Hi

As expected BFL RBL crosses 10L cards.

Rgds

Hi

As expected BFL RBL crosses 10L cards.

Rgds

Solid performance continues

Few points from MD interview with BQ:

Continue to manage growth, not chasing market share.

Growth was strong across all business segments.

To maintain 25-27% of balance sheet growth and 23-25% of net income growth.

May raise capital during capital during Q4 of FY20.

Cost of borrowing remains at 8.3%.same as in Q3

AUM growth for FY20: broad based growth …most business lines growing at 25-27%.

Provisions expect to be within 1.4 to 1.6% of avg assets.

Added 8 million new customers in FY19.

Present across 18,00 cities, will expand to 20,000 cities. Expect 5 to 7 millions new customers addition.

Housing Finance: growth could be stronger… watching liquidity situation…remain committed to 3-3.5% of ROA and 18-20 of ROE.

Liquidity scenario of industry: more structural compared to previous liquidity crisis.

Excellent Analysis . I hope all NBFC give such analysis of their PF .

While overall it seems to be a great result however there are some small concerns

PCR has fallen from 70% to 60% . If they had stuck to same PCR ie 70% then they would have take a hit of 182 Cr in provision .

But it also meant that impairment increased from 215 cr to ( 375+182 ) cr ie increase Gr of 159% vs loan Gr of 41% and Income gr of 52%

I am not sure if this one period blip on account of some large one off loan . If not that this growth in bad debt is a cause of concern

I suppose this is due to change in AS. In IndAS, provisioning is to be done bad on expected credit loss and not on gross numbers. So I expect them to maintain PCR at 60-65% level only.

All have price targets way below the CMP…everyone says premium multiples cant sustain…are they not saying this from last many years?

I attended the conference call of Bajaj Finance. Some of the points I noted on the call:

• Pretty strong quarter for the company. Customer franchise increased by 32% during the year. During the quarter added 1.92 million new customers.

• Since the liquidity crisis started company added 17000 crore AUM post September, 2018 to March, 2019.

• RoA were very steady.

• Deposits grew by 69% during the year

• Overall growth was pretty granular across the various segments.

• 1000 crore of capital infused in Bajaj Home Finance. Satisfied with the mortgage lending business performance.

• Company received investment grade rating of BBB- from S&P for its ECB program. All set to complete the document in May, 2019. Will raise entire USD 750 million this year.

• Focusses on granularity of portfolio. Augment profitability and reduce risk.

• Portfolio quality continued to remain good. Gross NPA would have gone down by 8 – 9 bps excluding IL&FS write off.

• Continue to be managed well. Very well placed. Sitting on 7000 crore of cash and cash equivalent. Partnership with RBL continue to grow.

• Released – we will start to talk about competitor activity on retail side? Released on slide 51, 52 and 53.

• Significant slowdown in consumption – discretionary and non discretionary. How do we look at it on maintaining growth? Consumption outlook does seem slower than it was in November. It is also very patchy. Electronic retailer in April reply is good while in May its poor. Focus on strategic expansion, geography expansion and wallet share of clients. 35 million customers represent one of the largest share amongst retail clients. Our share of wallet is very low in customers. Continue to focus on geography, risk management and analytics.

• Credit card tie up with other banks? Globally its common to work with multiple partners. Happy with RBL. Continue to grow rapidly. In long term, its possible that we may have one more partner given our ambition to be 3 – 4 top card company in India.

• Mortgage business – 34,000 crore assets. At what stage will you consider to spin out the business? What RoA are you targeting? We look at 17000 crore of assets sitting on BFL will wind down. We look at internally as 34,000 crore of assets on home mortgage. Margins will be higher if we transfer the entire 34,000 crore portfolio in home mortgage. Cost to income ratio is still higher than industry. On costs we have done whatever we had to do. It is now scale which will take care of the ratio. Industry wise, we are 1.5% of the market. If we are not 8 – 10% of the industry size, it doesn’t make sense. But we are not in hurry. We will build down the business in few years. 14 – 15% RoE with 8 to 9 times gearing is good in mortgage business. We don’t want to compromise risk for higher RoE and manage ALM well.

• ECB – indicated fully hedged cost? Hedging costs are different and change continuously. Fully loaded costs will vary. We will do fully hedged – interest and principal. We expect to be lower than our current cost of borrowing.

• Positive ALM while competition are struggling to lend are you gaining market share? Doesn’t give time to think about market share gains. Essentially complete with leading private sector banks. That hasn’t seen slow down. Auto Finance business we are seeing market share gains. Competitor activity is reducing at counters. Other than that we haven’t seen reduction in competitor activity.

• Raising ADR/GDR or raising debt in future? Yes. We have considered.

• New disclosure on overall leverage risk. Professional side we have seen jump by 25 – 30%. This is just unsecured exposure but we will have some secured loans also. Any idea about overall household leverage? Yes. Data is available. Unsecured loan leverage is more important since there can be multiple loans. This is about managing risk and if there is risk, we will take action. Top 15 cities in India – number is very different and very pronounced – if we go lower it is very less pronounced. Action ability is Top 8 cities represent higher risk. This is not for analytical perspective but on actionable purpose. Our exposure to this category was 11 lakh per person and now also is around 11 lakh per person. Business loan exposure has actually gone down per person/loan. Business loan any cut on the business? Exercise done by us quarterly. LAP – IL&FS NPA increased. Otherwise it is much lower.

• Mortgages – Composition of the book – 36 – 38% over the next 3 years. 3 – 3.5% RoA and 16 – 18% RoE for the overall company.

• Cost to income – delivered 35% cost to income which is lowest we have seen. Still some scope for mortgages to go down cost to income. Can cost to income go down further? Realistically, income growth will reduce cost to income. Other than mortgages we are looking to cut expenses. Cost to income should steady now from 34.5 – 35.5%.

• Banking license in future? Looking for acquisition for any bank? Thought process in place for that? Cant say yes or cant say no. Clear structural distortion in the sector and in general whatever I read. Two important pillars of financial industry going through distortions. They have to get fixed in the short term by set of actions and in the long term by reform. As we navigate through this we will continue to evaluate if its appropriate to think about a bank.

• Any segment where there are potential risk? Top 8 – 10 cities continue to represent much higher risk than rest of India. They represent large opportunities but high risk too Rural will continue to grow higher than top 10 cities.

• Leverage risk assessment – where are we more comfortable? 67% of our customers are existing customers. If you are lower risk customers, we will approach you now but for a high risk customers, we will approach after you have paid the loans. Unsecured portfolio represent rightful representation of risk. Around 10% of our B2B customer take personal loan from us.

• Incremental cost of fund during the quarter? 8.2% consolidated cost of debt. We continue to raise money from CP, bond market and banks. Dropped 15 bps rate of interest for deposits. 3000 crore NCD raised at rate of 8.5 – 8.6% during March, 2019.

• SME portfolio – quality of book deteriorating as per other banks. Our view? SME remains volatile. We deal with micro SMEs. In general we are quite ok ending March, 2019. They remain more volatile of the segment. Watch them carefully and act in agile manner. Market like Delhi, 2 years ago, the portfolio has gone down by 20% in 2 years while overall loan book has grown by 50%. Top 15 markets out of top 50 are in early warning zone. Increasing credit cost for us because of it? At peak of demonetisaiton it went to 230 bps. Currently its 200 bps. Its tough to scale business. As you scale, you go towards naturally more volatile end of scale.

• Consistently, overall coverage has been improving. What does it mean for asset quality behaviour? We are seeing on an aggregate basis, better portfolio entering the year than closing the year. Consistently, the coverage has increased. Early warning indicators that we are seeing, might reflecting in NPAs? If market starts start to behave erratically, our nos will also be impacted. We will continue to improve risk management. Doesn’t mean that if our balance sheet growth, loan losses should grow. Over 24 month period, there will not be a self-employed home loan portfolio sitting on our balance sheet. Want to identify small pockets of issues and work on it.

• Fee income to PBT ratio? Should be able to hold at it at current level with plus/minus 50 bps. Fees income is now amortized over the tenure of loan.

• RoA – consistently at 4%. With increasing proportion of mortgages in our total portfolio, what RoA are we are looking at? When this strategy gets implemented, RoA will steady between 3 .3 – 3.5% with RoE of 18 – 20%. That’s been so for the last few years. We will deliver it in next 2 – 3 years. RoE – as true risk in mortgage business goes down, leverage in housing finance will go upto 8 – 9 times. If sum of parts gets delivered, we will deliver 18 – 20% RoE. Premium for Bajaj Allianz Life and Bajaj Allianz General? Work with 8 insurance companies. Premium we originated overall was 950 crore. Similar growth of balance sheet for premium of around 40 – 45%.

• Colour on developer segment? What is the stress? Total book is 1200 crore. General market we will not be able to provide an update. Overall market is 500,000 crore and we are just 1200 crore. We continue to work at ticket size of lower size. Represents 140 relationships we have. Project don’t sanction above 45 – 50 crore with average ticket size 25 – 30 crore. Not there in North India. We are present in western and Southern India. Not the first lender. Average rate is 12.5 – 12.75%. Our exposures are lower. Focus on velocity. If we don’t get the share of home loan portfolio, we are not interested. 38 -40 lakh is our average loan for home loan and our focus even on developer is for homes around 60 lakh. Don’t finance any project with average amount of 75 lakh.

• 30 days plus bucket in consumer, lifestyle etc has gone up sequentially. Anything to consider? Nothing to read it in that. We are not observing anything materially. In lifestyle, this is a yearly phenomenon. In Q4 there is some bump up post Diwali season in Q3.

(Disclosure: Invested)

Net Income projection 2023 based on some numbers quoted by Rajeev Jain

Bajaj Finance wants to be among the top 4-5 mortgage players in India by acquiring a market share of 8-10%. The Housing Finance market itself is now 20 lakh crores. Also Jain mentioned mortgage portfolio will increase to 38% of AUM compared to around 30% now. Doing some number crunching here.

Size of the Mortgage portfolio in 2023= 2000000 Cr X 8%= 160000 Cr

Overall AUM = 160000/.38 = 421052 Cr

Net Profit to AUM in 2023 (currently 3.44%) = 3%

Net Profit in 2023 = 421052 X 3% = 12632 Cr

4 Year CAGR in Net Profit= 33%

If the company manages to achieve this with good asset quality the share should be trading between Rs 8000-10000 in 4 years

Disclosure: Big exposure to Bajaj Finance through Maharashtra Scooters

Cud u explain how have u taken bajaj fin exposure thru Maharashtra scooter? Any risks there? Also in Bajaj Fin?

Maharashtra Scooters derives 70% of its value from Bajaj Finance so it should track performance of BFL pretty strongly. There is a non-zero probability of liquidation/narrowing of discount once the shares are transferred from WMDC to Bajaj Holdings (not sure if you are aware of the litigation). Since I have a large position it helps with diversification as it has stake in Finserv and Bajaj Auto

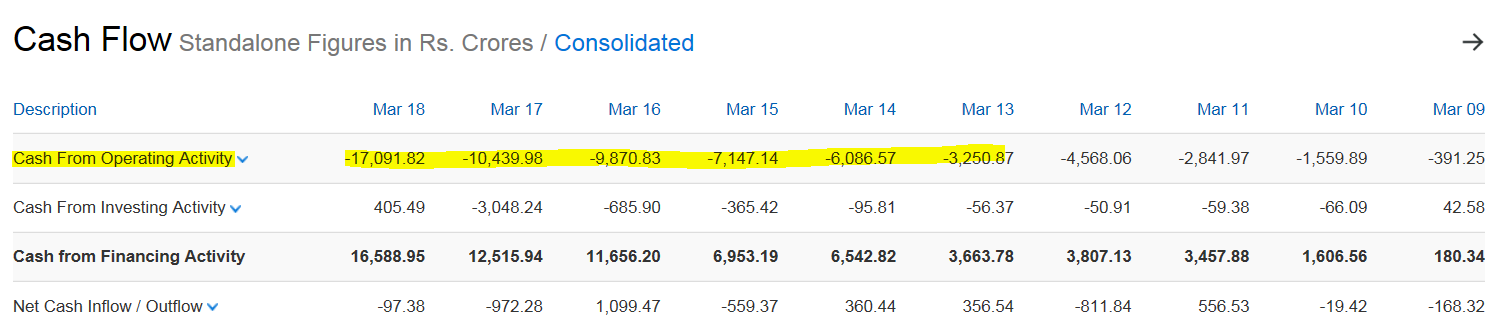

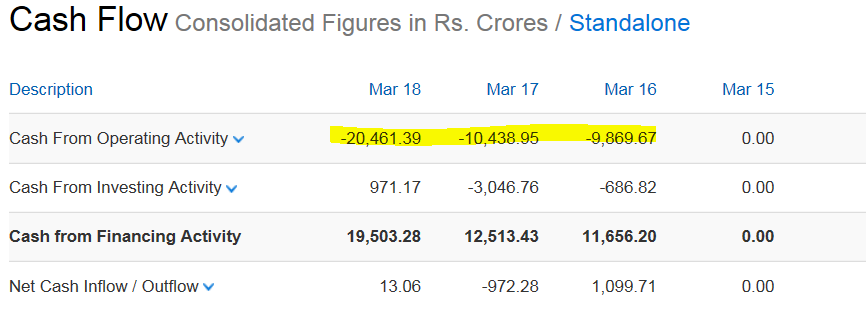

Hi , Can any one help me in understanding why operating cash flow is consistently negative for Bajaj finance over last 10 years ? generally its not considered good , but is it common for financial businesses ? Can any one please explain this.

For banking companies, cash comes in the form of interest. So their Cash flow would be coming in Financing activity. Manufacturing co’s service co’s cfo will be seen.

Yes it is common for financial businesses. It is explained here:

Can Bajaj Finance maintain the growth trajectory for next 5 years? Is it fairly valued /overvalued presently? Would like to solicit opinions of fellow investors.

Bajaj Finance is such a matured & ahead of curve business, which does not require so much of thought process, as far as Performance Evaluation is concerned.

Management -->Rajiv Jain-Sanjeev Bajaj duo have excelled by now in mastering the gauging of the Business Potential & Opportunity Size & they are always keen to tap the same & have been able to do so successfully till date.

Also they already are way ahead in Planning the next avenue of growth, when competitors start following their execution of Ongoing high growth Business Verticals.

Valuations lens is what is typically different for a different eye. For me considering the Growth Potential & Management hunger for Growth, it will always enjoy scarcity premium.

Also during turbulent times, to the likes of past year or so, smart money always chases these kinds of Predictable Businesses. Investors make a beeline to grab such wonderful businesses to ensure permanent Return of Investment ( & avoid Loss of Capital).

Their ROA is the best in the Industry.

Please do your due diligence. Its totally my Point of view & I deserve a right to be wrong.

Adding to what @bsahni has mentioned.

Bajaj Finance is much more a FinTech than traditional NBFC. Only tech and analytics and AI can stay in this business as long as a black swan event turns all your AI into dump. And only traditional approach cannot survive if it doesn’t make use of technology in these times. BF has blended lending practices of traditional/conservative NBFC with technology well.

Opportunity size is still to catch with their current business. But we can expect the growth rates to go from 35 to 25 to 20 and stabilize there in next 3-5 years. No one can grow at 30% forever as we know with example of HDFC Bank.

Valuation here is also tricky. It has lot of qualitative and trust aspects along with numbers. And then BF gives surprises also. For example, it’s FY18 EPS was 47 and analysts all built up targets with 30% growth and EPS of 61. Price went to 2900 at which point it was very expensive trading at almost 50X FY19. Then stellar results followed and FY19 EPS is actually close to 70. Stock crossed all time highs and trades at 50X trailing and 39X FY20. Still expensive but the valuation will stay elevated as long as growth is there.

Disc - Invested. So naturally my views are biased.

What separates Bajaj Finance from other NBFCs?

1) Management Bandwidth - They have champions in consumer finance starting from Nanu Pamnani (Ex Citi Banker, who was BTW instrumental in getting Aditya Puri in Citi Bank then), Rajiv Jain (Ex GE Finance) and of course Sanjeev Bajaj who has done better than his elder bro and charismatic father. They thrive to extend the management team by appointing independent CEO if the division overgrows (eg Housing Finance)

2) Cutting Edge Technology - They had cream of the ex- e-Serve team, which was captive unit of Cit Bank. They have built on that to latest skill in FinTech, as mentioned by Nikhil. There are not too many companies particularly in NBFC space which makes such extensive use of technology in their core business. This is instrumental in keeping them ahead in the game.

3) Structure of a Bank with lower regulator oversight - The kind of products they offer are no less than a full fledged commercial bank with loan book higher than most of the smaller Banks. They have benefit of extensive dealer network of Bajaj Auto on which they piggy backed their branch network. (I don’t think the cap of 15% ownership will make Bajaj Finance interested in being Bank because they can do 75% of what bank can do and for rest 25%, they have partners. (Already Kotak is in fight with RBI over the ownership issue)

4) Partnerships - Not being a bank is handicap at times such as inability to offer Credit Cards which they have overcome by partnering with RBL. Also in payment network partnership with MobiKwik.

All the points by fellow investors are appreciated. Thanks for the response.

However, can these strengths of Bajaj Finance be replicated? If someone with deep pockets enters the business, can the pole position be affected?