The carnage continues, at this point is this still a market overreaction to some negative news and one negative quarter or did the conference call not build confidence in investors?

Exited 50% of holdings today (enough to cover initial investment).

This panic selling is what bringing d bloodbath to the street. If v avoid it, at least we can contain the further fall. Why do we live like there is no tomorrow in extreme Bull phase n bear phase.

I think it’s fairly priced given it’s earnings yield n future growth rate greater than the G sec yield

Earnings yield are calculated by considering current EPS / current market price. But will this year also EPS would be same ? that’s the question. What is the worst case scenario.

Prices go down by 20% (affecting revenue)

No volume growth

Raw material prices do not decreases (already up 20% from last year , affecting margins )

In this case how much EPS company can produce or how much it can go down from current EPS of 98.

Not to forget the possibility that for the farmer- The variable costs become higher that the sale value, which would mean he wouldn’t grow the 2nd or 3rd crop. To me this is the worst case possibility, which would in the short term mean volume degrowth for Avanti in feeds business.

However, such a situation for the farmer is far likely to occur in Vietnam before it occurs in India, since costs of production are higher there. If and when it happens, it should reduce supply bringing price to normalcy.

Feed Growth 4303141.1(10% YOY)=473345 MT65

(Mgmt stated prices are almost stagnated. I have taken avg price instead of 69 which was around during Q4FY18. On the other hand, mgmt Stated its around 90 currently)=30767 mn

So total Revenue comes to 40942 which gives 20% YOY

Taking NPM of 10% we will have 4094 mn gives a de growth of 12%.

But with CMP its still available at 6.47 YE. Including the DY i think its almost comparable to the GSec. That too with the conservative estimation.

PS: Going by feed price of 90, we will hit revenue of 42601 mn in feed and 52776 in total, giving a NP of 5277 and yield of 8 which very attractive i think

Do you expect Shrimp processing rates to remain the same?

Management has guided for EBITDA margins of 8-10%. This is before depreciation and taxes.

Consider that for a Company having EBITDA margin of ~20%, the prices have dropped by ~20%. Plus RM costs have gone up. The management has said they won’t pass the increase in rates to the customer, so as to still make it viable for the farmer to be in business.

In light of this, do you still expect NPM to be 10% ?

Requesting for reasons as well. Thanks

Raw material prices for feeds rising to all time high ---- Avanti unable to pass that on to farmers. SO a margin hit there completely for Avanti as management mentioned.

Export prices falling by 20-30%… leading to farm gate prices falling… As per management at these rates farmers are making no profits no loss…

The positives:

The raw material prices seen to fall in future due to a good monsoon

Export prices seen to rise in future as shrimp consumption in USA should increase after the slowdown due to the extended winter. Plus China imports seen increasing…

Surely the headwinds are there for the sector but next few months need to be tracked closely to see if the pain points are receding…

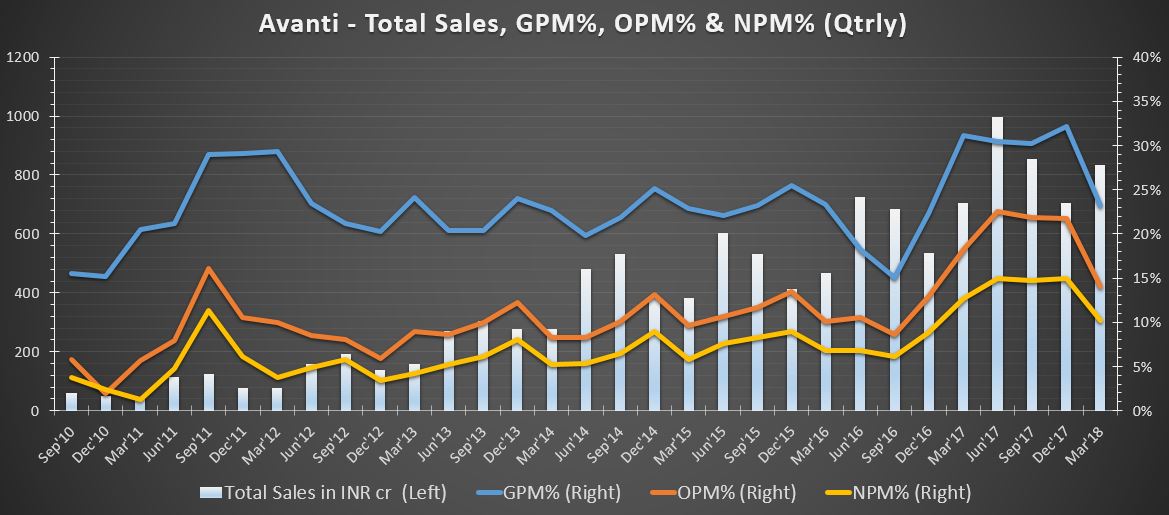

Avanti Feeds Ltd

Highlights of Q4 FY18 and FY18 annual results

Financials

Q4 FY18 Consolidated

o Revenue grew by 25 % to 849.38 Cr from 681.56 Cr last year same quarter

o PBT De-grew by 5.28 % 124.60 Cr from 130.6 Cr last year same quarter

o Profit percentage stands at 14.67 % from 19.6 % last year same quarter

FY18 Consolidated

o Revenue grew by 29.71 % to 3392.960 Cr from 2615.74 Cr last year

o PBT grew by 109 % to 704.17 Cr from 336.93 Cr last year

Segment Wise revenue

Shrimp Feeds

o Q4FY18 Standalone

Profit stands at 112.88 compare to 123.66 Cr last year same quarter , it was less due to increase in price of raw material of fish meal and soya

Fish meal price grew to 105.22 from 78.20 last year same quarter

Soya price grew to 36.03 from 30.65 last year same quarter

o FY18 Standalone

Revenue grew by 26 % to 2853 from 2230.83 Cr last year

PBT grew by 114 % to 630.66 Cr from 294.64 Cr last year

Processed Shrimp

o Q4FY18

Revenue grew by 71 % to 109.21 Cr from 63.97 Cr last year same quarter

PBT grew by 68 % to 11.72 Cr from 6.98 Cr last year same quarter

o FY18

Revenue grew by 51.33 % to 581.18 Cr from 384.06 Cr last year

PBT grew to 73.84 Cr from 42.10 Cr last year

Current status of shrimp culture in India

Export price has been declining steeply during the last 3-4 months due to reduce shrimp consumption in US on account of extended winter season result in pealing up of stocks and stable shrimp production in stable shrimp production in countries like Indonesia, Vietnam. The shrimp imports by China from Vietnam were also curtailed due to Chinese Regulatory reasons.

Now again the consumption of shrimps in US has come back to normalcy and the demand started picking up. The Chinese imports are also expected to go up in the months to come. Company have to focus on other market also

Farm gate price has also increase again now and farmers realise that decrease in farm gate prices was a temporary situation . For long term shrimp consumption is increasing assuring the demand will increase in the long run . Shrimp culture will be on the same level as of 2017-18 and in Odisha and Andhra Pradesh the culture is increasing from last year

The farmer would have invested in developing the infrastructure for shrimp culture and would prefer to continue this activity as the profitability is more in shrimp culture compare to other agriculture crops. Therefore there is no need to have apprehension in sustainability of shrimp culture and exports from India in this year or in future

Company feed business is expected to grow by 15 % in FY19 , sales of 4,30,000 MT in FY18

Profitability was at peak in FY17 which is basically comparable to now.

Price of Fish meal and soya was marginally less in FY17 compare to FY18

Average Fish meal price in FY17 was 95rs per Kg and expecting it to 98.50rs in FY19

Average Soya price in FY17 was 38rs per Kg and expecting it to 41rs in FY19

Assuming other cost remain same the PBT is expected to be around 12 %

IMD has predict a good rainfall which has already touched most of the states . This is a good sign of production for agriculture crop like soya and wheat which is important for company and may have positive impact on prices looking forward

Exporting of shrimp in FY19 is expected to about 14,000 MT representing a capacity utilisation of 60 % . Company total capacity is 2000 MT .

Focus on value added product and achieve a minimum 70 % of exports of these products and rest in other areas. Export prices and raw material prices are highly dynamic and volatile . Considering the past performance a PBT of 12-15 % seems to be achievable

Q&A

Till how much will the trend of price of fish meal will increase ?

o Trend has slow down now moving upward . Now monsoon has started and farmers are expecting a good crop. SO it will be more on the stabilisation not on the relaxation in the immediate future because in next 15-20 days the sowing will start in major states like Madhya Pradesh. After the culture of soya is good the price is likely to be stabilise or even come down

What are the drivers for fish meal prices ?

o Fish meal prices depend upon the fish catches available. Fy17-18 was a unusual year where there were low catches and production went down so the prices increases. That’s why company had considered FY16-17 more comparable year then FY17-18. Now going forward if catches are good then prices will come down . At this point of time company can say that now prices will not go up

What is the current feed realisation of the company ?

o Yearly average is 65,300 to 65350 Per metric ton last year. In last quarter company has to provide certain discounts so that’s why realisation in last quarter remain lower compare to other quarter

How much capacity come up from Thailand and Vietnam has impact on shrimp prices ?

o Issue is regard to the demand , the continuity of demand will be there throughout the year . Main reason was consumption level came down. India is the largest exporter shrimp to USA today and company don’t see any changes in that , company will be the major exporters going forward.

o Whole Industry is now trying to increase their efforts to other countries in respect of value added products to countries like Europe so it is very difficult to predict that which country is impacting hoe much unless company have data of each country

Is the current situation on ground is bad as company is cutting the guidance ?

o The Ground realty is that culture is cutting and there is not going to be decrease in culture so when the culture is there the feed consumption will be there . 4.7 lakh ton in FY17-18 and another 15 % growth in FY19 will make it to 5.25 lakh ton in FY19 .

In presentation it is mention that India shrimp growth is expected to 5-10 % in FY19 but company is guiding of 75 % increase in production . So what gives company confidence to maintain such a growth rate ?

o There is no lack of demand in exports of shrimps . Company will be able to compete with prices and also improve markets and diversify into other countries also so company had targeted this growth in FY19 . Company will achieve over 65 % capacity realisation in Fy19

Is there any price increase as realisation is more on QOQ compare to YOY ?

o It is very difficult to increase price increase at this point of time because farmer are under gate situation so company want to actually encourage the farmer to go for culture. So there lies the success of the industry . So what is happening now is only a temporary phenomenon so same price will not increase . This financial year there will be no increase in price because company have to protect the interest of the farmers also for sustaining of the culture .

o In profit margin as realisation being more or less the same don’t take the realisation of Q4 FY18 , one have to take the average realisation for the whole year that will be more relevant. In FY19 also company will be able to meet the profit realisation is there will no increase in raw material price . Company volumes also goes up so it will grow in absolute terms and also in percentage terms .

How many months of raw material inventory company hold and what is the average realisation for fish meal and soya ?

o It depends upon the weighted average system . In volume term company maintain it depending upon the fish meal season company hold it up to two months also. If the pricing is likely to go up then company stock for two months .

o Soya bean is locally available so there is not much fluctuation so company hold inventory for 30 days and if necessary it take up to 35 days

o In imported items company maintain it to 60-90 days

o Average price for soya bean is 40rs and hope it will come down further

o Average price for Fish meal is 98-100rs and hope it will come down further

What about the inventory in US how much time it will take to sale ?

o In couple of two months it will clear and things are now changing

What about capacity utilisation on feed side ?

o It is 6 lakh tones and primary objective is completely utilise capacity 5.4 lakh consumption in FY19. So company will watch the consumption in current year and then go for expansion which will be necessary in FY20 end

By how much farm gate prices has come down in percentage term ?

o Come down by 25-30 % YOY . Now it is stabilizing

o In this season the prices are on the downward trend because it is the first crop of the season . Prices could be 15-20 % less YOY. The rice in price depend on demand and supply

At what level the farmer will start incurring losses ?

o Last year farmers had made a huge profit margin but level of profitability will not be at that level . The expenses has also gone up like lease , rent . Now correction will take place . So currently the farmers are breaking even not making losses . Last year was exception because they make very huge profit

o Government is supporting to grow this sector so further reduction will not be seen in prices of shrimps

Is there any request from government to reduce feed price from feed manufacturers ?

o There is a general discussion which is happening . Most important is quality of feeds but it depend that reducing quality will give the farmer expecting results of aquaculture and reducing the feed quality will not work

As company have highest market share so company have economy so does company get economies of scale in terms of raw material prices cheaper then others as size of company is big ?

o There are 3-4 factors which determine the profitability and pricing

As having 43 % of market share company get economies of market share

Quality of feed which company maintain by the formulations from which farmer get better FCR . Company have R&D also and company will able to provide good quality

Company have fleet of technicians to get the best quality products

In spite of increase in prices company will be able to maintain the profitability ?

o Yes

What was the gross profit margin in the processing business in current year ?

o Company have ready to eat product and ready to cook product . In ready to eat product there is good margin compare to ready to eat product. It could be anything from 7-15 % so company try to maximise toward the higher margin objective in which 70 % toward value added product which is combination of lower end and higher end value added product and also the other normal traditional product on PBT margins

What was the price for fish meal and soya in FY18 ?

o Average was 89rs and soya was 33rs

Why there is not PAT growth even of revenue growth in past 2 years ?

o As capacity will goes up naturally the profitability will grow up then PAT will also grow up. Current scenario is a short term phenomena company cant take it for future

Is there any seasonality in international prices ?

o It is a complete demand supply , as the demand is more the prices will always be higher and quality of shrimp also determine the price.

In FY18 how much volume does company do in processing ?

o 5800 metric ton

Does company will not see growth in PAT level in coming 2 years ?

o Yes as exports goes up revenue goes up and naturally the profitability goes up .

o Two year is a very long period and what is happening is for very short term . One should not take it as standard and use for future

Does company had sell any ready to eat product in FY18 ?

o Not yet company is working on that

o Ready to cooked products has been already started

o There are three levels

Raw

Ready to cooked products

Ready to eat products

In 14000 Million ton of target next year how much will be the ready to cook ?

o Around 35-40 % will be cooked and selling to US market and other markets also

o In FY19 company will have ready to eat also

o Company have both spot order and long term contract orders . Company is getting very good orders coming now for long term coverage and it will be delivered on month to month basis

In the last 5 years what was the lowest raw material price and highest raw material price ?

o Prices had been lower then this , about 15 years back the price of fish meal was 20rs and those days company was use to import the whole 100 % fish meal . Global prices are also around 100-115 rs. Recent is the highest price

Now how much fish meal is imported and domestic consumption ?

o Almost 100 % is from domestic market

What kind of market share does top-3 business will have ?

o In India there are two players Avanti feeds and CP put together market share is 43 % and 38 % so total will be 82 % .

Is there any conversation with government to take aquaculture under agriculture to get benefit of it ?

o Industry is trying for it from last 2 decades but it is not happening as government see it as a commercial activity so it don’t considered under agriculture. Company is trying to implement that still

How has been company realisation and production in first two month in current year ?

o The drop in prices earlier then drop in consumption and then farmer reaction is only temporary it is not going to be permanent . Suddenly farmer will not stop doing farming it is only a correction that is taking out and company is giving the message to farmers that don’t get panic it is not a permanent hurdle

o Yes company is able to work in April and May according to projections

Does company see any healthy competition from others ?

o Company don’t see any threat from any of the competitor . Because company always at the doorstep of the farmer as he needs whether in formulation for high HCR , any problem regarding with water and growth . So company is there for advising

Interesting contrast between media articles and management commentary of the two leading players of aqua industry - Avanti Feeds and Apex Frozen food. Both are saying that the problem is not as big as projected in media and the things are slowly improving. Both the companies have guided for volume growth despite industry problems.

In the case of Avanti, the management sounded pretty confident of 10-15-20% growth in feed business despite the headwinds for the industry (thereby further increasing market share). As per the presentation, they also expect to increase the utilization in the processing segment to 60% and post good volume growth of over 50% (though turnover will reflect less increase due to fall in price of shrimp by 20%). Despite this, even if the company does deliver on growth of 15%, the profit may fall 10-15% for FY19 given the reversion of margins to earlier levels.

One will like to see improvement in price of shrimp for the long term growth and sustainability of the industry.

But as often, by the time performance and situation improves evidently, the stock price would have adjusted accordingly. A certain leap of faith is always required.

100% agree with @ayushmit that improvement in shrimp prices (especially for new and levered shrimp farmers) would definitely be very beneficial for the entire value chain and long-term industry prospects.

I’m interested to learn Avanti’s business model regarding their Processing & Exports segment. I hope that they would maintain a spread/margin regardless of the underlying price volatility of shrimp. Like CCL Products, they take order first from their international coffee clients and then buy raw material coffee beans, maintaining the spread by keeping appropriate margin and not focus on what’s happening with coffee bean prices. If anyone has any insight into Avanti’s processing and exports segment, please share it or else I will try to ask this question on next quarter’s conf call.

If they try to maintain the margin and not focus on speculating prices (buy more shrimp when prices are low and then get butchered when prices fall further), then business model should be sound and long-term sustainable.

If they expect to increase the utilization in processing segment to 60% and post volume growth of over 50%, I would expect them to make decent money considering that their COGS would also go down with fallen shrimp prices. Good monsoons shall help them to maintain decent margins in feed segment keeping raw material prices in check, which is outside of their control.

Next 3-4 quarters very crucial for everyone part of the shrimp ecosystem. Expecting feed industry leader to come out stronger through this rough patch (hopefully its temporary) given that they have capacity to suffer thanks to healthy cash on b/s. And this stock is definitely not for faint hearted given cyclical nature of the industry. If I happen to own Avanti for next decade, I expect at least 3-4 more draw-downs that are north of 50%.

On a side note - I as an end consumer, here in the US, have so far not benefited from the fall in global export shrimp prices. Was paying $5 late last year for 12oz or 340gm of medium cooked shrimps from India (peeled, deveined, tail-off) at grocery store, and today I am paying $5.49 for the same packet. Losing on unrealized gain in stock price and also paying more for the same product. Living on double edge sword in this world of shrimp business.

However, according to a third person, also speaking anonymously, companies are planning to wait as they expect the volatility and downturn in the seafoods market to be a short-term phenomenon. “There is a view that the headwinds for the seafoods sector are of a short-term nature and that the pricing will improve going ahead. The companies are thus willing to wait out this period of volatility.”

On 1 June, Avanti Feeds in a filing to stock exchanges said pricing of shrimps is expected to improve with US demand coming back on track. “The decline in price is only a temporary reaction and the consumption in the US has come back to normalcy and the demand started picking up and would be restored to normal level soon and is even expected to go up, which is expected to trigger an increase in prices,” Avanti Feeds said.

The steep fall in the export prices of shrimps seen over the past three to four months was due to global developments such as a temporary decline in the consumption of shrimps in the US due to a long winter coupled with stable shrimp production in countries like Indonesia, Vietnam, the company’s filing said.

AvantiFeeds CEO has said they will do 10-12% PAT margins this year and topline will increase by 10%. If we extrapolate the numbers, their FY18 topline was 3392 Cr. So approx topline would be 3731 and net profit would be in the range of: (373 to 448 Cr). FY18 was 465 Cr.

Fy18 was an exceptional year for the company, those margins are just one-off. Going forward the stock would not be given growth valuations in my opinion as profits would be lesser as compared to FY18.

Longer term prospects (3+ years) look good though.

Not fair to expect Avanti to repeat FY18 GPM, OPM and NPM performance in FY19. FY18 was a glorious exception; it is past now. Investment thesis from hereon should be based on i) normalized margin, ii) current valuation and iii) return on incremental invested capital.

Very interesting data. Thanks for promptly putting it up all the time. It has been very helpful

Data gives more credence to claims of the managements in this industry that probably things are not affected and as bad as reported in media. Or may be we need to see the data of may also. But what a panic it was!

Like rightly mentioned by you, the evaluation from here has to be based on normalized margins, growth prospects and valuations.

Disc: I don’t like to discuss my trades but just because I have been very active on this thread thought of mentioning…have reduced a bit of my position today given the high allocation i had. It was very uneasy to go through such wild swings

Please take your own call or consult an investment advisor