Some selected branches are even open on Sundays.They provides free gifts to their customers (mostly all the bottom of the pyramid) like pressure cooker, non stick pans etc. It’s a huge hit with our maids

4 Likes

incidentally, same author has written a book on HDFC Bank - posting link for reference https://www.amazon.com/Bank-Buck-Story-HDFC/dp/8184953968

I would not give a lot of credit to such books - since, these will mostly carry one sided view. However, Tamal is a journalist (as I have read), and provides some interesting anecdotes at the time of bank formation. I tend to read such books more to understand the culture and organizational DNA rather than try to find any other meaningful financial insight.

4 Likes

Thanks, Appreciate your response!

I skimmed through Bandhan bank and AU Small finance bank. In all terms Bandhank looks pretty strong. Earning growth, Cost to income 35%, NIM ~10%, CASA ratio, low cost funding.

Bandhan bank looks very promising buy only doubt is about Promoter stakes sale. If it has to be dropped to 40% what will happen to stock price.

1 Like

Assuming they are smart enough, they will reduce stakes via some acquisition …

1 Like

Just bear in mind in your comparisons that AU sfb is going through transition to sfb and has higher cost to income ratio and lower ROE this year… what is important in the comparison is 3-5 years picture and how will the picture be post transition… also bandhan is primarily micro-credit(un-secured) while AU is secured credit.

Pointing out differences, not advocating one stock over the other.

3 Likes

Thanks Raman. Completely agree I don’t know any other micro credit company to compare so skimmed through MAS, AU and Bandhan to have relative strength idea. But you are right they are not apple to apple comparison.

@RamanTiwari I also like Bandhan due to their concentration in the East and NorthEast region where un-bankend population is high and Bandhan being strong player will maintain their earnings growth for a longer period.

Also if you look at the GNPA they are not much for unsecured loan so it is providing both benefit of higher NIM along with reasonable risk.

Most of the lending of Bandhan bank is in unsecured and for self employed which is having less competition. Bandhan has the advantage of being bank to cater these target customers in more cost effective way. I think there is definitely competitive advantage for bandhan bank and there is huge market as we can see several micro finance companies are doing well.

I think Bandhan target market size is big and they have competitive advantage. I am not sure how long this competitive advantage will last but can be assumed for 1-2 years.

1 Like

Bandhan Bank Annual Report 2018 Notes

Hi

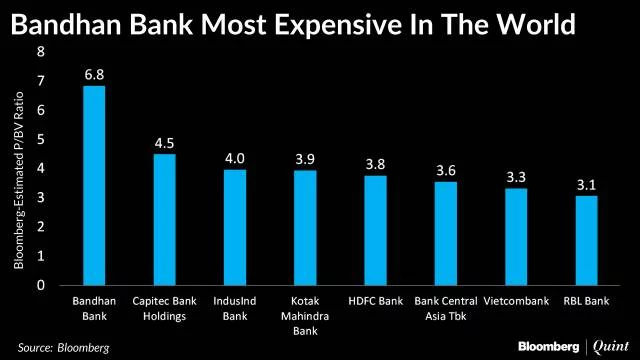

Bandhan bank leads the pack of the overvalued banks globally ![]()

Regards

Deepak

4 Likes

Hi Deepak,

Do you think this is over-valued or its OK based on projected earnings growth and “unmatched” NIM / ROA / asset quality it has?

Best Regards,

Vishal

The question you should be asking is why are they interested in buying PNBHF if there is a vast untapped market available for them where they can generate NIMs of 10% plus?

3 Likes

Since they r converting to bank,10%Nim would definitely moderate

Bandhan has already converted to a bank (unlike SFBs which are still in the process). Their high NIMs is because of their asset mix - 90% of which is in MF. Their own housing finance book hasn’t picked up. I would think they want to diversity their asset book - buying PNB HF would give them a ready made business. However, I find it quite interesting - the only parameter common to PNB and Bandhan is high growth rate, on others (ROE, RoA etc.) they are quite different.

1 Like

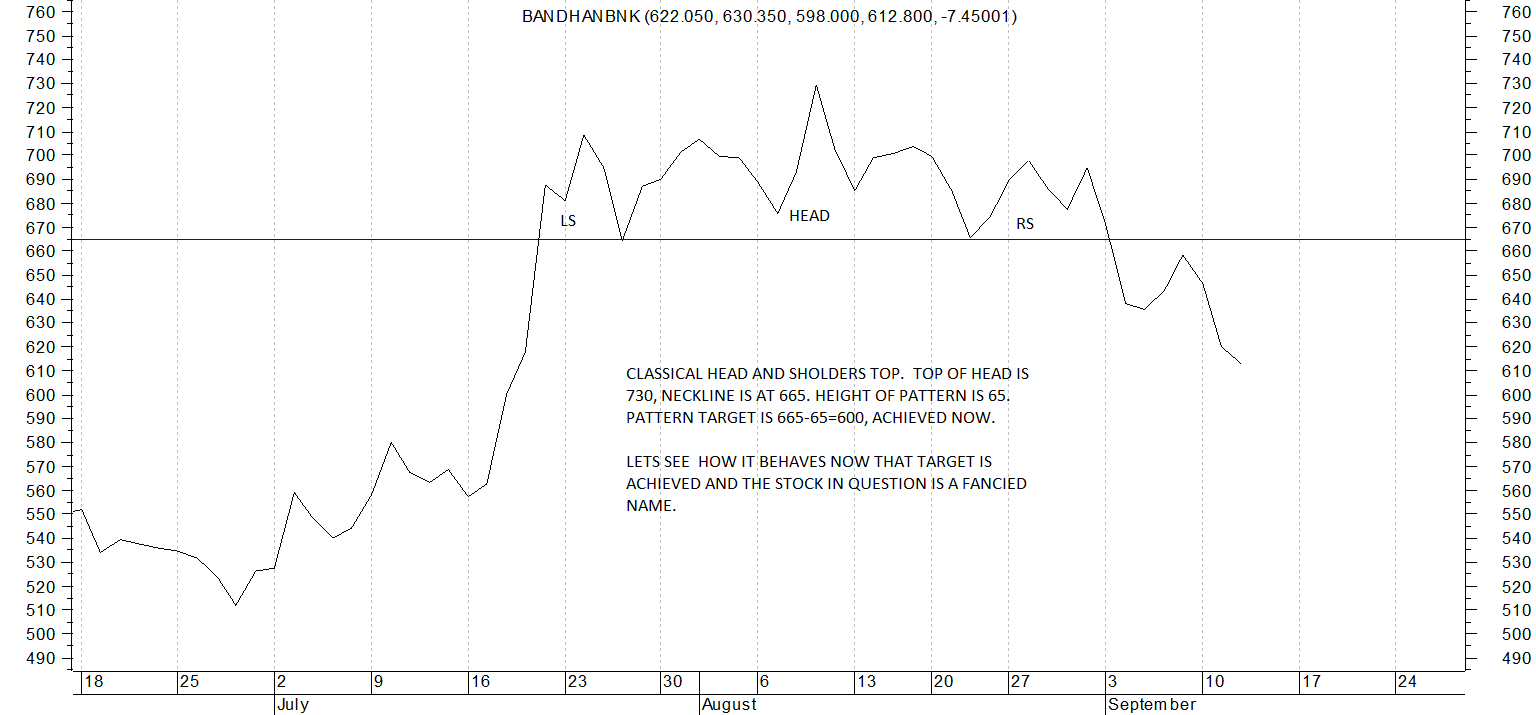

Relief for Bandhan shareholders!

1 Like

3 Likes

When you say tat target achieved at RS 600, what exactly it means to a retail investor?Can it go down further or it has come to interesting level to keep watch/buy?