months. The margins may just drop a little to 35 % as you have said, but there is a huge uncertainity

I still doubt if margins are correlated with crude prices. As per my understanding styrene prices is an important driving factor. And 85% raw materials is imported and hence and exchange rate changes will have a huge impact.

As per the latest report from B&K securites ABS spreads have expanded by 50% in June alone, where as crude oil prices are at 6year high now. If they are too dependent on crude prices I don’t think spreads will expand by 50% in a month.

Disc: Invested and biased.

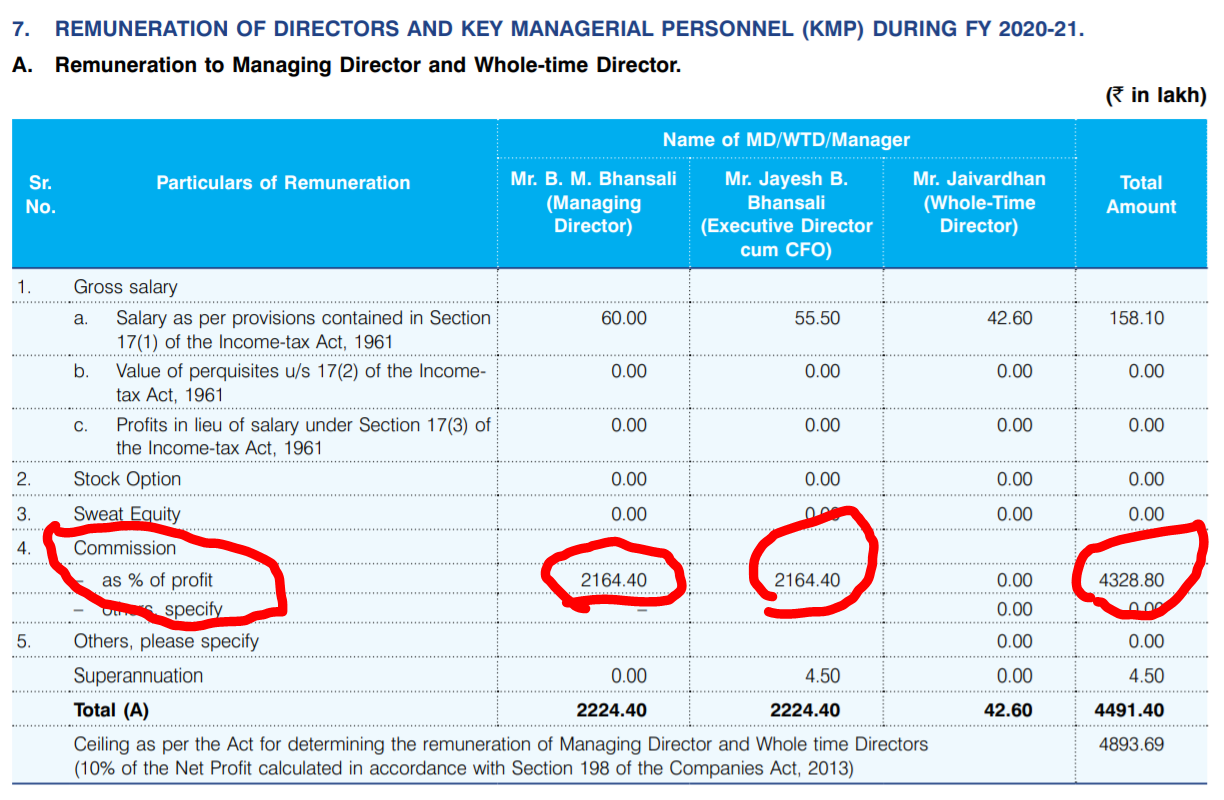

Margin Increase by 42.25%

But that will be from CSR. Not from individual’s account. correct me if I am wrong.

I am wary of promoters taking huge profit linked commissions or ESOPs. Especially in case of commodity companies, the fortunes are dependent to a large extent on commodity prices over which the management has no control. In such cases, it is a good idea to see what the management said when commodity prices were low and results were bad. Usually, you will find them blaming global slowdown, low commodity prices or other external factors for poor results. During good times, they take the credit (and your money too)! There are many such companies, of course. It is upto the investors whether to ignore this or not.

Excellent results

While not following this too keenly, on a slightly related note IF Bhansali is using styrene that is 100% imported, the following info might be useful both as a source or as future competitors who may enter the same space.

Again, this is a few years away and also not sure whether monomer styrene is what they use

They are the users of styrene monomers, they sell ABS. They have been importing styrene monomers as there is no producer of it domestically.

How do the seasoned investors here see the environmental conservervation and green movement impacting ABS and SAN consumption trends? Also, how do you think ESG investing trend will impact investments in the industry?

in same situation as you…got the stock through a filter on screener.in. The indicators looked good. But now after reading the whole story, there is something definitely fishy - time and again ppl have been asking questions about how they are able to get good margins and there is no solid , sustainable explanation. Plus there is this huge promoter remuneration. Thats why the broader market is giving it a miss, even though sales are rising since 2017.

Brown Field ABS Expansion Project: