As per february visit of Reed Hastings - there are 100% chances of Netflix piggybacking Jio’s fibre plans.

Source - https://factordaily.com/netflix-jio-partnership-in-india/

As per february visit of Reed Hastings - there are 100% chances of Netflix piggybacking Jio’s fibre plans.

Source - https://factordaily.com/netflix-jio-partnership-in-india/

From this statement I remembered a humorous statement from my friend who’s earning his bread and butter by investing/re-investing in startups:

Entrepreneur - I am building Quora for blue collared workers

Investor - So it is another Metoo startup; I am not interested in funding it.

Entrepreneur - Sir it has good MOAT compared to Quora

Investor - I am still not interested

Entrepreneur - Sir, we are based out of Republic of China; and our target markets are Shenzen, Goungzou, Foshan, Youngzou and so on…and this is also one of the MOAT

Investor - How much amount you need for scaling up?

Its always nice to listen RD

From a customer standpoint and by customer I mean the end user Amazon, Flipkart or even a Netflix has provided choices that were previously just not achievable. I still remember 5 years back when I was trying to buy a washing machine most of the offline retailers were not willing to give a paisa off, were overpriced and one guy even refused to provide a home delivery after the customer (me) planning to spend around 25K.

I went ahead and bought from Snapdeal.

Similar options exist in electronics. For those who are interested, the choice in CPU’s, motherboards, ram types, SMPS etc…provided by an online retailer far exceeds anything that the offline world used to provide. (I quote this example because I am somewhat of a computer enthusiast and have dabbled in the world of PC graphics, gaming etc…for almost 2 decades now and have personally seen and experienced the change.

Also as mentioned before in this thread, small customers and new age entrepreneurs are also benefiting. I see so many home grown food brands in Amazon or Flipkart which I have never seen before.

Maybe it hurts a small group of powerful organized retailers but good riddance to them. I would not personally want to go back to the old days for no reason.

FY 19 Q3 results are out

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=70e00d02-a5a8-4dda-82c8-d369df8dfc72

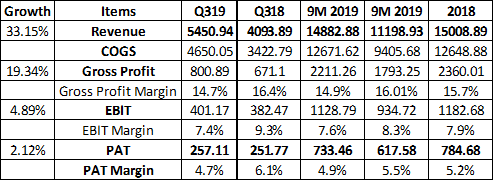

Mixed set of numbers from Dmart. The negative obviously is the reduction in margins - due to front loading of expenses and spending due to the festive season. These clearly are temporary. The reduction on gross margins - now at 14.7% - needs to be viewed in light with historic averages. My sense is that they will maintain it at 15%. The growth rates of sales/gross profit/ EBIT and PAT are 33%/20%/5%/2% respectively.

The good is the great growth in topline of 33% that too on a high base - which indicates a stellar gain in market share. Only a retailer will tell you how important growth in topline is for a retail operation - ultimately a business chugs along at the topline growth level.

The D-mart story is very well intact in my view.

Best

Bheeshma

Could the revenue growth be due to inflation ?

Probably some of it atleast, what is most likely real growth rate

IMO, it could be inferred that sales growth is due to discounts etc leading to lower margins. Inflation is benign and that is not a great thing for a retailer.

No of stores have reached 164 with 6 new stores opening in Q3.

1 Store was added in the Q1FY18

4 stores were added in the Q2FY18

5 stores were added in the Q3FY18

14 stores were added in the Q4FY18

5 stores were added in the H1FY18

Total = 24 stores were added in the FY18

2 Stores were added in the Q1 FY19

3 stores were added in the Q2 FY19

6 stores were added in the Q3 FY19

5 stores were added in the H1FY19

As store opening is on expected lines & Growth in top line is also fine. Flat PAT may raise minor concern as it could be due to festive season.

Neville Noronha has clarified that the company’s topline continued to grow well, even though profit after tax (PAT) growth remained flat vis-a-vis the corresponding quarter last year, primarily due to gross margin reduction on account of price cuts.

“Operating costs inched upwards due to preloading of certain expenses - primarily around capability building across infrastructure and people,” he added.

Views that show the negatives of a company that is perceived as super-good are absolutely invaluable, because a company which people are vehemently justifying paying 110 PE for, anything negative cannot possibly come to their minds.

Here we see that profit has been dropping for three straight quarters. Revenues may be increasing, but this is the trend these days with the new-agey retailers. They give hefty discounts to keep the numbers well dressed or let the customers get a feel for their way of retailing; And when they stop the discounts, revenues often dry up too.

I dont know how 110 PE types companies have behaved in the past; has the profits growth slowed down? And when they have, has the high PE sustained?

I think 33% sales growth is due to festive season but there is no profit growth due to more discounts are offered to retain customers because intensity of competition has increasing as Dmart strategy is being adopted by Food/Big bazaar & Reliance retails of everyday low price offers.

This is a third quarter in a row without meaningful profit growth.

A couple of more quarters without profit growth and stock price may start going south.

Views of other participants required on the topic.

Thanks.

Appears to be a classic double-top, coming on the back of below average results. Page took a 40% beating from the top (as of today, can’t say bottom has been found) on the back of tepid results which couldn’t back the valuations. I suspect same could be the case here. 40% from the top would be around 1000 levels. I see value around 800-850 levels but doubt if it will get there as the 1700 high will act as a price anchor.

I would like to highlight following points which have emerged after discussion with my equity adviser-

We all visualise that market is ready to pay a particular high price to a particular stock. But this high price is a result of demand and supply equation. Prices can go high due to excessive demand or short supply…the later may be a case with D-Mart…we need to quantify the availability of its shares in the market…as i know its much less as compared to other stocks as majority is being owned by the promoters…The balance 15% or so which is available in the market may be in the hand of very few who might be creating a artificial short supply…so with the reputation of a great business along with a short supply creates a recipe for high valuation. Those very few might be people with very deep pockets who have the capability to influence the market and if these big bulls do not release the supply, high valuations will continue.

If promoters have recently sold the shares at a PE of 40, this gives us a hint about correct valuation for the stock. A lot of clarity emerges when we compare the stock with the real estate. If a person is selling a land at some particular price and the seller happens to be a savvy investor himself who is well versed with the future prospects of the Indian Market, he will not certainly sell his property at a huge discount. Only in the situation of great financial distress, he will opt so. But this does not seems to be the case with D-Mart promoters. For them, they needed good money which can be utilised for the expansion of the business. So they must have not sold it at a great discount to its intrinsic value.

Promoters of India’s favourite drink frooti have never bothered to launch an IPO because they have ample money…

With these thoughts, a 1 year past PE below 40 is suitable to enter which in turn means a long drawn patience. Even a 1 year fwd PE of 40 with a visibility of 20% EPS growth currently means a price of 688.

This a hypothesis of mine as i have not really collected any data but just went through the threads of fellow investors on this forum. I request for your views as D Mart present a good learning lesson for us…( not invested but resisting hard to not buy at an overvalued price… )

)

Hi @ranjan_r

This is the trend of Dmart Gross Margins over time. The average gross margin of the last 8 years is ~15%. Gross margins are just reverting to that.

Operating expense % has gone up by a few basis points as highlighted by you but not by a great amount but in retail a few basis points is meaningful esp in dmart.

The gross margin is expected to bob around 15% as far as i am concerned.

Best

Bheeshma

The reaction to dmart stock price is typical of a very high PE stock undergoing valuation compression. At these kind of valuations a lot of quarters’ worth of high growth is priced in. Markets usually forgive lacklustre results of these kind of companies foar a quarter or at the most two quarters and that too if there is clear reversion to high growth post these lacklustre quarters.

Here in case of d mart no one is sure about when normalised margins will be regained or henceforth what will be normalised margins.

When high PE stock suffers valuation contraction its often a painful ride for shareholders. And many a times the pendulum doesnt stop at the centre. It often swings to the other extreme. (Though in case of dmart i think there still might be buyers at some levels where the pendulum is close to centre.)

Got it now Thanks but Historically if you see,Q4 tend to be week quarter for dmart. Have doubt whether dmart will achieve ~15% margin…

One may run a screener for 17%+ CAGR and relatively high PE 7 years back. Despite ups and down, one may be surprised.

Story of Dmart stays Intact: High Quality + High Growth + Extra Large Opportunity

Topline grew at 33%, bottomline 2%. Last year same qtr operating profits were abnormally high and are now reverting to the mean

Now as it is the most expensive stock, valuation have come down as market had priced in the best.

My sense is as long as topline growth stays… it won’t fall too much from here… and might trade in a narrow range. I would monitor new store additions. Last year they added 14 Stores in Q4 FY18. Need to see if they can replicate the same next qtr.