It cant be true,as far as I know ,they give payouts to retailers for canvassing loans

Normal business practice all nbfcs or any business follows

I would like to refer you to this post - How to analyze NBFC companies?. The scale of operations in housing loans is much bigger. The OPEX is smaller (in percentage terms) as compared to other asset classes like gold loans, vehicle finance etc. NPAs are lower. At the end what matters is RoE (return on equity). That is high for housing finance NBFCs even though they work on lower spreads.

1 Like

Thanks. 15% cost income ratio for HFCs vs 40% for Bajaj Finance was what I was missing. Also they are Cross selling different types of LAP products (Flexi, Hybrid, Traditional LAP) with mortgages and these products have higher yields (about 1-1.5% higher).

2 Likes

Also pure play HFCs are leveraged 11:1 compared to 4-5:1 for other NBFCs that helps them to achieve 20% kind of RoE

1 Like

hi all,

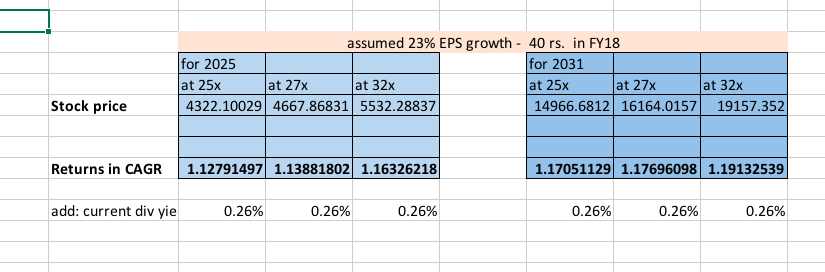

I hope all agree BajFin a secular growth story on the indian consumption theme. Plus BajFin seems to have a big wide moat which has been discussed earlier here. Now P/B has come down significantly due to QIP plus consolidation. Expected 2500 cr PAT in 2018, plus 4500 cr QIP, plus 9600 cr equity at end FY17 implies FY18 equity of nearly 16,500 crores. at MCAp of around 90,000cr, P/B comes to 5.5. the slow correction from past several months seems to have brought this stock down 20% from highs.

in my (rather amateurish) calculations below , I assumed CMP of 1600, with 23% PAT growth rates. If one were to buy at 40 PE today with a long (8-12 years) horizon and also considering P/E multiple contraction to come in the range 25-30, still makes a decent CAGR, I hope. of course, I had to make the strict assumption that BF stays omnipotent .

disc. pondering entry with cash parked in ‘parking spaces’ ITC & Colgate.

5 Likes

If you breakdown the factors that are going to drive the growth of NBFC/Private banks over next 10 years, there are three major ones

- Growth in per capita income. A fairs= assumption here can be 10% CAGR (6% real growth + 4% inflation) - multiplication factor here is 1.1^10= 2.6

- Market Share gain from PSB’s. Currently PSB’s have a 70% market share and are expected to lose 3-4% every year. So in 10 years private banks/NBFC can increase their share from 30% currently to say 60% - multiplication factor of 2

- Consumption loan as percentage of income in India is 15%, it is 100% in developed markets. Say this goes upto 30% in 10 years - Multiplication factor of 2

So total opportunity size for NBFC/Private Banks = 2.622=10.4 times which gives a CAGR of over 26%

However with barriers to entry being low a lot of new players might want to get in, which will impact both the growth and the margin of the existing players. So the opportunity size is big but will Bajaj Finance be able to overcome the challenge of new players entering the scene? I have taken exposure to Bajaj Finance through Maharashtra Scooters which I think has a better risk reward profile compared to direct exposure.

4 Likes

I used to invest in holding companies but no longer…I was always intrigued by their low valuations compared to their underlying assets…so to understand this I read some articles and watched some videos on ‘investment in holding companies’…it was long back so can’t trace them now…If your objective is to benefit only (not also) from BFL’s growth, and if BFL grows, then your returns thru direct exposure will always be higher…much higher than indirect exposure thru a holding co…u can check the previous performance of any other holding company not just Mah Sco to validate this…but if u invested in Mah Sco for some other reasons also then it is another matter…so pls do consider ‘only’ and ‘also’ carefully…these two words used wisely can make a huge difference. It’s like dilute your focus, dilute your returns.

Cheers

RR

5 Likes

One of the reasons I have invested in Maharashtra Scooters is it is a play on huge future dividends.Now imagine if Bajaj Finance and Finserv manage to grow at 20% CAGR for 10 years and pay 20% of profits as dividend you will get Rs 350 per share as dividend from Maharashtra Scooters which is now trading at Rs 2300. to get the same future dividend from Bajaj Finance you will have to buy 5 shares at Rs 8000. Also unlike other holding companies Maharashtra Scooters has a better chance of amalgamation shareholders are already putting pressure on Sanjeev Bajaj to do so, only thing preventing this thing from happening is the case in Supreme Court with WMDC. Regarding capital appreciation yes if Bajaj Finance outperforms Bajaj Auto and Finserv then Bajaj Finance will give better returns but not by that much since 50% of MSL’s value is derived from Bajaj Finance, I dont see the discount which is currently at close to 70% widening, in fact there is a chance it might narrow as there has been a update in the companies act which gives less flexibility to promoters from passing special resolutions on capital allocation. In general your observation regarding Holding companies might be correct but in this case I found exposure to Bajaj Finance through MSL more attractive.

2 Likes

We were to buy an Air Conditioner and thus visited a shop in Chennai. Saw that there is a new competitor in place!

TVS Credit Consumer Durable Loans

There were people from Bajaj Finance, HDB Financial Service and TVS Credit CD Loans. Competition is high and there are all sort of offers to woo the customers from 5% cashback to 100% cashback. Even ICICI Bank, SCB were offering “no cost” EMI apart from 5% cashback.

The moment we express that we are going for “finance”, people from TVS/HDB/Bajaj come to us and pitched their respective offers and we get to choose between them!

In the end, we went with Bajaj as their offer was better and I’m a shareholder. ![]()

Some observations:

- Bajaj Finance was fast to approve the loan and was eager than TVS/HDB fellows.

- They cross sell Bajaj Finance - RBL SuperCard where we need to give consent if we want to be considered for a credit card. Great way to cross sell along with the loan!

- They cross sell extended warranty too and the cost for it can be added to the CD loan.

- The EMI card comes with a fee of Rs 117/year (waived off if used at least once in the past year) when we activate it by requesting a PIN. Our EMI card limit was Rs 65k whereas direct customer ID based limit at store was Rs 50K.

- The sales person said Bajaj Finance may be better as they give an EMI card too which can be used for future purchases.

21 Likes

Thanks for posting your observations ![]()

Yes this is an advantage! Not only future purchases, you can use the EMI card on ecommerce websites, travel websites like makemytrip etc.

And there have always been competitors when you go to buy any consumer electronics item. These days even at small mobile shops there are 3-4 NBFCs offering 0% EMI along with Bajaj Finance. BF has been able to grow their loan book & customer franchise inspite of this. This is what separates it from the rest of the bunch.

6 Likes

Confused - Bajaj Finance or FInServe? Who is providing these loans? I see Bajaj FInserv logo!

It’s Bajaj Finance. They use holding companies’ logo. Even on their Website / Twitter handle / Corporate Presentations etc, they address themselves as Bajaj Finserv

attached these resources for your reference:

https://www.bajajfinserv.in/corporate-bajaj-finance

https://twitter.com/Bajaj_Finance?ref_src=twsrc^google|twcamp^serp|twgr^author

Expecting BFIN to increase market share in coming days. With PSBs gone and among PVT bank , I only see, HDFC Bank in retail loans, whereas Axis, ICICI still struggling,plenty of opportunities for BFIN.

Actually in case one attends, Chola, BFIN and HDFC Bank concall, you will get overall ground report of the market pretty well.

1 Like

Cost of funds will also increase right? yields may touch 8% going forward

That is for all NBFCs. BFIN is no different. But good NBFCs with an excellent management knows how to keep cost of funds low. Just read HDFC sec reports on Chola.

Don’t worry on cost of funds. In case it goes up, weaker ones will be more badly affected.

1 Like

Basant mentioned a very pertinent thing about interest rates or cost of funds. It does not affect one company, it affects an industry. If the cost of funds go up, the most affected will be the weaker players with low margins. Till they make profits everybody can compete. But once the profit margins becomes less the weaker players become exposed. The strong players will become stronger. bad times actually put many competitors out of business by weakening their business model.

Most of the strong players like HUL, Asian Paints, HDFC, Page, TTK, Indusind and the like became much stronger after the 2008 meltdown. These companies gave enormous returns. In fact many of these companies’ share price took a breather when the stock markets actually turned bullish. I made far lower returns since 2014 than I did from 2010-2014.

13 Likes

What would be an approximate mak size that bajaj finance is addressing . ?

Results are out

4 Likes

8 Likes